Continued from part 1

Returning from living in Kenya introduced me to this thing people often refer to as the real world. Adulthood, the future, my car’s low-fuel light: these were suddenly hard for me to fathom. After all, I had been chillaxing in sandals and shorts for the bulk of my mid-twenties. This is not to say that 70 degrees and sunny does not have its stressors. For instance, while walking around Nairobi I would suddenly be overcome with the desire that, yes, did I want to eat a mango. And after purchasing, slicing, and eating said mango, my fingers were often pruned from the juice like I had just taken a bath. Inconvenient.

Returning to the United States would be an adjustment, but this was a choice I was willing to make. I missed my family, my sister was getting married, and my graduate studies were finished. Most pressing, there is only a certain amount of Nescafe instant coffee a man can drink before madness sets in and he finds himself shirtless in the desert, chewing khat leaves and offering his opinions to the local djinn.

Returning to the United States would be an adjustment, but this was a choice I was willing to make. I missed my family, my sister was getting married, and my graduate studies were finished. Most pressing, there is only a certain amount of Nescafe instant coffee a man can drink before madness sets in and he finds himself shirtless in the desert, chewing khat leaves and offering his opinions to the local djinn.

I eventually landed in Seattle, and through a colossal exercise in misjudgment, somebody offered me a job. With this job came an actual income, an income that introduced all sorts of new questions:

- Should I get a one bedroom apartment or a studio?

- When was the last time I went to the dentist?

- Where can I find a pretty American girl who will let me buy her a drink?

Perhaps more pertinent to this website, I was suddenly thrust into saving for retirement. And with this new responsibility came the question: how can someone save for retirement in a way that is kind towards those in need?

Searching for a More Moral Mutual Fund

It is interesting that I still had this value, or any values at all. You see, world traveling involves a certain degree of deconstruction. For instance, in Kenya I watched as people used bicycles to sharpen knives. How? Well, they simply propped a bike on blocks, attached the chain to a grinding stone between the handle bars, and peddled it while pressing the blade’s edge against the spinning stone. It was simple in its genius. And suddenly you never could look at a bike the same way again.

It is interesting that I still had this value, or any values at all. You see, world traveling involves a certain degree of deconstruction. For instance, in Kenya I watched as people used bicycles to sharpen knives. How? Well, they simply propped a bike on blocks, attached the chain to a grinding stone between the handle bars, and peddled it while pressing the blade’s edge against the spinning stone. It was simple in its genius. And suddenly you never could look at a bike the same way again.

All sorts of societal beliefs and practices were realized to be less important than I had been taught (in example, Big Gulps). Yet one thing that had become more true over the past three years was the reality of hardship and poverty throughout the world, along with my ability to do something about it. “There are no great deeds,” Mother Teresa used to say as she bathed children in the slums of Calcutta. “But there are small deeds with great love.”

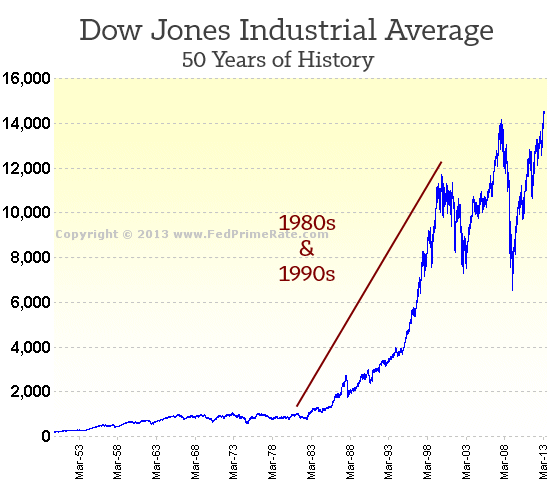

As I researched different ways to save for retirement, I realized a whole host of people had been asking this same question about socially responsible investing, and they were doing so while looking at the main way the country was saving for retirement: mutual funds. Why were mutual funds the most trusted way to save for retirement? Because for much of the last thirty years American mutual funds had soared in value. People who had invested portions of their retirement in these funds were richly rewarded, often with little to no effort of their own. They had simply handed portions of their income or savings over to a big investment firm and the firm had subsequently delivered positive results. This passive approach to investing continues to be the most popular way to save for retirement in our nation today.

I researched different socially responsible mutual funds, picked one that had won numerous awards the previous year, and opened up my very first IRA. I could not believe how responsible I felt. Looking back, it seems a very dull decision, but at the time I felt a joy similar to my first shave. I remember looking down at the glossy prospectus that came in the mail and marveling at its rowed numbers and colored graphs. Life seemed full and real and going somewhere.

Six months later I received another prospectus about my mutual fund. Reading this one more soberly, I was frustrated to notice a small box that said, “Ten Largest Holdings”. Within this box were ten of the largest corporations on earth, companies like Coca-Cola, companies that were about as synonymous with social responsibility as Kate Upton is with going to church. Nothing against Coke (or Kate Upton) per se, but there had to be a better way to help people than through caloric intake and dental cavities.

Seduced by Peer to Peer Lending

This realization quietly hounded me for weeks, like a pebble in my shoe. Here I was, a decent man with a decent income and a desire to do something good, and I had been duped into becoming part of the system, fooled by a marketing gimmick. I guess I should have done my homework better. “Is there any other option?” I kept asking myself. Holding onto that mutual fund felt like dating a girl while your friends keep confiding that “you can do better”. There was this image in my head of something extraordinary, something worth waiting for, but I had no idea where I could find it.

And then, from a distance, she came into view. I was reading one of the earthier personal finance blogs when I noticed an article about something called peer to peer lending. I followed the headline and was intrigued by what I read.

The article began by saying how the majority of the borrowers were people who were stuck in credit card debt. Through your invested cash, they could combine all their confusing credit card bills into one easy payment while at the same time lowering their interest rate. Since the banking sector was mostly sidestepped and there were fewer middlemen to pay, peer to peer lending was incredibly efficient, and borrowers could get far lower interest rates than they could with their credit cards. The article closed by talking about the lucrative returns lenders could receive on their investment.

The article began by saying how the majority of the borrowers were people who were stuck in credit card debt. Through your invested cash, they could combine all their confusing credit card bills into one easy payment while at the same time lowering their interest rate. Since the banking sector was mostly sidestepped and there were fewer middlemen to pay, peer to peer lending was incredibly efficient, and borrowers could get far lower interest rates than they could with their credit cards. The article closed by talking about the lucrative returns lenders could receive on their investment.

Things just flowed from there. Like a train emerging from tunnel, I opened up my first account that evening, transferring my Roth IRA from that “socially responsible” mutual fund to Lending Club a few months later.

Read the epic conclusion in part 3.

[image credit: Rabiem ‘Sunset Romance‘/Andrew Hyde ‘Something is odd’

Kai Hendry ‘Man sharpening a knife‘/SqueakyMarmot ‘Whoops…‘ CC-BY 2.0]

Leave a question or comment