Each quarter I will post the current state of my peer to peer lending returns at Lending Club and Prosper so that readers can follow my process, ask questions, and make critiques. My approach is maximum ROI through highly-targeted low-grade loans.

I opened my first account in September of 2011, and have opened two more since then. I have a total of three accounts, two with Lending Club and one with Prosper. As you can see in the following table, I finished 2012 with a wonderful ROI in both Lending Club and Prosper.

|

Account |

# of Notes |

Average Age (months) |

On-site ROI (boo!) |

XIRR ROI |

NickelSteamroller/ Prosper-Stats ROI |

| 1. Lending Club |

46 |

12 |

16.27% |

12.34% |

13.6% |

| 2. Lending Club IRA |

353 |

7 |

21.00% |

19.00% |

17.5% |

| 3. Prosper |

339 |

5 |

20.04% |

19.8% |

16.9% |

I am not sharing my account balances, though this will probably change as I become more warm to the idea. For now, I feel note number and ROI is enough. My preferred way to determine ROI is through the NickelSteamroller.com Portfolio Analyzer for my LendingClub accounts, and through the Prosper-Stats.com tool for my Prosper account. While some might prefer calculating return using the Excel XIRR function, I prefer it this way because these tools take into account late loans. That said, I included the other two for comparison’s sake.

Account Breakdown

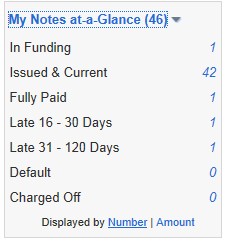

Lending Club Account: This was my first peer to peer lending account, and has been the one that has suffered from the most mistakes. The bulk of my lending here was done without using LendStats, and you can see the difference. I actually own a few B-grade here, something that I quickly abandoned in favor of low-grade notes for all the rest of my accounts. This account now funds only D grade loans.

This was my first peer to peer lending account, and has been the one that has suffered from the most mistakes. The bulk of my lending here was done without using LendStats, and you can see the difference. I actually own a few B-grade here, something that I quickly abandoned in favor of low-grade notes for all the rest of my accounts. This account now funds only D grade loans.

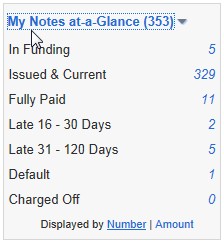

Lending Club Roth IRA:  This is probably the one of which I’m most proud. I opened this IRA by transferring my retirement account away from a socially-responsible mutual fund (which, when I examined its holdings, was not very socially-responsible). I have put a lot of effort into maintaining good filters, and am happy with the resulting few late loans and defaults. I still cannot believe that I’ll withdraw these funds tax-free (ahem… in thirty years). This account only funds E, F, and G grade loans.

This is probably the one of which I’m most proud. I opened this IRA by transferring my retirement account away from a socially-responsible mutual fund (which, when I examined its holdings, was not very socially-responsible). I have put a lot of effort into maintaining good filters, and am happy with the resulting few late loans and defaults. I still cannot believe that I’ll withdraw these funds tax-free (ahem… in thirty years). This account only funds E, F, and G grade loans.

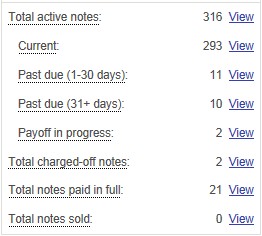

Prosper Account:  I have learned the most about developing good filters through lending on Prosper, mostly because they have such possibility for a great return in E and HR loans but have also been most difficult to avoid late loans. Things have not gone totally as I had planned, to a small degree from LendStats ending its Prosper tool and me not switching to Prosper-Stats.com quickly enough. I also feel my filters on Lending Club are stronger because that platform has a lot more loan history to examine. That said, I am still happy with my Prosper account. I recently reworked my filters for 2013 and am interested to see if I can pull this ROI up to 17%. This account only funds D, E, and HR grade loans.

I have learned the most about developing good filters through lending on Prosper, mostly because they have such possibility for a great return in E and HR loans but have also been most difficult to avoid late loans. Things have not gone totally as I had planned, to a small degree from LendStats ending its Prosper tool and me not switching to Prosper-Stats.com quickly enough. I also feel my filters on Lending Club are stronger because that platform has a lot more loan history to examine. That said, I am still happy with my Prosper account. I recently reworked my filters for 2013 and am interested to see if I can pull this ROI up to 17%. This account only funds D, E, and HR grade loans.

Inflated ROI

While my high ROIs in these accounts are definitely worth celebrating, its important to remember that my accounts are just beginning to get established. Peer to peer loans are amortized, meaning they give less ROI as more time goes by. Even with me consistently reinvesting my returns, I expect amortization and defaults to bring my ROI down in the coming years. I feel my real world ROI at Lending Club will settle down to 15%, with about the same for Prosper.

Overall, I am thrilled with my experience in peer to peer lending. It is awesome to get over a 15% return in any avenue at all, let alone one that is socially responsible.

Questions or comments? If you enjoyed this please Like or Tweet it below.

Kudos on your returns!

I’m curious on your plan for when the market dives again. I have been a lender on Prosper for 5 years and LC for 2 years. Your high risk, high return portfolio would have been decimated in 2008 and 2009 like mine was if you strictly stayed with the mix that you list above.

Since you just started lending in 2011….the market as a whole has been on an upswing. High rish borrowors are able to pay their bills but you know that will change once, (and it will change) the market turns south. Do you have a game plan for this certainty?

Hi Jack. Thanks for your question. It’s a good one and I’ll be addressing it better in a future post. However, here’s my sense of things (and only my opinion): the market is far less involved with borrower repayments than we might assume. I believe a major downturn in the economy (like national unemployment ballooning to 15%) would affect my account negatively, but not substantially. In that scenario I believe I would only have a 5% increase in defaults.

2008 was the biggest economic downturn since the great depression, yet Lending Club still produced a positive return for its lenders (something the S&P can’t say). Plus, back then their underwriting was still being worked out, so I would assume their defaults would be even lower today.

Hope that helps, Simon