Update: This project has been completed. Click here.

For today’s post I want to focus on a really interesting question recently asked by reader Huina Smith:

“Could you compare withdrawal of investment between Prosper and Lending Club. I am a new Lending Club investor, but I realize there is no way we can get the money out if we need to use it in an emergency. Lending Club has a trading platform to sell notes at market price, so most likely an investor like me has to take a loss if we want to get the money out, thus wipe out the profit we made in the process. Because of this reason, I decided not to put too much money in this type of account. Does Prosper do better? Any comments, suggestions would be greatly appreciated.”

Huina is experiencing a typical problem that we all face eventually. Often lenders have trouble understanding how to get their investment back if they want to close out their accounts. The short answer is that Lending Club actually has made it quite easy, even in the event of an emergency. If you want to price your notes at cost, gaining no profit (but taking no loss), you can have your money back in a matter of days. If you want to go slower, you can earn a decent profit on your healthy notes. However, her larger question about Lending Club versus Prosper got me thinking about how the withdrawal process is different between the two platforms.

Today, LendingMemo is happy to announce the launch of The Liquidity Project. This will be a five month experiment to examine how easy it is to liquidate a peer to peer lending account. We will do this by selling $1000 worth of notes (40 notes) from each platform on the secondary market.

The process will be as follows:

- Set Up Portfolios – My regular/taxable Lending Club account has a balance of around $1000. I will profile this account today, highlighting average account age, 36/60-term balance, and risk grade. I will then find $1000 in notes from Prosper that match this account (as close as possible).

- Sell Notes – Over a period of five months, we will slowly sell off $1000 notes of both accounts, starting at a 50% premium and slowly reducing every three days until we hit 0%.

- Examine Results – Once both $1000 portfolios are sold, we can analyze the data to see what notes sell the easiest, what premium markups are possible, and how Lending Club and Prosper compare in regard to closing a lender account (liquidity).

Let’s look at each of these steps in more detail.

Step 1 – Set Up Portfolios to Sell

First let’s look at my taxable Lending Club account so we can match it with an appropriate Prosper portfolio.

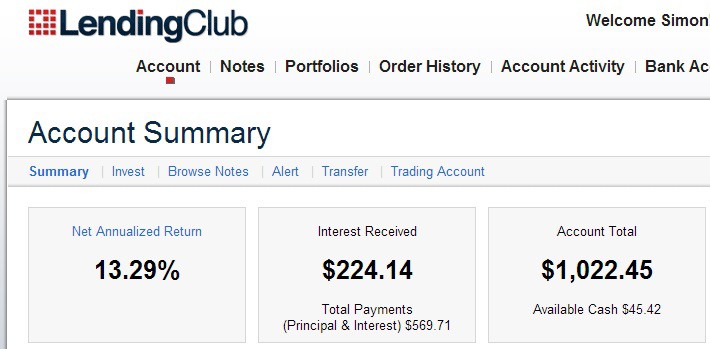

Lending Club Portfolio

(click to zoom)

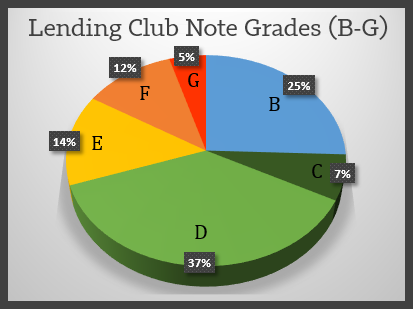

My taxable Lending Club account has a balance today of $1022.45. Of 46 notes, two are in default and four have been paid off. This leaves 40 notes that are available to sell. The grades of the 40 sellable notes are: 10 B-grade notes, 3 Cs, 16 Ds, 5 Es, 4 Fs, and 2 Gs.

18% of the notes have a term of 36-months. 75% were issued 19 months ago, with the remainder issued less than a year ago.

Prosper Portfolio

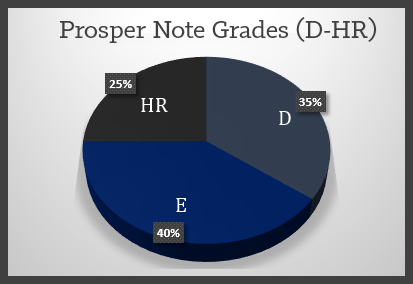

While my Prosper account has over four times the number of notes as this Lending Club account, I have done my best to select 40 notes that match the ones for sale at Lending Club. 14 are D-grade, 16 are E-grade, and 10 are HR-grade loans.

45% have a 36-month term; 55% are 60-month. The majority of these notes are less than a year old; 20% are 12 months or older.

Step 2 – Create Selling Calendar

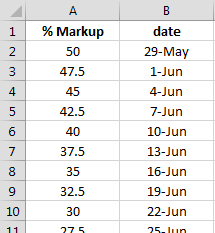

Starting the 29th of May, I listed all these notes for sale at a 50% markup. Every three days I will lower the markup on these notes.

Starting the 29th of May, I listed all these notes for sale at a 50% markup. Every three days I will lower the markup on these notes.

- From a 50% markup to 20%, the premium will drop 2.5% every three days until July 4.

- From a 20% markup to 10%, the premium will drop 1% every three days until August 3.

- From a 10% markup to 6%, the premium will drop by 0.5% every three days until Aug 27.

- Finally, from a 6% markup to zero, the premium will drop by 0.25% every three days until November 7.

With this schedule the project should run for approximately five months and adjust 56 times.

Step 3 – Identify Learning Points

Every note that sells will have its interest rate/loan grade, term, note size, payments to date, and FICO recorded. At the end of five months, we should be able to answer the following questions:

- What is the best premium a lender can get on both Lending Club and Prosper’s secondary market?

- What notes sell the quickest/slowest? (this may inform how we first set up our accounts)

- Getting back to Huina’s question: how does Lending Club’s secondary market compare to Prosper’s if we would desire to close an account?

Let’s Do This!

I can identify a few weaknesses in this study. First of all, the accounts are differently aged. The Lending Club portfolio is almost two years old, while the Prosper portfolio is only a year old, so there will be some differences there. Secondly, most notes will probably sell around 6-7% markup, so I may go months without an actual sale. This may mean the start of the project is a boring one indeed :)

I have to admit that this project helps ease a distraction I’ve been having since LendingMemo began six months ago. My taxable Lending Club account has been easy for me to forget about. It only earns maybe $10-$20 per month, and has some B-grade notes I purchased before I knew much about peer to peer lending. In this way, I am not very attached to this account, and think the Liquidity Project is a chance to make my Lending Club experience simpler, giving me a reason to close the taxable account so I can completely focus on my Roth IRA (see my Lending Club returns).

I am excited to see what happens! I am eager to examine the profit a lender can make from his or her healthy notes that are being repaid on time, as this info might help develop additional p2p lending strategies for the future.

[image credit: Kyle May “DIY Fake Ice Cubes” CC-BY 2.0]

Interesting experiment. Looking forward to the results.

Thanks Dave. I look forward to sharing them.

So what have been the results?

At the moment about 15% of the loans have sold. When all of them sell, I’ll write a post on the topic. Thanks for your interest Jon.

I’d like to see the results. Will they be available soon?

Last three notes selling this month.

Are all sold? Looking forward to see the report.

Yeah, where are we at with this study? Great planning. I’m very curious to see the results.