A lack of strategy is one of the most common problems new investors face at Prosper. Once someone has opened an account and transferred funds over from their bank account, it can be confusing to figure out what to do next. This problem is easy to see in the variety of success that different people experience on at Prosper. Some lenders thrive while others lose money. So what is the difference between the two?

Today we will examine six important strategies the average investor can use to achieve solid returns on Prosper.

#1. Diversify Your Investment

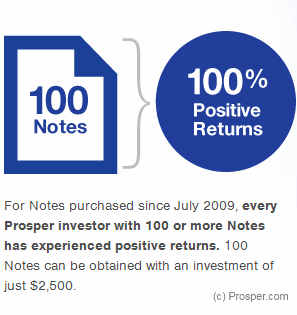

The most important thing you can do to get a great ROI (return on investment) at Prosper is to diversify your account in 200+ notes. Prosper has stated, “Our lender data indicates that the single most important factor in achieving consistent returns is exposure across multiple notes.” In a study I did in February of Prosper lenders who were invested in 200+ notes, only four out of 3800 lenders lost money. In the graphic on the right, Prosper even purports that, when the subset from 2009 are isolated from the rest of the group, not a single investor has lost money who had been invested in 100 notes or more.

The most important thing you can do to get a great ROI (return on investment) at Prosper is to diversify your account in 200+ notes. Prosper has stated, “Our lender data indicates that the single most important factor in achieving consistent returns is exposure across multiple notes.” In a study I did in February of Prosper lenders who were invested in 200+ notes, only four out of 3800 lenders lost money. In the graphic on the right, Prosper even purports that, when the subset from 2009 are isolated from the rest of the group, not a single investor has lost money who had been invested in 100 notes or more.

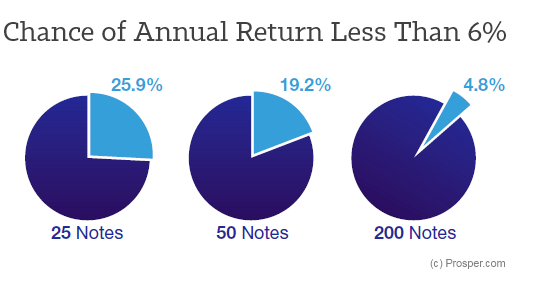

This concept is outlined well in the charts below. The more notes you have, the greater of a return you are more likely to earn (source via LendIt2013):

Aside from investing in 200 notes or more, you can further diversify your account by investing in:

- Notes of differing vintage (late 2013, early 2014, late 2014, etc.)

- Notes of across different loan grades (AA-HR)

- Notes on additional platforms (open an account @ Lending Club)

Read more: Diversify Your Account Like a Pro

#2. Reinvest Returns into More Loans

As loans get paid back, available cash will begin to build up in our account. This uninvested cash earns no interest just sitting there, so we have to keep reinvesting it into additional loans. It is important to establish a rhythm to log into your account and regularly do this. This rhythm will be different for everybody, but once a week might be a good starting place. Of course, it helps to do this when Prosper adds new loans to their platform: 9am & 5pm on weekdays, and noon on weekends (pacific standard time). This way you will have the most variety of them to choose from.

Prosper’s Automated Quick Invest option (read more) is a great way to stay reinvested, especially if you are investing in the less competitive, lower risk AA-C grade loans. After setting up your search parameters (as simple or complex as you want), the tool will automatically invest any available cash for you into additional notes without you having to log in at all. Simple.

Read more: Fight the Mud of Cash Drag with Automated Investing

#3. Invest Through a Prosper IRA

Alongside the phenomenon of compound interest is the wonder of tax-free investing. While peer to peer lenders often forfeit a solid portion of their investment to taxes, Prosper helpfully offers their lenders the ability to open a self-directed IRA (regular or Roth) or roll over a 401k.

Alongside the phenomenon of compound interest is the wonder of tax-free investing. While peer to peer lenders often forfeit a solid portion of their investment to taxes, Prosper helpfully offers their lenders the ability to open a self-directed IRA (regular or Roth) or roll over a 401k.

The benefits of a peer to peer IRA are awesome. Say you are 35 years old and open a Prosper IRA with $5,000, adding just $500 per month that grows at 10%, closing it when you retire at age 65. You would earn $1,074,000. If you used a taxable account all those years and were in a 25% tax bracket, you would only have $664,000. That is a difference of $410,000 just for filling out a couple forms back in 2013.

Read more: Retire Well with a Lending Club or Prosper IRA

#4. Filter Prosper’s Available Loans

Prosper does a great job in their underwriting, denying unsafe borrowers access to a loan while approving those who are more trustworthy. To boot, we can help our returns by doing a bit of extra filtering ourselves. Filtering loans is probably the most complicated part of peer to peer lending, but it can often be worth the extra effort. For instance, borrowers with a public record (like a bankruptcy) are often less likely to pay their loans back.

A great way to begin is by filtering the platform for borrowers with:

- Higher income

- Longer employment history

- No public records (bankruptcies, liens, etc)

- Fewer inquiries

However, the above list is really just scratching the surface. Filtering your loans is a skill that you can get better at over time, involving numerous tools such as NSRPlatform’s Prosper analytics tool. You can learn more through this introduction to filtering, this series on filtering, or by downloading my free p2p lending eBook (15 pages devoted to filtering loans).

However, the above list is really just scratching the surface. Filtering your loans is a skill that you can get better at over time, involving numerous tools such as NSRPlatform’s Prosper analytics tool. You can learn more through this introduction to filtering, this series on filtering, or by downloading my free p2p lending eBook (15 pages devoted to filtering loans).

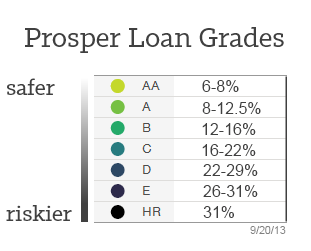

#5. Include Riskier Low-Grade Loans

Most lenders start out safe by investing in AA-B grade loans. However, eventually they realize the benefit of adding riskier low-grade loans to their account. AA-grade loans earn us only 6-8%. Compare this to D through HR-grade loans which earn 22-31%. The default rate is certainly higher for these riskier loans, but the high interest rate can often than make up for it. Of course, the added risk should not be taken on if your investment style needs more safety. For instance, if you are approaching retirement then you may want to minimize the number of riskier loans you invest in.

Most lenders start out safe by investing in AA-B grade loans. However, eventually they realize the benefit of adding riskier low-grade loans to their account. AA-grade loans earn us only 6-8%. Compare this to D through HR-grade loans which earn 22-31%. The default rate is certainly higher for these riskier loans, but the high interest rate can often than make up for it. Of course, the added risk should not be taken on if your investment style needs more safety. For instance, if you are approaching retirement then you may want to minimize the number of riskier loans you invest in.

Note: Getting these lower-grade loans is competitive. Many lenders (some armed with fast APIs) are quite eager to earn these higher returns. If you want a shot at funding these loans, will need to log in when new loans are added to the platform: 9am & 5pm PST (noon on weekends). It can be a bit of a feeding frenzy, but the higher return can make up for your trouble.

I only invest in D, E, & HR-grade loans because I am younger and can take on that risk. So far, that approach has worked well for me (see my portfolio).

Read more: Filtering for Low-Grade Loans

#6. Stay Updated and Informed

Peer to peer lending is only just beginning. Prosper, while showing great strides in 2013, will certainly go through more changes in the coming years. For instance, just a year ago their Automated Quick Invest tool worked great to fund D-HR grade loans. Now this is no longer the case. There has been such a demand for loans that everybody has had to adjust their lending practice.

It is important to be aware of the risks of investing with Prosper (see this article). It can be helpful to subscribe to industry sites like Prosper’s blog, a place where Aaron Vermut continues to communicate the changes Prosper experiences as it continues to grow. Lender operated sites like LendingMemo & Lend Academy are helpful as well. Although the future of peer to peer lending is unknown, its changes will take lenders less by surprise if we remain active in the conversation.

A Warning: You May Get Addicted

One of the more interesting peer to peer lending articles this year was Sam of Financial Samurai writing about his experience as a Prosper lender. He spoke of how much he enjoys reading the different loan descriptions, funding the ones that meet his scrutiny. I have to admit that Sam captures the lending experience well. Being a regular investor over at Prosper has continued to be a wonderful (and sometimes addictive) experience. I always enjoy logging in to watch my account balance grow month by month, knowing that this growth is the result of using the strategies listed above.

[image credit: Stefan Erschwendner “Strategy”/Philip Taylor “Roth IRA” CC-BY 2.0]

If you have $1000 to invest, would you still recommend D, E, and HR rate? My inclination was to go with B-D rates until my total investment was closer to 100 notes.

$1000 is not enough to invest in peer to peer lending. You need at least $2000 which will allow you to start with 80 A-grade notes. See the “How to Try P2P Lending” article in the sidebar.

That is interesting advice. I would think investing in only A-grade loans wouldn’t give you very good returns (less risk, less reward).

I understand the 200+ notes is the ideal. But imagine you purchased those 200 notes over a few years rather than immediately. Wouldn’t you still invest in lower grade loans?

It seems strange to say the first $2000 would go to all A-grade loans, then after that, start diversifying.

I started with $200 in Prosper, and I’ve built on it over the last 6 months. I anchored myself with A-B loans, then started to expand into certain C loans after 10-12 notes. I’m currently at about $1000 ($25 profit), 40 notes and now have two thirds of my loans in B-C (with plans to go riskier)

I’d start when you can and just play it safe while you learn the system. Once you’re comfortable, go a little riskier and see where it takes you. If someone’s profile is glistening, you may be willing to dump $25 into a D or E loan off the bat. Just enjoy it

Just be aware that $1000 is not enough to be fully diversified. You generally need at least $2000, and that is if you stick with AA-grade notes at Prosper. $5K with all grades. Read the “How to try P2P Lending” article in the sidebar.

The original article is from September 2013. Would you say the same strategies are still applicable today. I borrowed from both lending club and Prosper in the past (all paid back) and in a position to now invest. Looking for increasing the account, but also looking for various monthly cash flow options. I’d appreciate your feedback, thanks.

Hi Richie. Yes, all of the strategies are still valid. Cheers, Simon

Thanks. Do you have any other ideas for cash flow investment options?