Each quarter I post the current state of my peer to peer lending accounts. I am a lender who enjoys maximizing my return through fine-filtering the riskier loans. I opened my first account in September 2011, and have opened two more since then.

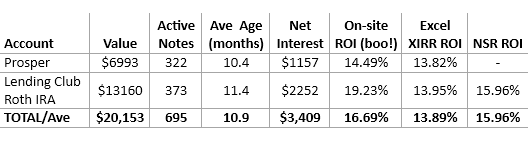

As you can see in the following table, I continue to celebrate positive returns on both Lending Club and Prosper.

Figuring Out ROI Can Be Tough

Calculating your peer to peer lending ROI (return on investment) is tricky business. If you want the easy route, both Lending Club and Prosper offer you their typically inflated number. If you calculate the rate yourself using the Excel XIRR function you get closer, but this still does not take into account any notes that have gone late (and are, as such, no longer worth their full value). Michael’s Portfolio Analyzer on NSR includes a reduction from these late notes, but does not do well with loans bought or sold on the secondary market, so this is the last quarter I will be including this figure. I have included all three ROIs above for comparison’s sake (see my analysis of calculating XIRR return).

Accounts Breakdown

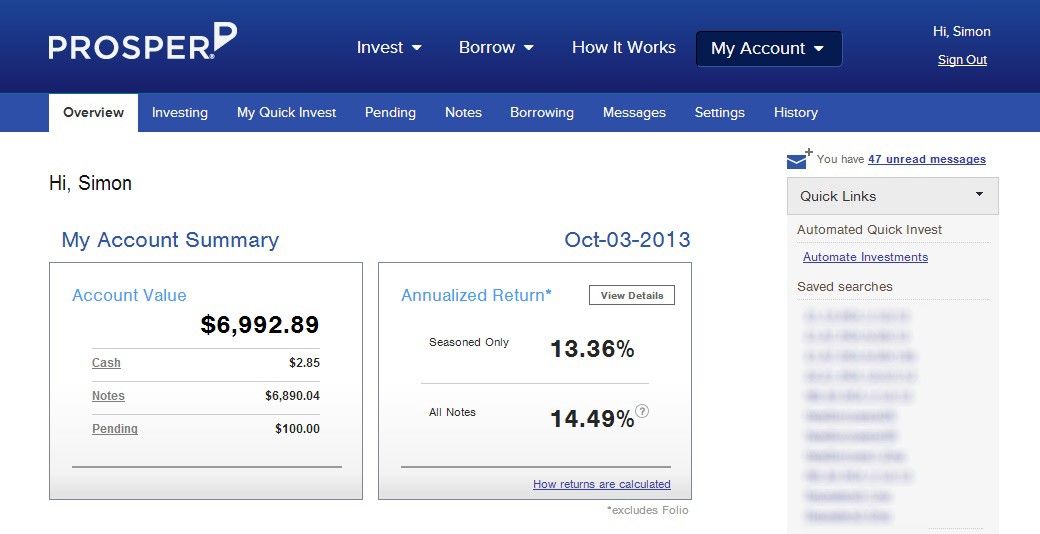

#1 – Prosper Taxable Account (13.82% return):

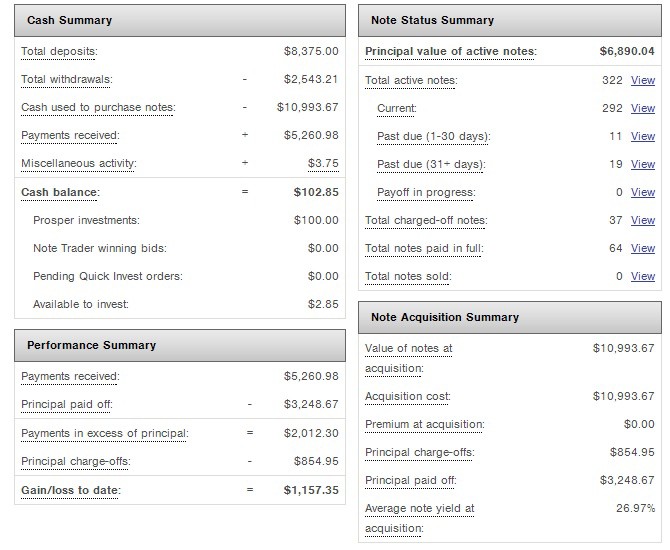

(click to zoom)

Last quarter (2013Q2) I was having trouble getting Prosper’s Automatic Quick Invest to find notes that matched my specific filters. This problem has been fixed by moving over to API investing, as seen in my $2.85 in available cash. My account only invests in D, E, & HR grade notes that meet filters developed on Prosper-Stats.com. I found it interesting this quarter that the “seasoned” ROI they gave me was actually below my real world XIRR calculation. Typically it is the other way around – the on-site calculation is usually too high.

Furthermore, it is interesting to note that the average interest rate of the loans I invest in is 27%, yet I am only earning a 13% return. The reason for this difference is the 37 defaulted (charged-off) notes in the screengrab on the right. This is three times the number of defaults I had on my Lending Club account, evidence of the riskier borrowers I am lending to at Prosper.

Furthermore, it is interesting to note that the average interest rate of the loans I invest in is 27%, yet I am only earning a 13% return. The reason for this difference is the 37 defaulted (charged-off) notes in the screengrab on the right. This is three times the number of defaults I had on my Lending Club account, evidence of the riskier borrowers I am lending to at Prosper.

Overall, I am happy with these returns. Prosper continues to put my money to work helping others get out of credit card debt, providing me with a great return on investment.

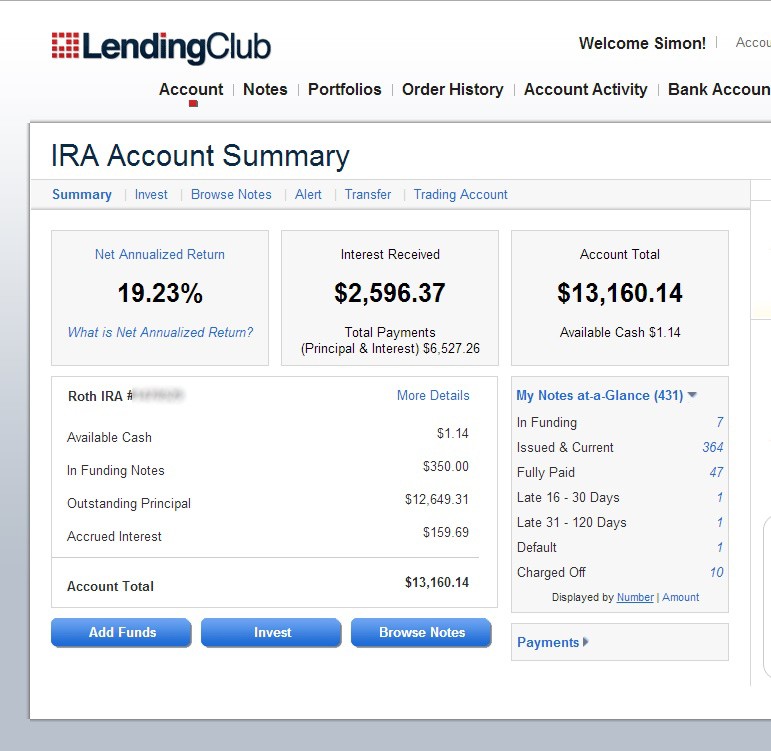

#2 – Lending Club Roth IRA (13.95% return):

(click to zoom)

My Lending Club IRA similarly continues to do well, only investing in targeted E, F, & G grade loans via API. 83% of my notes are with 60-term (5 year) loans, so its makeup is a bit riskier than most lenders. I added $1,500 in new funds this quarter, mostly from closing my old Lending Club taxable account. The average interest rate for my 431 notes is a sexy 21.16%. This means I have lost about 7-8% through my 11 defaults or through selling discounted notes on Foliofn.

My Lending Club IRA similarly continues to do well, only investing in targeted E, F, & G grade loans via API. 83% of my notes are with 60-term (5 year) loans, so its makeup is a bit riskier than most lenders. I added $1,500 in new funds this quarter, mostly from closing my old Lending Club taxable account. The average interest rate for my 431 notes is a sexy 21.16%. This means I have lost about 7-8% through my 11 defaults or through selling discounted notes on Foliofn.

Last quarter my returns had dove almost 3% from the quarter before, from a 16% to a 13% return. In an attempt to stop this momentum, I put a few minutes effort per week into posting any Grace-Period notes at a 10% discount on the Foliofn secondary market (read more on this strategy). I’m happy with the results, though they are less dramatic than I thought they would be. Selling late notes also meant losing a bit of principal to discounts – but I think the overall gain (avoiding defaults) was worth it.

Am I Really Earning a 13.89% Return?

Last quarter (2013Q2) my returns had dove 3% from the previous one (2013Q1). Yet this quarter my overall return actually rose a tiny bit to 13.89%. Is this the new normal? Have I fully experienced the dreaded default curve? I am tempted to say yes, considering my average note is over 10 months old. However, there are a few reasons to doubt this claim. Firstly, I closed my smaller Lending Club taxable account, a portfolio that was earning a 9% return, so that brought the average return up. Secondly, I did inject $1,500 in additional funds this quarter, so there might be a temporary boost there.

I am really curious to see if I can sustain this return into the fourth quarter.

Lending Club Pulls into the Lead!

Regular readers have heard me talk about how Prosper has typically given me higher returns than Lending Club, but this quarter the tables turned, albeit very slightly. Prosper gave me a great return of 13.82% this quarter, but Lending Club beat them by 13 basis points with a 13.95% ROI. Maybe this is because my risky Prosper notes are finally defaulting. Perhaps Lending Club’s sale of late notes on Foliofn is the reason for its rise. Whatever the case may be, it is interesting to note. I am curious if Lending Club will prove itself to offer a more lucrative investment than Prosper as my accounts begin to age.

Simon, you can also do a straight ROI calculation. The reason why you can do that is since the loans are fully amortizing, your principal balance is declining as is the amount going to interest. I talk about that here: http://p2plendingexpert.com/calculating-returns-irr-or-xirr-vs-roi/

Hi Stu. Nice to hear from you. My straight ROI is 17.64% for Lending Club and Prosper is 16.75%. That said, I think XIRR is more accurate because cash drag is such a factor in this whole escapade.

Actually I account for the cash drag, which I agree is important as zero interest earned so it’d Bronx my returns down slightly but since cash earns no interest, that’s why I think it is the most accurate. I like this conversation though of seeing how to calculate returns for yourself

Great information. I found you be searching for Lending Club reviews. From your experience Prosper and Lending Club appears to be the best programs for online note investing?

Hi Cesar. Indeed. Both are great options, and the only ones available within the US.