Anybody who has been an active investor in peer to peer lending for longer than six months will have experienced an interesting phenomenon. The percentage of their return on investment will explode out the gate during the first couple months. After all, the average interest rate for loans at Lending Club is around 14%, so an investor’s returns in the first month or two mirror this number. For many investors, discovering a 14% ROI hidden outside mainstream investing can involve a great deal of excitement. People see a double digit return on their Lending Club or Prosper account and rush to tell friends, creating informal investor blogs to celebrate their discovery.

Here’s something people don’t talk much about: the corners of the internet are full of stale p2p investor blogs.

Now, many of these folks simply run out of things to write about, which is understandable considering the simplicity of this investment. But for others, the tale is more edged. Their bright elation turns dull when they experience a string of defaults within the first year. Suddenly their peer to peer lending experience stops being the techie suave discovery they assumed it was. Mojo lost, they resume life as usual.

Why Are My Lending Club Returns Going Down?

I want to talk today about what it means to have realistic expectations around this investment, specifically highlighting peer to peer lending’s return curve. We need to remember that these are not really notes but people that we have entrusted our money to – people with lives full of uncertainty, people who are always at risk of being unable to make their payments no matter how strictly we filter the platforms beforehand. Defaulting borrowers will have a dramatic negative effect on every investor’s portfolio, full stop, and we need to be ready for this.

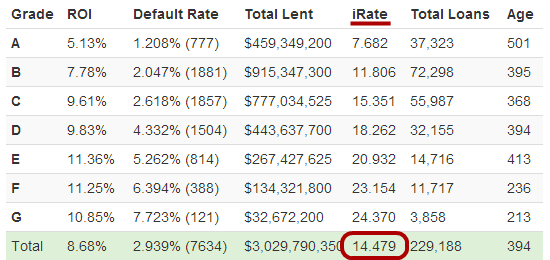

Average Interest Rates at Lending Club

To begin, let’s focus on where returns begin, which is the average interest rate of the loans that Lending Club & Prosper issue. We can easily find these rates for Lending Club by going to the Return Forecaster section at NickelSteamroller. If we isolate all loans issued since SEC approval, we get the following chart:

The circled number is the average interest rate on the $3 billion in loans that Lending Club has issued since January 2009. If you look above it, you can see how each loan grade (A-G) has increasingly higher interest rates. This 14.479% is our starting place. Minus 1% in investor fees, it is a decent place to understand the p2p lending return curve.

People who are brand new to investing in Lending Club will often have a return (or NAR – Net Annualized Return) that tracks with this number. As mentioned above, this can be a pretty exciting time. After all, what investments across the web offer a consistent return north of 10%? Probably none. Furthermore, if an investor manages to snag a decent number of the riskier D-G grade loans, their initial return can be quite sensational – sometimes above 20%.

The Impact of Defaults on ROI over Time

This initial return on investment, often 10%-20%, is inflated because borrowers have not had the chance to default on their loans. To demonstrate, let’s imagine that the first note you purchase is in a 36-month loan at Prosper. Imagine the borrower immediately takes their loan, withdraws it in cash, and loses it on the roulette table in Las Vegas. Then imagine that, in a breathless string of bad judgment, they go on that evening to get arrested, eventually getting sentenced to 36-months in prison.

This initial return on investment, often 10%-20%, is inflated because borrowers have not had the chance to default on their loans. To demonstrate, let’s imagine that the first note you purchase is in a 36-month loan at Prosper. Imagine the borrower immediately takes their loan, withdraws it in cash, and loses it on the roulette table in Las Vegas. Then imagine that, in a breathless string of bad judgment, they go on that evening to get arrested, eventually getting sentenced to 36-months in prison.

In this situation, having a broke borrower who has no ability to make their payments, you are highly unlikely to get your investment back. Yet four months will go by before this loan officially defaults – four months where your portfolio may deceptively seem more stable than it actually is. Furthermore, this will probably not be an isolated incident. Most investors, myself included, will have a number of notes in their portfolio that seem fine but actually are four months away from being lost. As written of previously (see: P2P Lending Default Rates), having borrowers default is unavoidable for every investor who is diversified in 200 notes.

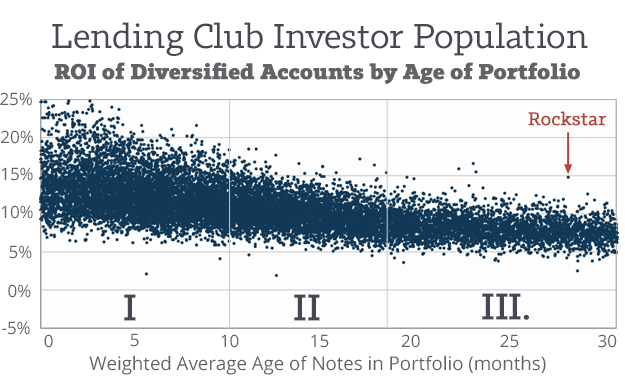

Lending Club recently launched an amazing graph that shows all of the returns of their investors splayed by account age (at least, those who are diversified and not on Foliofn). This graph is brilliant at demonstrating the return curve of this investment class.

This graph communicates a few very powerful truths. For starters, it reveals the revolution that is happening online within peer to peer lending. Thousands of investors are involved in this exciting new asset class. Secondly, this data beautifully demonstrates how defaulting borrowers form a return curve over time for every investor. And we’re all experiencing this! Each little dot signifies an investor who is doing the same thing as me and you – (1) picking hopefully-worthy loans and (2) experiencing a portion of these loans defaulting over time.

The Three Seasons of the Return Curve

I have divided the return curve up into three different sections, three seasons that every newborn portfolio will experience before it reaches stability.

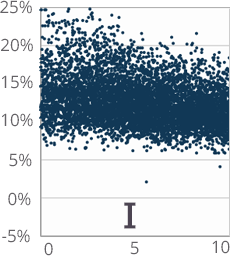

Season I (1-10 months)

This season begins with no defaults, just blissful returns. An investor’s ROI tracks closely with the average interest rate they invested in. For most investors, this season can be marked by an initial return of 10-20% depending on the loan grades that have been taken on. However, month four will find most accounts hit by their most intense default rate (See: NSR | Default Count of 36 Month Loans vs Age).

This season begins with no defaults, just blissful returns. An investor’s ROI tracks closely with the average interest rate they invested in. For most investors, this season can be marked by an initial return of 10-20% depending on the loan grades that have been taken on. However, month four will find most accounts hit by their most intense default rate (See: NSR | Default Count of 36 Month Loans vs Age).

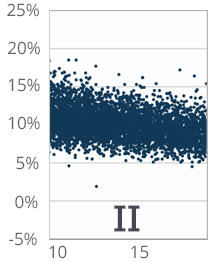

Season II (10-18 months)

Since ten months have elapsed, every account will have experienced the majority of its defaults. Anil over at Random Thoughts has a great post demonstrating this in statistical detail, and it makes sense. People who are unable to repay their loans (either from being strapped for cash or through irresponsibility) will most likely reveal this condition sooner rather than later. Prosper agrees with this principle, saying that an account’s returns are not seasoned until 10 months have passed.

Since ten months have elapsed, every account will have experienced the majority of its defaults. Anil over at Random Thoughts has a great post demonstrating this in statistical detail, and it makes sense. People who are unable to repay their loans (either from being strapped for cash or through irresponsibility) will most likely reveal this condition sooner rather than later. Prosper agrees with this principle, saying that an account’s returns are not seasoned until 10 months have passed.

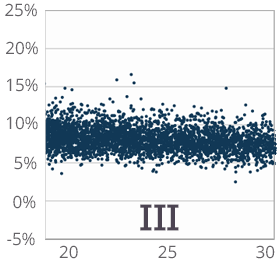

Season III (18+ months)

By this time, the majority of defaults have happened. The most unstable borrowers have had a chance to default on their loans, and you can see it on the graph to the right. While there is still a small bit of loss after eighteen months, the returns for most investors have stabilized between 5-9%. Historically, this is our expected return. This is the number we should be quoting prospective investors who are interested in getting started.

By this time, the majority of defaults have happened. The most unstable borrowers have had a chance to default on their loans, and you can see it on the graph to the right. While there is still a small bit of loss after eighteen months, the returns for most investors have stabilized between 5-9%. Historically, this is our expected return. This is the number we should be quoting prospective investors who are interested in getting started.

Conclusion: Three Takeaways

After looking at this graph, there are three things to remember regarding our peer to peer lending investment.

#1. Keep realistic expectations. While the initial returns we experience as investors can seem exciting, they are almost guaranteed to go down with time. For example, my first return on this site had me pegged at a 19% ROI. This return, while fun, was unsustainable. Despite savvy filtering of the platforms, despite investing in loans with an average interest rate of over 20%, my return has fallen almost ten percent since it began. My experience is typical for any investor, but especially for those who invest in low-grade notes – the fall is more precipitous than if one sticks with safer A or B-grade notes. That said, to maintain the surfing metaphor, I enjoy the big waves.

#2. Expect a large drop to happen in the first 10 months. Prosper’s approach to seasoned returns coupled with investor research by statisticians like Anil Gupta reveal that the majority of defaults happen within the first 10 months. In this way, it can be helpful to focus during this time, not on your return, but on keeping idle cash low, using historically trustworthy filters to create a diversified peer to peer lending investment.

#3. Heartily celebrate your portfolio’s overall return once 18 months have passed! Good job – you earned it. Any notes over 18 months old and with a Current status are quite likely to stay that way. Call a friend for beers at the local pub, for you have become a seasoned peer to peer investor.

[image credit: Minoru Nitta “locals“/ Håkan Dahlström “Roulette wheel” CC-BY 2.0]

As a side note, most of the data that supports this post came from research involving 36-month loans. That said, 60-month loans seem to be tracking along the same path.

How much higher is the default risk over 60 versus 36 or is it the same after 18 months? Seems like there much be higher risk with longer term.

Hi Michael. It’s definitely higher. See the latest 2014Q3 returns post.

Nice read, enjoyed the part about stale p2p lending blogs. I try to tell my friends about p2p lending and they just ignore me. Fortunately, we have our blog to share with others and a community of people like you who are passionate about it. I’m still in season 1 and have finally seen my first late notes. I’m curious if you are automating your investments using a tool yet, feel free to email.

Very well written Simon. Understanding the downward trend for returns is crucial for new investors to develop. Nothing is more disappointing for new investors and a big turn off for future dollars than realizing you aren’t making as much as you thought you were.

As you’ve mentioned in your comment, it will be interesting to see how things continue to develop as the 60-month notes continue to age, even as they track along a similar path.

Great article! I loved seeing that graphic on the Lending Club website because it gives people an expectation of where they will be… Which is not around the 16%+ they were at in the first few months of their accounts.

Great article. I haven’t tried peer to peer lending myself, but this is some nice data about expectation setting.

Thanks Simon. P2P has been a welcome diversification of our sizeable portfolio of stocks, options, real-estate, Tbills, Munis, and cash. Making 9.5% steady with no defaults after 1 year. Filters rock!

R,

Fred

Another good article Simon. I wonder if the average ROI would actually increase a little if you extrapolated that data further, as it would seem plausible that loans are less likely to default after 18 months (start of Season III), especially for 36 month loans. So once the defaulted loans are weeded out earlier on, the remaining loans with higher interest rates will bring the average back up some. Just an observation from an amateur.

Being in Alaska, my only trading option is through Folio. Though initially disappointed by that, I’m now wondering: Folio allows me to buy discounted notes, and filter them for never late and seasoned. Seems like that’s an advantage over initial loans. Any thoughts?

Hi Laren,

(Finally getting to your comment after the holidays)

Folio presents a whole bunch of advantages over simply funding notes from the start – the main one you touched on, which is filtering for loans that have never had a late or missed payment. However, you will probably pay a premium for them. The reason investors like myself enjoy funding notes from the start is the ability to get them at cost, without paying a premium. This, of course, means we take on a bit more risk, but the overall return seems worth it.

That said, you can lower the volatility of your portfolio dramatically if you buy Foliofn notes that have perfect payment histories.

I usually only purchase through folio; however, sometimes I look at the new notes.

What I don’t like with new notes is the time to fund doesn’t earn you interest. And there’s rarely a history established. And sometimes they don’t fund at all.

I have not had a problem buying notes at a discount, I think there almost always is a surge from someone dumping their portfolio at a discount just because they had a default.

Thanks Keith. Wise words.

I have been trying to visualize my Prosper portfolio on the LC graph since it was published a few weeks ago. The X-axis (time in months) has me confused. I have been lending on Prosper since Oct of 2012 at a steady rate for the last 14 months. This is a very regular thing with me, like brushing my teeth. So my ~1,000 notes are very evenly spread over the last 14 months. Prosper shows my returns as “Seasoned Only 13.07%” and “All Notes 10.31%”. Although I have read the definition of this a number of times, I still don’t fully understand it. I estimate about 200 of my 1,000 notes are over 10 months old and fall into the definition of “seasoned”. So my question is, where on the graph would I place my dot? Thanks to whoever that answers.

SeattleSun

Hi Seattle Sun. If 200 of your notes are over 10 months old, then your seasoned return is the return you are earning on them.

Your dot would be placed on the X-axis of your overall portfolio age. In Prosper, you can find this number on the View Details link of your account screen. Scroll down the page until you hit the Annualized Return by Purchase Period section. Here you will see “Average Note Age”. Take this number of days, divide it by 30 (30 days are in a month) and you will see where on the X-axis you would place your dot.

Hope this helps,

Simon

Has the menu layout changed on the Nickel Steamroller site? I’m trying to follow along with your articles while using NS and having issues….for example, you mention the “Return Forecaster” section of NS in the article above, but I’m not see that in the menu anywhere on NS……any additional clarification would be appreciated…..thanks.

I too felt this I was riding high at about 16% ROI! And then boom default! I plunged to 6.5% ROI I’ve slowly worked my way back up to 9% I’ve also focused on reducing my risk. I have approx 250 notes I review my account 5 times a week watching for any signs of default I have a guideline in grace period or late 3 times and your being sold off. When I sell my note my goal is to get my principal back. Its no longer about making money its about protecting my money. Making nothing on a $25 note is better then losing $10 of that $25.

Also if the note is a lower APR I’m more likely to sell as I’ve come to believe higher APR notes are where the money is at.