A few weeks ago I had the opportunity to sit down for a conversation with Lending Club’s founder Renaud Laplanche. I had briefly met him before, but this was the first time we were able to sit down and connect. I walked away from this discussion with a deeper respect for the integrity of this company and how they aim to transform banking as we know it.

Interview with Lending Club’s CEO

Just how big is peer to peer lending? What is the saturation point?

We could talk about a saturation point for the product currently offered by peer to peer lending companies, but that seems to be somewhat restrictive in its scope. What Lending Club is actually doing is transforming the banking system. Unsecured personal loans were really our first product, but that is not at all the full extent of where we want to go. We plan to develop all types of credit products, whether it is consumer loans or business loans. In the consumer category this includes student loans, car loans, and mortgages. If you include all these products, the consumer loan market is in the trillions of dollars. There is $12 trillion in mortgages alone, and if you then start including international markets things get even bigger. In short, there is no saturation point, no practical limit for how big this could get.

But limited to personal loans…

In the current market, product, and geography, Americans have $850 billion in credit card debt that could be refinanced by a personal loan at a lower rate. About 40% of that, $350 billion, meets our credit policy. In terms of large issuers of personal loans in this country there is only Lending Club, Wells Fargo, and Discover, so I think we could capture a decent size of that market.

Considering most of these loans are from people paying off their credit cards, won’t Lending Club be impacted by this national trend where more and more people are paying off their debts?

National credit card debt has actually gone down very little, from $900 billion in 2008 to just $850 billion today, and most of the reduction came from charge-offs in 2008 and 2009 rather than consumers actually paying down their balances. Basically, these borrowers could not make their payments, so $50B of their debt was simply written off.

So little has actually changed.

That’s correct.

Are you worried about the credit card companies realizing that there is this opportunity to be had, that they are missing the boat? What if the banks could lower costs and increase their efficiency to match Lending Club’s? What is to stop JP Morgan Chase from cutting you out through doing all this themselves?

Culture.

Culture?

Yes. If you look at the history of innovation, there are very few examples of that happening, of incumbents reducing their cost structure and out innovating the low-cost technology-based entrant.

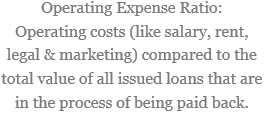

Let’s highlight some numbers around our cost advantage compared to the banks. The operating expense ratio for banks is between 5-7%. Ours is below 2% and trending lower every quarter. We have this 5% cost-advantage that we can pass on to our customers, so it is really hard to see how banks could compete.

Let’s highlight some numbers around our cost advantage compared to the banks. The operating expense ratio for banks is between 5-7%. Ours is below 2% and trending lower every quarter. We have this 5% cost-advantage that we can pass on to our customers, so it is really hard to see how banks could compete.

There have been many examples of this happening before, whether it was when Borders could not react fast enough to Amazon or when Blockbuster could not react fast enough to Netflix and eventually went bankrupt. There have also been many attempts at companies trying to survive by spinning out low-cost operations. Ten years ago, because of pressure from Southwest and Jet Blue, all the major airlines spun out low-cost alternatives. Delta launched Song; United launched Ted. But these alternatives ended up having exactly the same cost structure. Despite their best efforts, they kept the same culture.

Why would it be so difficult for JP Morgan Chase to institute a culture-change?

There are three factors. There is the physical infrastructure – the branches. It would be really hard for JP Morgan Chase to close 5,000 branches overnight.

Furthermore, Lending Club runs our entire operation on a nimble server farm in Nevada, a setup that has the same piece of code running on every single machine. Our platform was purpose-built. It does exactly what it was designed to do and nothing else. In contrast, the banks all run on disparate systems that came with the mergers of other banks, many built twenty-five years ago. Getting all these legacy systems to a place where they could run like ours, getting them to use technology that was developed in the past two years like we do, this is almost impossible.

The third and most important aspect is really cultural. The kinds of people who come to work at Lending Club are those who say, “I want to transform the banking industry. I want to create something new and innovative.” With a very different talent pool you end up with a very different outcome.

During the 2008 financial crisis you still managed to deliver profit to your investors. How did you do that? How did you deliver a 3.8% return in the middle of economic catastrophe?

Part of it is our stringent credit policy, where we set the dial regarding the minimum requirements for a loan, like an applicant’s FICO score. Overall, I think we have a more conservative approach than other companies. People sometimes make trade-offs between originations and credit quality, but predictability in our loss rate is our main asset. It is what we are recognized for. It is why investors come to us, and we cannot mess with that. Each time we have to make a decision, we have decided in favor of the quality of our loans, and I think that shows in our track record.

Marc Prosser at Forbes recently wrote an article that highlighted how peer to peer lending is uncorrelated from the swings of the stock market. Might this independence also have helped?

Well, not all of consumer credit is uncorrelated. If the economy slows down then more people lose their jobs. But the people who are the most exposed to these economic conditions typically have lower credit, so the tighter our credit policy, the more liberated we are from the swings of the economy.

Remember, in a 2008 environment our returns went down as well. So we are not totally uncorrelated. But we still did better than a lot of other debt instruments. I think we can put it this way: prime consumer credit tends to perform well in any economic cycle.

My dad is a retired environmental scientist who, like many Americans, had a workplace that designated him a mutual fund for retirement. Why does American retirement continue to prefer mutual funds instead of the more reliable returns within premium consumer credit?

Changes take time.

Do you think the nation will switch over?

Yes. I think we are going to be a part of every asset allocation within the next 10 years. No one should invest 100% of their assets in consumer credit, but I think many investors will consider it a share of their asset allocation, the same way that there might be a share of cash, stock or corporate bonds.

Google made a $125 million investment in Lending Club six months ago. How has your new relationship with Google affected the company?

There are a number of projects we are working on together that are not public, so we can’t talk about them. What we can mention is how eager they have been to help. We had several brainstorming sessions with them on marketing, not just on search engine optimization but also some really interesting discussions on branding and security. Google, being Google, has been exposed to more security threats than anybody else out there, so their help on that front is really productive. Finally, we were able to talk to quite a few of Google’s managers who experienced the same fast growth seven years ago that we are experiencing now, and they shared some of the things that worked for them.

Interestingly, there is a lot of alignment between Google and Lending Club in how we see the world and how we see ourselves. Google has used technology to lower cost, deliver a better experience, and empower the end user. They transformed publishing and advertising. All that is very aligned with what we are trying to do in financial services. We are using technology to lower cost, empower investors and borrowers, and transform banking.

Let’s switch topics and talk about the average retail investor, the people who frequent LendingMemo. Their experience has changed a lot over the past year. What happened?

The platform became larger. We built up a lot of credibility with institutional investors, and this larger institutional base created competition. We welcome these institutions because they helped us grow in a lower-cost way than retail investors. Institutional accounts are more concentrated, so they are not as expensive to service, and since it is a bigger pool of capital the loans get funded faster, so it is good for borrowers because they get their loan funded immediately.

But at the same time we want to preserve a vibrant individual investor base, because it is very diversified and predictable. It is really important for us to preserve that. We now have agreements with 95% of institutional investors that help us limit them on a monthly basis in order to make sure there are plenty of loans left for retail investors. By the end of this year or early next year, I think we will have a better balance and more loans available for retail investors. That’s our goal.

Do you ever see Lending Club expanding its loan grades, either to super-premium AA or high risk HR-grade loans?

We are always trying to be more helpful to more people, to broaden the scope of what we are doing. Insurance, pension funds, and banks are coming to us looking for a 2-3% return target, so we could start making AA-grade loans at a 3.99% interest rate, a loan that would attract borrowers with an 800 credit score and long credit history. On the riskier side, we are also testing our expansion, but it is a lot more dicey. This is the type of population that would be the most exposed to an economic slowdown.

My average site user probably invests $12,000. How do you see the experience of this investor changing in 2014?

It seems that we have solved our low-inventory problem, so there are more loans to choose from. We are developing better account reporting tools – more analytics and ways to slice up and understand your return. We are working on our statistics page, and are doing a large overhaul on the Foliofn secondary market.

In the past six months, what are some frustrations you have experienced?

Well, I think it is really hard to keep hiring good people, to resist the temptation to simply hire whoever will get the job done. We have resisted it and kept hiring standards high, because I think that is how we will have really great people working here. But we have seen a lot of companies going public, having no cash constraints and just throwing tons of money at candidates. The environment in Silicon Valley has become such that there has been an over-inflation in salaries, making it harder to hire really talented people, or losing them for the wrong reasons. We know they would have done great here, but they can succumb to the temptation of simply making more money elsewhere, so that’s frustrating. What I like is people coming to work here who have conviction, who love what we do and who want to be a part of it.

What are some of the ethical situations you have had to face?

Most banks and lending companies often have to make decisions where, on the one side is the interest of the customers and on the other side is their own profits. I think these are tough calls to make. If I had to single out one thing I am the most proud of over the last six years, it has been the decision to constantly be the good guys of banking, how we have always decided in favor of our customers.

Can you give me an example?

(pause) We could take advantage of the current investor appetite, right? The reason why you cannot invest as easily as you would like is because there is a lot of investor interest right now, which means we could increase fees. But we decided not to. Despite having plenty of opportunity to increase fees we said, ‘No, let’s keep delivering great returns to investors.’ Also, recently we had made a display error in a small number of accounts, and decided to credit the investor accounts for the difference.

You mean Lending Club’s recent credit miss?

Correct. These are the kinds of decisions that are hard to make, but I am very proud of the way we made them.

What is your favorite part about Lending Club?

The fact that it is working. This began as a PowerPoint presentation seven years ago…

… a Facebook application.

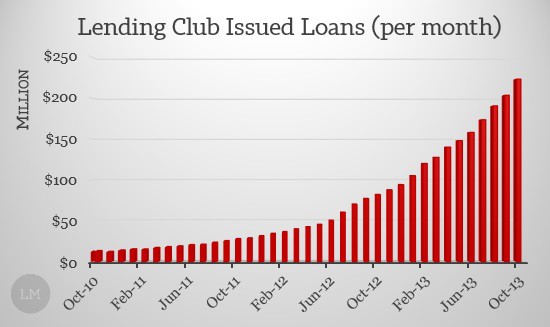

(laughter) Exactly. We had differing ideas of how to launch it, what would and would not work. But the fact is we are here. We have three hundred people now, and will make $2 billion in loans this year as one of the largest issuer of loans nationwide. Yet what is even more exciting is the potential of where we are headed. I feel that our competitive advantage compared to traditional banks is really long lasting because, again, it is grounded in technology and cost, not something they can react to. The amount of debt that American families are carrying is really huge, so the opportunity to make an impact and help people is really tremendous.

Fantastic article Simon. I learned several new things here. Interesting that he thinks the addressable credit card market is $350 billion. That is higher than I have heard before. Anyway, great job.

Thanks Peter. I am curious what portion of this addressable market he realistically thinks Lending Club can capture. What do you think?

One can only guess but I think they are going after a large percentage of that market – at least 25% and probably closer to 50%.

Great interview, without a doubt there are some new things to be taken from this. I, for one, have one of the accounts affected by the error, although I’m not even sure what really took place. To be honest I didn’t realize I had gotten the credit until I was taking a closer look at my account.

I am very interested to see what the significant overhaul on the Foliofn platform will look like, as well as how things will move forward for investors as we turn over into the new year. I love looking at numbers, so it will be nice to see what sort of improvements come out with an updated statistics page as well as additional means to view our own performance.

Thanks Adam. What month did this take place? I’m interested to check out my own statements.

The credit hit my account in August 2013. Let us know if you were affected as well.

Enlarge

Nice explanation there on the statement. Thank you for sharing Simon.

This is somewhat refreshing. I was just thinking to myself how few loans are on Prosper and Lending Club right now. I just checked Prosper and only ONE loan was above 10% out of 33 available loans. It is good to know that Lending Club is keeping the consumer in mind and focused on the end user experience as opposed to just squeezing us for every penny they can get. I did have some display issues with my account as well (September) which Lending Club could never give an explanation for. I’ll have to keep a closer eye on things. After reading this interview I have a renewed admiration for the future of P2P lending. Have you tried the Foliofn service? Any thoughts on that?

I wonder if the Dreamforce conference and cloud integration movement in large firms is on their radar. Integrating Legacy servers is indeed tough but if that would reduce operating costs by a flat number and bring consistency throughout the network I think large institutions would be more than willing to look into a solution by box.com or a similar cloud co.

Thanks for the comment Garrett. While I think some steps like this could be made, I agree with Renaud that doing so would be an almost impossible task. You can bet the banks will try their best though.