One of the most interesting tasks we have within the peer to peer lending community is trying to convince others how Prosper and Lending Club are good investments. After all, only a small portion of people have even heard of peer to peer lending, much less understand what it is.

A Common P2P Lending Conversation

I imagine many of us have run into this problem with our friends or family members. While we may have personally come to accept peer to peer lending as a great way to invest, most of our close-knit relationships are still unaware it exists, or are unconvinced that it is a great way to put their excess cash to work. A typical conversation with a friend might sound like this:

Investor: “Hey friend, have you ever heard of peer to peer lending, a way to invest through companies like Prosper or Lending Club?”

Friend: “Nope. What is that?”

Investor: “It’s really great. You lend out your extra cash to people around the country who need a loan. They repay it slowly with interest.”

Friend: “Like Kiva?”

Investor: “Sort of, but to Americans. I’ve earned 9% per year on my investment. I actually invest through an IRA, so it’s even tax-free.”

Friend: (looking distracted) “Uh, interesting. Gotta go! I’m signing up today for a Fidelity ‘Growth Fund’ that, while rising and falling with wild abandon, could theoretically earn me an 8% return (but probably won’t). This actively-managed fund will eventually take $150,000 in fees from me before I die. Hey, is that a violin?”

Investor: (playing Shubert) “It’s a viola. My 9% Prosper returns are so boringly consistent I’ve finally had time to master Arpeggione Sonata.”

Perhaps your conversations have not gone exactly like that, but the fact remains that we need to identify convincing reasons to help people begin lending.

8 Ways to Convince People to Open a Prosper or Lending Club Account

There are many reasons investors lend through sites like Prosper and Lending Club. However, if you are trying to convince a doubtful friend or family member, here are eight of the best:

#1. Highlight the Great Returns

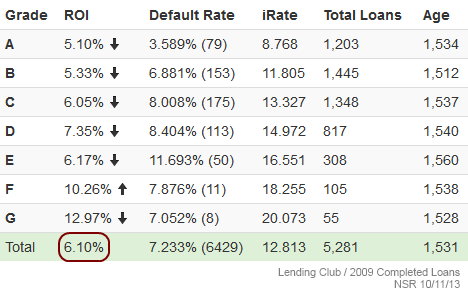

Nothing gets heads turning like raw ROI (return on investment). As stated in the recent post P2P Lending: What is an Expected Return?, the diversified lender can expect to earn between 5% and 12%, depending on their degree of risk and skill. Let’s look at this more closely. Below you will see the return for Lending Club’s 2009 3-year loans, which by now have all been paid back in full (or defaulted):

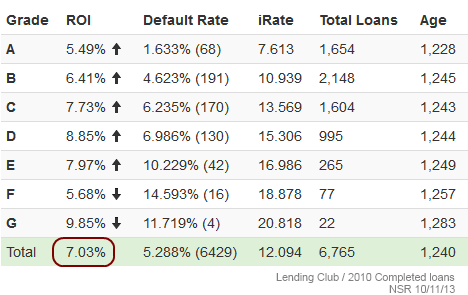

And here is the same table for completed loans from 2010:

While remembering that past performance is no guarantee of future returns, these two tables are quite compelling. Across all loan grades (levels of risk A-G), peer to peer loans have historically given investors a 6-7% return. This return can climb as high as 12% or 13% (see my portfolio) if an investor takes on riskier loan grades and develops a good selection criteria. Read about ways to increase return in my Lending Club Strategy or Prosper Strategy posts.

#2. Trumpet the Growth of Prosper & Lending Club

If anything is easy to applaud, it’s the thundering momentum of p2p lending.

Year after year, peer to peer lending as a whole is going in one distinct direction: up. While only a small portion of Americans today know and understand the nature of this investment, you can bet this situation will soon be different. It has been theorized that peer to peer lending could eventually issue $200 billion in loans. Nobody really knows how high things could go, but if this $200B number is accurate, it means we are not even at 2% of what is possible.

#3. Highlight P2P Lending as an Alternative

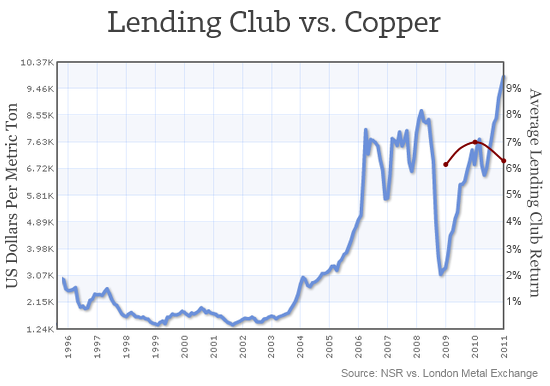

During the financial crisis of 2008, the United States was in a collective tail spin. Not only did the sub-prime mortgage situation upset weighty indices like the Dow Jones Industrial Average, but nearly every retirement account and international market was negatively affected as well. The unified panic exposed how deeply connected everything is. For example, the housing market emergency caused massive shockwaves in things as unrelated as the price of copper (source):

However, the above graphic also shows how much of an alternative peer to peer lending is as an investment compared to everything else. When the sub-prime mortgage crisis sparked a global panic in 2008, and the price of copper dove into 2009 with so much else, the average Lending Club return remained a cheerful 6.1%. Then, as the price of copper recovered to new highs, returns at Lending Club even went down slightly.

This does not mean peer to peer lending is free from risk or negative national factors like unemployment (quite the contrary). However, the above chart is evidence that peer to peer investing is an alternative to the crazy noise that is the global financial system. For people who have assumed that they have no choice besides saving for retirement through mutual funds, this could be wonderful news indeed.

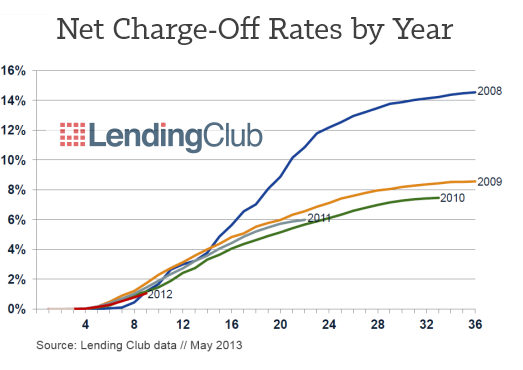

#4. Mention Lending Club & Prosper’s Stability

While we’re on the subject, a great way to convince others of peer to peer lending’s merit is to talk about its low volatility, meaning, how stable the returns continue to be, year after year. People often imagine alternative investments as crazy things that give high returns at one time and low returns at another. Peer to peer lending, on the contrary, is quite the opposite:

The above graphic demonstrates this fact in great detail. It is a screenshot from a presentation Renaud Laplanche gave at the LendIt conference in June, highlighting how the default rates at Lending Club have continued to be amazingly consistent year by year. The default (charge-off) rate is the percentage of the loans that fail to get repaid by borrowers, and this rate has largely stayed the same since 2009. Without making guarantees, this means we are more likely to earn a similar return in 2014 as we did in the past five years.

#5. Forward Articles from the Wall Street Journal

If people struggle to be excited by the returns or consistency, perhaps they will be swayed by press clippings. For instance, you could send them this recent Wall Street Journal article “Consumers Find Investors Eager to Make ‘Peer-to-Peer’ Loans” that includes a peer to peer lending side-graphic. It features great pictures and quotes from Prosper’s management team. Or forward to them this recent article from Business Insider that calls peer to peer lending the nation’s “Hottest New Investing Trend“. Finally, they may be eager to read the recent Forbes article titled “Peer-To-Peer Lending Challenges Too-Big-To-Fail Status Quo“, an article that questions the notion that America actually needs big banks at all.

If people struggle to be excited by the returns or consistency, perhaps they will be swayed by press clippings. For instance, you could send them this recent Wall Street Journal article “Consumers Find Investors Eager to Make ‘Peer-to-Peer’ Loans” that includes a peer to peer lending side-graphic. It features great pictures and quotes from Prosper’s management team. Or forward to them this recent article from Business Insider that calls peer to peer lending the nation’s “Hottest New Investing Trend“. Finally, they may be eager to read the recent Forbes article titled “Peer-To-Peer Lending Challenges Too-Big-To-Fail Status Quo“, an article that questions the notion that America actually needs big banks at all.

#6. Invite Them to Start Small and Exit Easily

Experimenting with Lending Club or Prosper is a somewhat low-commitment act. Lending is easy to try out, and an investor can quit anytime. For instance, most individual investors test the p2p lending waters with a small trial investment. This is quite easy to do, since both Prosper and Lending Club have allowed a minimum note (portion of a loan) of $25. You may not be fully diversified with just a single $25 note (see the benefits of diversification), but you can get a decent sense of the lending process as a whole.

Furthermore, peer to peer lending is a fairly liquid investment. This means you can pull your money out somewhat easily. Peer to peer notes are classified as securities, so a secondary market exists that allows their sale and repurchase. If an investor decides he or she is done, they can liquidate their investment on the secondary market (Foliofn). Often notes sell immediately if priced at face value.

#7. Highlight Peer to Peer Lending’s Simplicity

This is something that has not been talked about enough. Peer to peer lending, unlike investing in stocks, bonds, or mutual funds, is really stinkin’ easy to understand. If you invest in a mutual fund, things can get confusing. Suppose you invest in a Fidelity retirement fund that has holdings in hundreds of companies. After moving cash over from your checking account, your investment would go to purchasing shares of the fund, shares which would be split among hundreds of different companies. Where is your money at this point? Split among hundreds of institutions. For many, this is hard to understand.

This is something that has not been talked about enough. Peer to peer lending, unlike investing in stocks, bonds, or mutual funds, is really stinkin’ easy to understand. If you invest in a mutual fund, things can get confusing. Suppose you invest in a Fidelity retirement fund that has holdings in hundreds of companies. After moving cash over from your checking account, your investment would go to purchasing shares of the fund, shares which would be split among hundreds of different companies. Where is your money at this point? Split among hundreds of institutions. For many, this is hard to understand.

In contrast, peer to peer lending is simple and elegant. You are simply lending people cash. Borrowers either repay you or they don’t. Period. The fees are low and the platform data is transparent. Prosper and Lending Club only make money if their investors do as well. Certainly, there are detail-rich aspects to becoming a good lender (like filtering loans), but overall the process is more uncomplicated than anything around.

#8. Emphasize How Peer to Peer Lending Helps People

If all else fails, it can help to simply talk about peer to peer lending’s ethics. Peer to peer lending is good for the United States. It is good for society. The people who are taking out these loans are generally not reckless individuals with a sudden desire to open a tattoo parlor. Instead, they are premium borrowers with good credit who are generally using their loan to get out of credit card debt. They are moving from the ugly 25% interest rate on their Chase credit card to a peer to peer loan with a more reasonable rate, often 7-15%.

If all else fails, it can help to simply talk about peer to peer lending’s ethics. Peer to peer lending is good for the United States. It is good for society. The people who are taking out these loans are generally not reckless individuals with a sudden desire to open a tattoo parlor. Instead, they are premium borrowers with good credit who are generally using their loan to get out of credit card debt. They are moving from the ugly 25% interest rate on their Chase credit card to a peer to peer loan with a more reasonable rate, often 7-15%.

Have you ever blessed people with freedom through your Roth IRA? I have.

An Investment with a Promising (Though Uncertain) Future

How widespread will peer to peer lending ever become? Will it remain forever an investment option mostly used by those skilled in finance or technology? Or will the average American, fifty years from now, be well versed in the practice and language of lending money online?

I believe the answer lies somewhere in between. The returns are just too consistent and rewarding for this investment option to remain unnoticed. That said, it does take a small degree of know-how and comfort to simply open a lender account and diversify an investment into 200 notes. Lending Club and Prosper may eventually offer public funds, which would help, but the best experiences seem reserved for those who have the time and energy to learn the ropes of peer to peer lending for themselves.

That said, thousands upon thousands of financially proficient independent investors are still unaware that peer to peer lending exists. If you know one of these individuals who continues to be on the fence, my hope is that the eight arguments outlined above will help change their minds.

[image credit: USDA “20120807-OHRM-TEW-8924“/Muffinn “Wholemeal tin loaf”

Rolands Lakis “Mother & Daughter” CC-BY 2.0]

Nice article Simon. As much as I evangelize p2p lending I rarely try to convince my friends to give it a try. I just explain why I am so passionate about it, why I think it is safe, the returns I am getting and then leave it at that. Using a soft sell approach with my friends has led to many of them signing up….and then thanking me later.

Good food for thought. Thanks for stopping by Peter.

“It’s a Viola”?!?! Too funny!

On a serious note, I like to emphasize the “King of Graphs” that LendingClub CEO Renaud often showcases: 30 years of data showing the average interest rate banks charge on credit cards staying the same, and the prime rate dropping like a brick.

Anyone can generate this from Federal Reserve data. Start by googling “Federal Reserve G19” and grab the Historical Data. Then get your choice of bank rates from the H15 report. The gap between these two rates is what private debt investing is all about.

For extra credit you can grab the Fed’s charge-offs data on credit cards loans, which shows how stable those numbers have been (though of course they do rise during recessions, but have since fallen).

The more involved I get in peer to peer lending, the more I realize how important it is to trot out the 30 year graph of credit card rates. Thanks Brendan!

I tried it– I started small, with $3000, an amount that is practically indistinguishable from $0 in my circumstances. Some of the loans have done well, but even though I stuck to A & B notes only (75% A), my return rate after 18 months is around -4%. By contrast, in trading options and holding boring dividend growth stocks, I’ve consistently made money over the past 10 years– INCLUDING during the 2007-2009 downturn.

I told one of my friends about my experience with Lending Club, and he told me the problem was that I didn’t successfully sell my notes as soon as the payment went 30 days late. Maybe… but that is another way of saying I didn’t TRADE them well; if I had somehow unloaded the bad loans before they finally defaulted, that wouldn’t have made Lending Club a good investment, but would only have meant that I got someone else to take a bad investment off my hands, which is a very different thing.

I’ve stopped reinvesting my Lending Club notes because there are far too many deadbeats getting A ratings; I’m far more willing to believe that Pepsico can raise my dividend every single year until I die than I am that some random A-rated borrower will turn out not to be a thief.

Sorry you had such a poor experience Mike. However, on the aggregate, A-rated p2p loans are a remarkably stable investment, and do far more social good than investing in sugary beverages.

If $3000 is essentially equal to $0 given your astounding wealth, a -4% return is nothing as well. You should take pride that some of your loans made a real difference in someone’s life.

Concerning your point about how little of one’s investment in a Fidelity account would reach an Apple employee… WOW. Do you really not get that NONE of one’s investment in Fidelity actually goes to any Apple employees, not even a “sliver” (to use your word)? That’s just not how the stock market works. When you buy a share of Apple (either directly or through a mutual fund), the company Apple doesn’t actually get the money, except in the tiny, tiny minority of cases in which they’re issuing new shares. Generally speaking, when you buy Apple, you’re buying it from some random dude like me who happens to be selling his Apple shares– you’re NOT giving money to Apple.

Aside from that, you’re exaggerating the complexity of the stock market if you claim that Lending Club & Prosper are somehow more simple. Here’s how the stock market works: through a brokerage, you pay a very small 1-time fee to buy shares in a company. E.g., through Interactive Brokers, if I buy 100 shares of Coca-cola, I pay a whopping $1 in transaction costs. Then I hold Coca-cola until the day I die, and they increase the dividend payout every single year like clockwork. Are you really going to tell us that peer to peer lending is more “simple” than THAT? Seriously?

Mike, your points are well made, however there is another way to consider LendingClub vs Coca-Cola on the simplicity front, and that would be to compare a LendingClub note to the financial report for an S&P 500 corporation.

Buying a note from LendingClub or Prosper and holding it to maturity does offer greater transparency of economics than the board-level machinations of even a small US company, where the income of the stockholder owners can be taxed in dozens of ways through bloated payrolls, failed mergers, large options grants to insiders by board-controlling CEOs, consulting agreements, arbitrary bonus decisions, huge debt transactions and their servicing fees so as to hoard cash and avoid a takeover, etc.

There is an elegance in P2P lending that harks back to the earliest debt transactions of our species. Simply lending money and getting paid back does make a lot of sense, and perhaps more (to some people) than a bet on the future cash flows of a Fortune 500 company, itself one of the most complicated legal entities that any civilization has ever known. Never mind that Coca-cola’s value proposition is to disguise carbonated poison as ineffable happiness.

Better said than myself. Thanks Brendan. See you in a few weeks, I assume.

Regarding #7, a mutual fund investor’s money is not split amount hundreds of different companies. Mutual fund investors do not actually own the securities in which the fund invests; they only own shares in the fund itself. Mutual funds are simple to understand, you just need to do your research, the same with peer to peer lending.