In Shakespeare’s play The Merchant of Venice, we find Antonio, the wealthy merchant after whom the play is named, feeling emotionally downcast. His friends attempt to figure out why he is feeling so low. They ask him about his finances, but Antonio says his investments are secure:

My ventures are not in one bottom trusted,

Nor to one place; nor is my whole estate

Upon the fortune of this present year:

Therefore, my merchandise makes me not sad. (Act I, scene i)

As you can see, the rich merchant feels secure about his fortune because he has them spread it out in a variety of ways. In short, he is safe because he has diversified his investment. Eventually the listener realizes Antonio is blue because his best friend Bassanio has fallen in love with a foxy heiress named Portia, and is thus leaving him behind. But the merchant makes a compelling point, one that every lender must remember: diversify your account.

Let’s look at some of the ways diversification is important in peer to peer lending, exploring its benefits and highlighting its drawbacks.

Don’t Be Like Vito

The idea of diversifying your investments can be understood in the age-old saying, “Don’t put all your eggs in one basket”. Place your eggs in many baskets. The chance of you dropping a basket and losing an egg goes up, but the chance of you dropping a basket and losing all of your fragile eggs goes down.

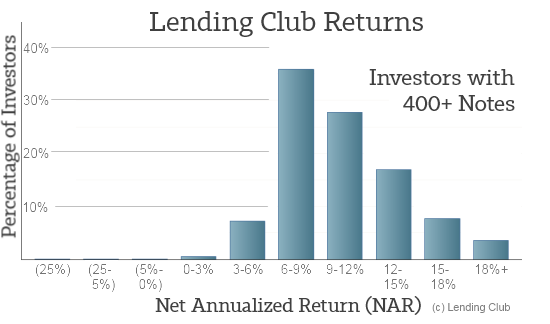

In peer to peer lending, some of the worst experiences come from lenders who put all their money in very few loans. For instance, there is a lender on Prosper named VITO9999 who, while swooning over HR-grade interest rates, invested $500 in one high-risk loan. This loan has gone late, and now Vito is on track to lose half of his invested money. If you search for all Prosper lenders who only invested in four loans like Vito, you will see that 20% of them lost money on their investment. Compare this to those who invest in a couple hundred loans and you will see a dramatic difference: out of 3800 lenders only four have lost money. Lending Club often promotes their “800 Club”, stating how not one borrower who has invested in at least 800 loans has lost money on their platform.

We are able to diversify our investment because we do not actually fund full loans. Lending Club and Prosper have allowed lenders to each buy a small part of the loan, called a note, for as little as $25. In this way, loans as large as $35,000 can be funded by hundreds of lenders. One of the most important things you can do as a peer to peer lender is diversify your investment in as many loans as possible. In this way, you avoid becoming another VITO9999. You reduce the odds that you will lose money on your investment and increase the chance that you will do well as a lender.

How many loans does it take to be diversified?

There is some debate as to how many loans one needs to be completely diversified. If you read my p2p lending eBook, you see that I recommend people invest in at least 200 loans. I believe this because Lending Club believes it. Lending Club Prime is a fully-automated service offered by Lending Club, and the minimum investment originally required to apply was $5000 (it is now $25,000). If you take $5000 and divide it by $25 notes, you get an account with 200 notes. In this way, Lending Club themselves believe that an account with 200 notes is diversified.

There is probably a small benefit to going even further, with statistical evidence of benefits from diversifying in as many as 700 loans (see here), but I feel at least 200 is fine. Lenders who invest in this many loans are dramatically more secure than those who only invest in a few.

Comparing Your Borrowers

One of the huge benefits a lender has when investing in at least 200 notes is that they are able to compare their loans against each other. Over time, some borrowers default while other borrowers remain steady. Having hundreds of notes will allow you to compare your better borrowers against your worse ones. Undiversified accounts (like those who only invest in a few loans) are not able to do this. Over time, you could reinvest your returns into the kinds of borrowers who have been trustworthy.

Don’t Over-Diversify

One reason why I invest in fewer than 500 notes per platform is because my loans are highly targeted using tools like NickelSteamroller. If I wanted to quickly invest in thousands of notes, I would have to loosen my criteria to do so, resulting in a lower overall return. Thus, it can be important to not diversify too much. Remember, the average return on platforms like Lending Club is about 7%. The more loans you initially invest in, the more your account will start to reflect the platform’s average (and we can do better).

One reason why I invest in fewer than 500 notes per platform is because my loans are highly targeted using tools like NickelSteamroller. If I wanted to quickly invest in thousands of notes, I would have to loosen my criteria to do so, resulting in a lower overall return. Thus, it can be important to not diversify too much. Remember, the average return on platforms like Lending Club is about 7%. The more loans you initially invest in, the more your account will start to reflect the platform’s average (and we can do better).

Tip: Stay With $25-$200 Notes

There is a problem with only investing in 200 notes for very large accounts, namely your ability to resell your loans. Let’s say you have $100,000 to invest and decide to diversify in 200 quality notes of $500 each. If you would ever want to resell your notes through FolioFN (say, in a financial emergency), you are going to run into trouble. It is difficult to sell $500 notes; buyers on the secondary market are trying to stay diversified as well. On the other hand, smaller notes of $25-$200 resell much easier. In this way, I recommend people only purchase these smaller notes. If you are investing $100,000, this means having an account with 2000 notes. The drawback is that it may take some time to find that many notes if you invest using a filter, and this investment will be less passive considering you will have to log in more regularly than average to reinvest your returns.

Three Final Ways to Diversify Your Account

Aside from simply increasing the number of notes we own, there are three more ways we can further diversify our account.

1. Buy notes across various vintages (late 2013, early 2014, etc). Try to invest in notes across different years. As the borrower pool changes, it is important to not only keep your investment in one particular season of this population.

2. Buy notes across various loan grades. Have you only been purchasing B-grade notes? You are at higher risk than someone who purchases a variety of loan grades. Even though this may slightly increase your risk or decrease your return, the diversification may be worth it.

3. Open an account an a competing platform. Have you totally focused on Lending Club? Open an account at Prosper. Are you only a Prosper investor? Open a Lending Club account. Investing across each of these similar platforms gives us diversification that a single platform cannot offer.

Conclusion

Interestingly, Shakespeare’s play ends with Antonio losing all his money because some ships sink at sea that were holding his investments. In this way, we need to remember there is another way we can diversify, and that is by investing in a variety of different avenues. As we seek socially responsible ways of investing our savings for high returns, we need to explore additional channels besides peer to peer lending.

Read more: Prosper’s diversification PDF from LendIt2013

Nice write up!

That 800 number from Lending Club is amazing.

Thanks :) I agree. It’s amazing what a difference it makes to have more notes than less.

Excellent write up. Poor vito. I’d like to see someone discuss what they observe are the least ROI-correlated filters…just a suggestion :)

Interesting. Can you explain more what you mean?