As we continue to produce more educational content to aid people who are looking to get started in peer to peer lending, I continue to be startled by the number of investors who have negative experiences with Lending Club or Prosper as a result of not diversifying their account.

Here is an actual comment left on LendingMemo’s site last month:

Lenders beware. I speak from experience that this is a good way to lose your money with almost no recourse. I invested in 12 loans rated A or B at Prosper.com and 8 defaulted. That is why states like Texas do not allow Prosper. It is not a scam but smells like a skunk!

Le sigh. Frankly, I am at a loss to understand how anyone is able to have this experience considering the barrage of invitation by the platforms for their investors to create diversified accounts.

The Most Important Thing in P2P Lending: Invest in 200+ Notes

Forever: the one rule we must continue to emphasize is the need for every investor to remain diversified, preferably in at least 200 notes. Let’s look at each of the platforms and see how they interact with this requirement.

Diversification on Lending Club (with Lending Robot)

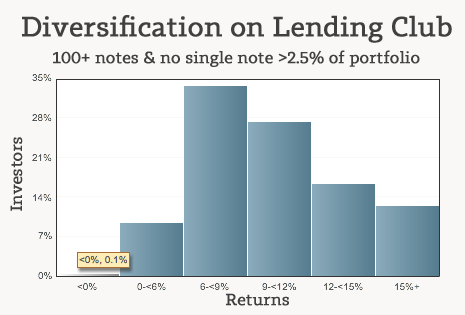

The benefits of diversification, as usual, are front-and-center on the Statistics tab on the Lending Club website. Here is their favorite chart:

The butter-colored box pops up if you hover a mouse over the “less than 0%” sliver. In essence, it shows that investors on Lending Club who are own 100 notes or more (and are not overly invested in a single note) have a one in a thousand chance of losing money. That’s a pretty powerful stat. Personally, I wish Lending Club would trumpet the even more stunning 200-note threshold like the rest of us, but “100 loans” is certainly an easier number for a casual investor to remember, and holds considerable weight on its own.

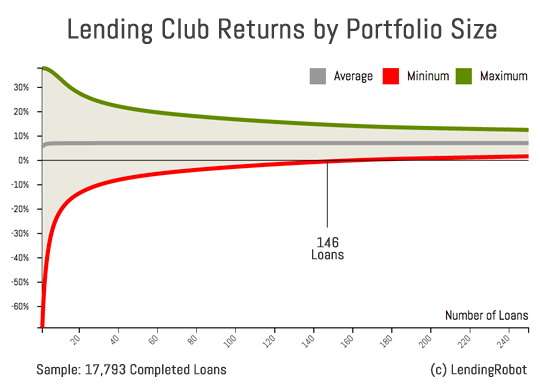

Further evidence of the benefits of diversification on Lending Club is seen within the brilliant new charts at Lending Robot. In the graphic they provided to LendingMemo below, they have aggregated all of Lending Club’s completed loans, cleverly drawing min/max boundaries vis-a-vis portfolio size. Check it out:

As Emmanuel elaborates in his recent Seeking Alpha post, the crossover point seems to be 146 for these completed Lending Club loans. This does not, of course, ensure that lenders who mimic this with similar sized portfolios are themselves guaranteed positive returns, but it does add another party’s vote to the mounting evidence that peer to peer lending (as an asset class) reaches full diversification with a portfolio of 200.

Diversification on Prosper (with Orchard Platform)

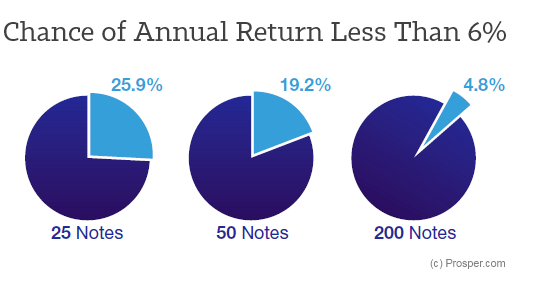

How does Lending Club’s position compare to Prosper’s? At LendIt last year, Prosper distributed a whitepaper (download it) with the following pie charts:

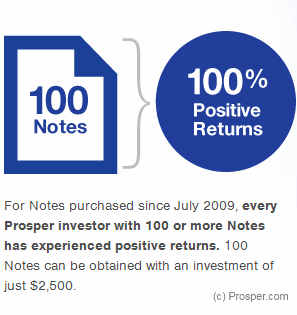

Tasty. Furthermore, their Prosper.com/Invest page has a graphic (reproduced on the right) that says all investors since 2009 with 100+ notes have earned positive returns. None have lost money. While I do not feel much need anymore to compare Prosper 1.0 to Prosper 2.0, this 100% stat is remarkable. By comparison, Prosper 1.0 had just 19% of diversified investors with positive returns (858 out of 4,450).

Tasty. Furthermore, their Prosper.com/Invest page has a graphic (reproduced on the right) that says all investors since 2009 with 100+ notes have earned positive returns. None have lost money. While I do not feel much need anymore to compare Prosper 1.0 to Prosper 2.0, this 100% stat is remarkable. By comparison, Prosper 1.0 had just 19% of diversified investors with positive returns (858 out of 4,450).

Alongside Lending Club, Prosper seems to advocate the easier-to-remember 100-note threshold as being adequate for a positive return.

To augment this conclusion, the svelte Orchard Platform did their own analysis last month of diversification on Prosper. Their work is always worth a full read (with graphs to boot), so you should definitely go there for the complete article, but here is their conclusion:

“Based on our analysis, if an investor cannot invest in at least 200 notes, the resulting portfolio may be too volatile to be predictable, and the likelihood of a very low (or negative) return becomes higher.”

[emphasis mine]

Four More Strategies to Diversify Our P2P Lending Portfolios

Although the most important requirement for lenders is having 200 similarly valued notes, additional diversification can be had by investing across:

- Risk-grades

- Vintages (issued quarter)

- Geographies

- Platforms

Strategy #1: Invest in Multiple Risk-Grades

One way we can avoid over-saturation within a particular borrow population is by investing across a gradient of the credit spectrum. This can be accomplished easily enough by purchasing notes in different risk grades.

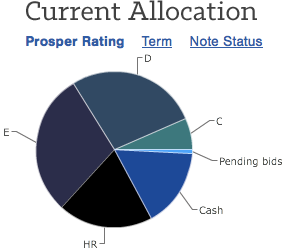

Personally speaking, I had become overexposed within my Prosper accounts by only investing in the riskiest D, E, & HR grades. To aid this situation, I have injected an additional sum of cash (seen in the graphic from my Prosper account on the right) that will eventually be 50% invested in C-grade notes, albeit those with an expected return of 16% or more.

Personally speaking, I had become overexposed within my Prosper accounts by only investing in the riskiest D, E, & HR grades. To aid this situation, I have injected an additional sum of cash (seen in the graphic from my Prosper account on the right) that will eventually be 50% invested in C-grade notes, albeit those with an expected return of 16% or more.

Tax Strategy for Multiple Grades: If one wanted to really pull the most benefit out of this approach, it might be a good idea to have both a regular (taxable) account coupled with a tax-incentivized account, like a Prosper Roth IRA. By placing the lower-earning loans in the regular account and the riskier higher-earning loans in the tax-free IRA, investors can achieve a better harmony of both liquidity and taxation.

Strategy #2: Invest in Multiple Vintages

Purchasing notes across differing vintages happens naturally for those who continue to add more funds to their account over time. In contrast, investing one lump sum in a single quarter isolates an investor to the national economics of that season, as well as only a single iteration of underwriting standards.

Since the national climate is always changing, and platform underwriting continues to both improve and flux in response to this climate, it is a good idea to try and inject lump sums intermittently, while avoiding a single large deposit (although I am interested in hearing approaches that might try to “time the market” of national employment).

Strategy #3: Invest in Multiple Geographies

As lightly touched on in my recent The Joys of Redlining article, peer to peer lending allows us to focus our investment within particular geographies. It is important to remember that both Lending Club’s and Prosper’s prospectuses highlight unemployment as one of the primary national conditions that affects peer to peer lending default rates. In this regard, investors might consider reviewing the geographic distribution of their portfolio using tools like the NSR Portfolio Analyzer.

This strategy is certainly the weakest, but I am curious if it is possible to balance notes across different geographies so as to reduce susceptibility to unemployment, considering certain areas of the country feel the swings of the national economy in different ways. Might it be possible to be less affected by a rise of unemployment in agricultural areas by balancing a portfolio with notes from tech-rich areas?

Strategy #4: Invest in Multiple Platforms

Finally, I continue to encounter investors who are solely involved with Lending Club. I sympathize with this approach considering the market leader is officially profitable and awash in revenue. Heck, my own affiliate ads for Lending Club are placed higher in the sidebar for that reason.

That said, Prosper has become a formidable player within peer to peer lending as a whole. Having exceptionally redefined themselves away from the company’s bumpy beginnings, the new management has turned the company completely around (Lend Academy), and done it in a single calendar year. By my projections, Prosper should go on to issue at least a billion dollars in new loans during 2014.

As investors in peer to peer loans, we can further diversify our account by spreading it across both Lending Club and Prosper. Have concerns that Prosper’s loans are of lesser quality than the rock-solid Lending Club underwriting? Again, here is the astute Orchard Platform to crunch the 2013 data and go on to vouch for Prosper’s current underwriting:

As investors in peer to peer loans, we can further diversify our account by spreading it across both Lending Club and Prosper. Have concerns that Prosper’s loans are of lesser quality than the rock-solid Lending Club underwriting? Again, here is the astute Orchard Platform to crunch the 2013 data and go on to vouch for Prosper’s current underwriting:

“From our analysis, we believe Prosper has not compromised its standards in order to grow. Whether we’re looking at external factors (ScoreX, Income), Orchard’s model, or Prosper’s model – we see that the quality has remained consistently high.”

Loan Quality for 2013: Prosper | Orchard Platform

Certainly, neither platform can perfectly capture prime-borrowers who are worth of our investment. Both Lending Club and Prosper, despite their best risk-pricing wizardry, are going to mistakenly deny a small subset of people who would actually be great recipients of our cash. But by spreading our investment across both platforms, we can further assuage the volatility that might come through overexposure to one particular standard of underwriting.

For most investors, this is essentially an invitation for you to add some Prosper earnings alongside your solid Lending Club returns.

Maximum Diversification: A Good Idea?

It is possible to reach a point of near-maximum diversity, a point where a portfolio begins to simply reflect peer to peer lending as a whole. For those who can afford it and are looking for all the stability they can get, this could be done through constructing a portfolio of thousands and thousands of notes.

However, it bears repeating that there might be such a thing as over-diversification for those of us who are seeking to beat platform averages. Considering a platform like Lending Club offers us a great return, the more notes we take on, the more we graft ourselves into their average. For those of us (myself included) who are interested in 9-12% returns, too much diversification may actually do more harm than good.

As an aside, I am curious if note selection may ever begin to bring adverse results. For instance, mutual fund managers the world over consistently attempt to beat national averages like the S&P500 through a more “refined” selection of stocks. However, these selections seem to lose to the market as a whole (Forbes). While investors like myself seem to have attained higher than average results for the time being, I am interested if this approach will ever begin to work against the overall diversity that Lending Club and Prosper are attempting to generalize into their yearly issuance.

[image credit:

Rob “Alexandrovsky Gardens” CC-BY 2.0]

Thanks Simon for a comprehensive guide to diversification. I am close to my initial goal of about 400 loans with Prosper ($10,000 +). I will post my results periodically. But my expectations from the analysis I have read would be that my perentage of 13.5% at the present time, will decline to about 9.0 % over one year with the expected number of defaults. Since I am manually investing each loan of $25 (and a few at $50), I am filtering my selections for greater risk avoidance. It will be interesting to see the rate of return this time next year.

Hi David. Sounds like you’re on your way.

I’ve only been doing this for a month, and only through Prosper, so far, but I am finding it incredibly difficult to diversify. I’ve only managed to acquire 64 notes (if you count the many still pending). Of the processed notes, I only have 1D, 8C, 25B, 8A, and 2AA. Prosper seems to average 20-30 new loans per day, gone within 30-120 seconds after posting. I have never seen an E or an HR listed.

Through the manual process, I’m lucky if I find two notes per day.

Using the automated process (which I was told is the way to go so you can compete with everyone else), I average less than one note per day. And it is never anything lower than a B.

I wanted to put $10k into Prosper, but at this rate, it is going to take me the entire year to do it and I’m going to have to be awake and refreshing pages at 10am and 6pm (my timezone) every single day of the year (and 1pm on weekends) to have a chance of achieving it. It seems like the automated system is for suckers. It only seems to run maybe fifteen minutes after the loans are posted and to just shove the crap off onto you that nobody else wanted.

The only way I see of changing this is if I lower my standards and just throw money at any and every loan, which I’m not willing to do.

Cron, you’re not the only one. Their lack of loan volume has really put a damper on their retail community.

At this point it seems like people should start investing on Lending Club and then add Prosper loans to aid diversification.

Best

Simon

Hey Simon,

Overall, great advice on diversification. However, I would suggest that the most relevant metric of concentration risk is not so much the total number of loans, but the maximum (and average) note size as a percentage of the total portfolio. For a sufficiently large portfolio, 100 or even 200 notes could represent very high concentrations. Likewise, 1 very large note and 99 little ones would not adequately diversify. Better to look at the right metrics.

Great website, though. Keep up the good work.

Cheers,

Miguel

Hi Miguel, you’re right. I should state at the beginning that this metric of total number of loans assumes the loans are all of nearly the same value. Thanks for stopping by.

Simon your advice proves valid in 2018 just like it did in 2014. P2P has become popular in New Zealand but we’re a small country and platforms are limited in number as the industry has consolidated. Harmoney is our biggest and they recommend your practice – they’d also limited a loan to a $25 exposure. Thanks for including the economy trends, something that should be at the heart of pushing for diversification!