In January of 2013, Aaron and Steve Vermut and Ron Suber faced a impressive task. They had just become managers of a platform called Prosper Marketplace, a company that was a pioneer in the American peer to peer lending space. However, the company was experiencing a number of critical issues that were dragging it downward, so the new team began outlining how to turn the company around.

One of the largest issues in early 2013 was the instability of their current investor base. Without stable funding of their loans, prime-rated borrowers simply would not get their loans funded. More than anything, Prosper needed a reliable institutional investor base. Without it, all of their remaining work would be in vain. To this end, the company turned to Ron Suber.

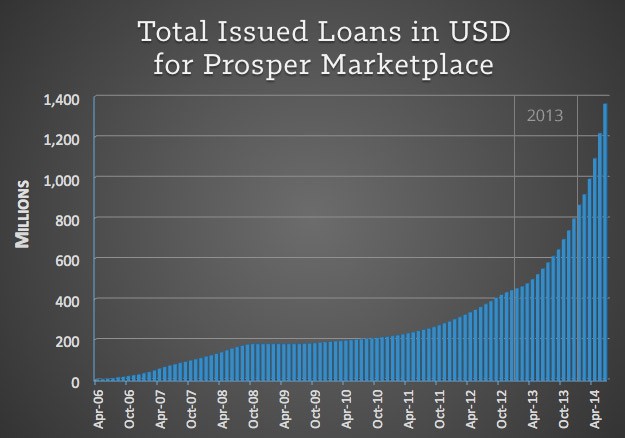

Suber, a gifted communicator and industrious traveler, packed his bags and got on the road, traveling the nation to listen to what these prospective investors were looking for. At that time, not a single institution was lending through his company. But just twelve months later, Prosper had some of the largest names in American finance as investors on its platform, institutions that ushered fresh stability upon the company, enabling both borrowers to get their loans funded as well as small-dollar investors to have a stable platform in which to place their excess cash.

Suber, a gifted communicator and industrious traveler, packed his bags and got on the road, traveling the nation to listen to what these prospective investors were looking for. At that time, not a single institution was lending through his company. But just twelve months later, Prosper had some of the largest names in American finance as investors on its platform, institutions that ushered fresh stability upon the company, enabling both borrowers to get their loans funded as well as small-dollar investors to have a stable platform in which to place their excess cash.

Recently, I was able to sit down with Ron Suber and talk about how he and his team were able to pull this feat off.

Interview with Prosper President Ron Suber

When you arrived, the company was in a very different place. What were some of the more immediate areas you needed to improve on?

Ron Suber: Clearly, there were many good things about Prosper when we arrived in January of 2013. But one of the main things that needed to change, and change in a hurry, was the brand. The identity, positioning, and design of the company needed a lot of work. Another key thing that had to change was how we acquired borrowers – moving away from this heavy reliance on direct mail and into a more digital marketing and partnership strategy, leaning more into our existing clients and affiliate program.

Aaron Vermut has described in an interview how he arrived to find Prosper sorely needing a stable investor base. Toward this end, what did your original job description look like?

My job description in the very beginning was not to sit at Prosper, but to hit the road and meet with both retail and institutional investors. This largely meant sitting down and listening to what they wanted from us. Many were using other platforms, both personal and business financing, so they could teach us what we needed to do in regard to improving things like the API, data, a bankruptcy remote structure, or setting up a whole loan program, since there was no way to buy a whole loan at Prosper when we arrived.

Notably, there also was this class action lawsuit against Prosper Marketplace by some people who felt they had been wronged. One of our early priorities was to meet with those people, introduce ourselves, and work something out that was good for all parties.

Imagine yourself having just begun your job in early 2013, ready to hit the road. How did you create your first list of prospective institutions to reach out to? Did you just go through your address book?

From my own family office, I was a fairly significant investor at Lending Club and Prosper starting in 2010. I had actually met with the management teams of both organizations, as well as with institutions that were already investing in both of the platforms. Also, my experience on Wall Street for 14 years with Bear Stearns, and working alongside 800 different hedge funds at Merlin with Steve and Aaron, really gave us a head start in terms of knowing the hedge funds, asset managers and family offices, as well as having experience working with them. We traveled around the country to meet with people, from Boston to New Jersey, to New York, to Florida, to the mid-West and all around California.

We had to articulate one key thing, that we had skin in the game too.

Some of these institutions said to us, “We want lower fees” or “We want Prosper to own some of the loans too.” But these were things we were not willing to do. We felt that the fees were fair, and we thought that the platform should not actually own a portion of the loans. So we had to articulate one key thing, that we had skin in the game too, that the management team was shoulder-to-shoulder fully invested in Prosper’s success as well. That was crucial to helping people see our commitment to Prosper’s success, and that it would grow with quality to become a successful and profitable company, like it is today.

When you think about those days, do you remember typing up that initial spreadsheet and getting on the plane to have your first meeting?

I remember flying from Chicago to New York, getting off the plane, and meeting with an incredibly smart $25 billion asset manager who gave me a real education. Candidly, some of these early groups did not invest on the platform for a year. I would stay in touch with them and keep them up to date. Actually, they gave us lots of strategic advice on how to improve the platform. And many of those original people who I met with in the spring and summer of 2013 are now clients of Prosper. It’s been a great relationship from the beginning, improving this company to a point where many became comfortable enough to get on board and invest in the loans.

How did that first meeting end? Did they partner up or take a pass?

The first meeting was an investor with another peer to peer platform, and they were very clear that they would not work with us until we changed certain things. It was actually very educational. I came back to Prosper and met with Aaron and Steve and our team here, and I remember standing up at a white board and drawing a picture. I drew the way Prosper was on the left side, and I drew the picture that these institutions in New York articulated they wanted on the right. And I said that in order for us to get many of these groups on board, we have to get Prosper to look more like the picture on the right, which involved all sorts of different legal, technology, and accounting improvements. So we began to hire people and work with the Prosper team to help us build out that picture.

And today, many of these groups that originally took a pass are now investors at Prosper?

That’s right. Some of them still don’t do business with us, but they want to. We just do not have capacity for all of them at this time. Today, a few of them are very big clients. In fact, one of our earliest clients has recently passed more than $100 million in loans, and is very happy to have been an early partner with us.

Peter Renton has said, “Probably more than anybody in our industry, Suber travels the country spreading the word and evangelizing peer to peer lending.” Just for kicks, how many frequent flier miles did you bank that year?

I am, unfortunately, an Executive Platinum flier with American Airlines.

(laughter)

The flight attendants know exactly what seat I’m sitting in. It’s actually not that glamorous; I flew over 100,000 miles last year. But this was something that had to be done. I had to meet those current and potential clients in person. There was no way around it.

How many prospective investors did you meet? How many signed up?

I met with more than 100 potential investors in those first twelve months. Today, roughly 20 of those groups are investors on the platform in a sizable way. It was really just about building trust. I had a few of these groups to my home, because they wanted to know more about us. Some of them came to the office to observe. Some of them even sent their accounting firms in to audit us, and really came to understand the inside of Prosper, not just our credit model, but how the money flows and technology works. They saw our relationships with the bank where the assets sit, and met with our legal team. The whole process has actually been a lot of fun and a great education.

There must be something really validating about having a major institution look at your company inside and out and choose to partner with you.

One of those early prospective investors from April of 2013 just put their first investment on the platform last month. Today, we laugh about our original meeting in a hotel conference room, about where the industry was back then, and where the platforms were. So much has changed.

It sounds like the majority of these groups took a pass for one reason or another. What were some of the common reasons they gave for not signing up with you?

Some of these early groups were skeptical towards our credit model and underwriting, either through a lack of understanding or trust. Today this has changed because the credit model is performing even better than we had advertised. The actual defaults have been less than what we expected.

Now that we are profitable, I think that is the final answer to people’s previous reluctance.

Another key issue was if we had enough capital to survive. We answered that question with the original money we invested with Sequoia, and then the September financing with Sequoia and BlackRock, and then the financing two months ago with $70 million from three large venture capital and institutional investors. And now that we are profitable, I think that is the final answer to people’s previous reluctance.

How has your job description evolved since you successfully created this investor base?

We think that these online market places for credit are a blend of both retail and institutional investors. We are actually very focused now on adding additional retail investors, even more so than before, so we are working today with some great investment advisors and wealth managers who are helping retail investors gain access to Prosper.

Has your overall work week stayed the same? Will you get on a plane next month to meet with a RIA somewhere, have a cup of coffee and hear their concerns, offering them to get on board?

It’s very similar. It is focused on education, awareness, and understanding of the retail investor, as we first did for the institutions, and then we did for the borrowers. We are working to make it easy for the big wirehouses and other places where retail people are to invest in Prosper loans.

Thinking back to those early days before Prosper’s turnaround was secure, what was one of your earliest celebratory benchmarks?

It was a big day when the first public institution that traded on the New York Stock Exchange became an investor-client at Prosper. Not only would an individual or a private investment partnership want to invest, but a public institution would as well. And then a second one came; the world’s largest asset manager started buying loans from us. And then insurance companies began investing. Then banks.

There was a clear “Aha!” moment at that time that made us realize that we had something special here. If these firms, with all the audits they had done on us from top to bottom, had decided to be clients, we knew this was going to be successful.

Do you remember going out for a celebratory dinner or drink with Aaron and Steve around this time? What did it look like when you got back to San Francisco?

Yes. The three of us met up, sat down together, and came to grips with the magnitude of what was happening. I remember saying to them, “This is even bigger than we originally pictured. This is a mega trend.”

Looking toward Prosper’s future, what excites you about where this company is going?

What really excites me is the opportunity to work with my current teammates and the new people joining Prosper. We have very talented people out of college, people in the middle of their careers and people leaving big successful technology and finance firms with PhDs. There are people coming from all over the world to work with us. I’m excited about the brand new office that we are building for the Prosper team. We hope to move there in December. This is more than work for me; it’s my passion.

A great article about a great American success story. We were one of the very early firms that believed in Suber and the Vermuts from day 1, and we applaud them and the rest of the Prosper team for doing an outstanding job navigating and managing the many layers of difficulty in running a peer to peer lending platform.

Hear hear. Thanks for stopping by Don.

Great interview, Simon.

The greatest pleasure in being involved in this industry is the quality of the people, especially within the marketplaces, and Ron is a perfect example. I’m slightly disappointed he’s only silver platinum, though…

The remarkable turnaround of Prosper from Dec 2012 to today has been simply amazing to watch. You captured it well, Simon and Ron. Keep up the great work, both of you!

True Blue leadership.

Agreed. Thanks Bo.

Great article, really shows how success is created. Ron and the entire Management Team at Prosper have done a remarkable job. Prosper is soaring and it can only get higher !

This is a great turnaround story. Ron’s leadership has been very impressive. I have met Ron couple of times in person and I think he is a real visionary with some tremendous people connect and leadership skills. Prosper specifically and the P2P industry as a whole is very lucky to have Ron as the key evangelist and brand ambassador.

Great interview.

Good info for P2P community, but also good advice for anyone with their own business or startup. Go out of your way to listen to customer feedback about your product.

Fantastic interview, and inspiring.

The message in here is powerful – learn from your customers through constant dialogue in order to make your products and services better, whether your customer is a 6 year old child or a multi-billion dollar institutional investor.

Because of his fidelity to his customer and potential customer base, Ron and team have certainly positioned themselves to benefit from this megatrend – a trend which may never have been revealed without the persistence of Prosper.

Great comment. Thanks Scott.