For people just beginning as peer to peer investors, the first step involves opening an account and choosing a few loans to fund. Once this has happened, it’s only a matter of time before they receive their first repayments, payments which also result in their account screen newly displaying the percentage of return their account is earning. However, the return percentage listed on the Lending Club or Prosper websites can sometimes be inaccurate, leading unaware investors to believe their returns are healthier than they are in reality.

In this post we will look at how these onsite numbers are calculated, and use them to show the effect that cash drag can have on our overall return.

Lending Club’s NAR vs. Excel XIRR()

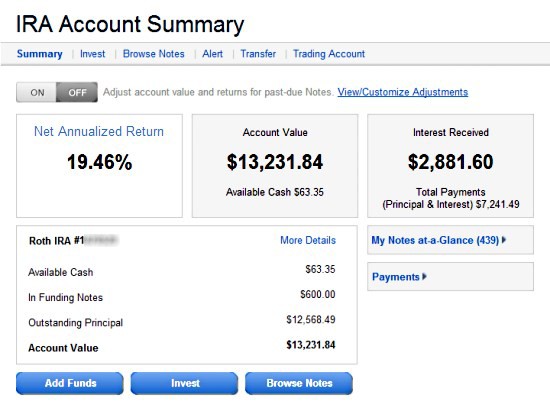

To begin, we will look at Lending Club’s NAR figure (Net Annualized Return). This is the big bold percentage number you see whenever you log directly into your Lending Club account:

My NAR is trumpeting a spectacular 19.46% return on my investment. But hold the champagne. The fact is, the number is inaccurate. How do I know this? By doing a simple XIRR() calculation, I can measure how much return I have earned since transferring funds to Lending Club’s account. The elegance of calculating with XIRR is how it skips getting bogged down in the details of each loan and simply looks at the big picture.

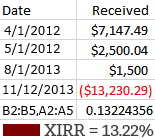

In contrast to the Lending Club NAR, calculating XIRR using Microsoft Excel reports a different picture altogether. Since transferring a total of $11,147.49 over the past 18 months, my account has an actual return of 13.22% – over 6% lower than 19.46%, and a much more realistic sounding return.

In contrast to the Lending Club NAR, calculating XIRR using Microsoft Excel reports a different picture altogether. Since transferring a total of $11,147.49 over the past 18 months, my account has an actual return of 13.22% – over 6% lower than 19.46%, and a much more realistic sounding return.

Folio Trading and the Corrosion of Cash Drag

There are a number of reasons why my NAR is inflated. For starters, I have sold a number of loans on Foliofn (See: Using Foliofn to Avoid Defaults), which messes up the onsite NAR. Lending Club told me last month that they hope to release an improved NAR that includes Foliofn trading, but for now its important to remember that trading on the secondary market will make your NAR less and less accurate over time (as a side note, it is interesting to state that thousands of Folio-only traders are totally in the dark regarding their return unless they calculate it themselves).

Second to Folio issues, NAR also does not include cash drag (uninvested funds) in its calculation. It simply measures the return I am receiving on invested money. Unfortunately, a big part of peer to peer lending involves uninvested cash, particularly at Lending Club since they do not have an automatic reinvestment tool like Prosper. As our loans are slowly repaid over time, payments will accrue as available cash. If we do not log into our accounts and reinvest that cash, it simply sits there, bored, earning no interest at all.

Second to Folio issues, NAR also does not include cash drag (uninvested funds) in its calculation. It simply measures the return I am receiving on invested money. Unfortunately, a big part of peer to peer lending involves uninvested cash, particularly at Lending Club since they do not have an automatic reinvestment tool like Prosper. As our loans are slowly repaid over time, payments will accrue as available cash. If we do not log into our accounts and reinvest that cash, it simply sits there, bored, earning no interest at all.

How big of a problem is this? To demonstrate, consider the account screen shot above. As far as investors go, I probably log into my account more often than most, largely because I run this website. I have done my absolute best to reinvest available cash into additional loans. And yet my NAR has always been inflated – even in my very first portfolio post from 2012. If cash drag has negatively affected my account so dramatically, an account that has been checked nearly every day for 18 months, you can bet your buttons that uninvested cash has an even greater negative effect on the average investor.

Boeing’s New 787 Aircraft: Just Sitting There, Doing Nothing

Cash drag is not just an issue for peer to peer lenders like ourselves. You can see the corrosive effect of cash drag even more dramatically in this Forbes article about Boeing (link). Earlier this year, when Boeing’s new fleet of 787 Dreamliner airplanes were grounded because of a battery issue, the grounding meant major lost profits for such a large company:

Cash drag is not just an issue for peer to peer lenders like ourselves. You can see the corrosive effect of cash drag even more dramatically in this Forbes article about Boeing (link). Earlier this year, when Boeing’s new fleet of 787 Dreamliner airplanes were grounded because of a battery issue, the grounding meant major lost profits for such a large company:

“Even assuming battery issue is resolved and Boeing is able to hit its 787 delivery guidance at 60+, we still see 787 as a ~$6B cash drag in 2013 with ~$7B inventory build more than offsetting ~$1B advance draw,” UBS analyst David Strauss wrote in a note to clients.

Grounded airplanes are like uninvested cash in our peer to peer lending accounts. Our investment is not being lost or degrading in quality – it’s simply not being used, and this lack of use means a loss of overall return.

Reinvest Returns and Keep Available Cash to a Minimum

While peer to peer lending is a fairly simple investment, there are a few things every investor needs to remember. Most importantly, we should diversify our account with as many loans as possible – at least 200, if we can afford it. This probably means purchasing smaller $25 notes per loan, especially if an investor is just starting out with something like $500 in trial money. My Roth IRA above is large enough where I can purchase $50 notes and still be diversified. People with $20,000 to invest can be diversified with $100 notes, those with $50K in $250 notes, and so on.

Second to diversifying your account, we need to set up a rhythm or schedule where we log into our account and reinvest available cash. For investors who have just opened their account and need to put a large chunk to work, this can mean peer to peer lending becomes a regular activity for a few weeks. But for most investors with an account of 200 notes, this can mean logging in as few as two or three times per month, especially if they are looking for the A & B-grade loans that are so plentiful these days. Every account and situation will be different, so play around with it and figure out what works for you.

With your cash fully invested, you can be sure to have a better lending experience. Even though many investors at Lending Club and Prosper are misinterpreting their return because of the provided NAR, you can instead focus on the ‘Available Cash’ amount and feel a sense of confidence whenever you see it near $0.00.

[image credit: Angela N. “City Paws“/ Dave Sizer “787 First Flight“CC-BY 2.0]

Have you checked our product, LendingRobot.com ?

We’re a Seattle-based company and created this tool first for ourselves, since investing in LendingClub is very time-consuming, especially if one wants to keep all his cash invested…

There are few other drags on your account not mentioned in the article. When you put money in a loan it may take three weeks before the loan is approved. In the meantime your money is tied up in loans. For my account this is a 200- 300 dollars all the time and you earn no interest on it. Quite a few of these loans don’t happen so you have to start the process over again. I have a radical suggestion make sure all the paper work is approved BEFORE you put the loans out for investing. An early prepayment penalty would discourage 1 or 2 month loans. Also not mentioned is basically your buying a non liquid investment that requires quite a bit of upkeep to maintain and you may really get about 9-10 percent return. If you decide to invest don’t dump all your money in at once at Lending Club loans are scare mostly because they have gone the route of letting big investors get first dibs on the loans, it can take 3 or 4 months to get your money rolled in. Be smart only transfer a couple grand at a time into Lending Club.

I have Prosper IRAs and the cash drag upon withdrawal is not insignificant. There are fees for each withdrawal, and since we can’t sell on FolioN, we must let cash accumulate to justify the transfer fee. I don’t have a calculation yet, but it is measurable and will impact yields.

I thought that if I invested $2,000 in a P2P account, my money would bring me a reliable let’s say 5% yearly income of $100 which is much better than $10 in a .5% MM at the bank. I want to be able to withdraw/spend the return, not reinvest it. Besides, how much is the withdrawal fee; a percentage of the withdrawal or a flat fee? I don’t seem to get something here about “drag money.” Will I get my $2,000 back if I am not satisfied or is there a minimum time you have to sign up for? – Thank you, Mrs. J. Harkay

Withdrawing money from your P2P account is not a quick process. You need to either (1) wait for loans to be paid back or (2) sell the loans on the secondary market. See this article: https://www.lendingmemo.com/liquidate-close-lending-club-prosper/