Each quarter I post the current state of my peer to peer lending accounts. I am a lender who enjoys maximizing my return through highly-targeted low-grade loans. I opened my first account in September 2011, and have opened two more since then.

As you can see in the following table, I continue to celebrate thriving positive returns on both Lending Club and Prosper.

Calculating ROI is Tough

Calculating your peer to peer lending ROI (return on investment) is tricky business. If you want the easy route, both Lending Club and Prosper offer you their somewhat inflated number. If you calculate the rate yourself using the Excel XIRR function you get closer, but this still does not take into account any notes that have gone late (and are, as such, no longer worth their full value). Michael’s Portfolio Analyzer on NickelSteamroller includes a reduction from these late notes, but does not do well with loans bought or sold on the secondary market. I have included all three ROIs here for comparison’s sake (see my analysis of calculating XIRR return).

Accounts Breakdown

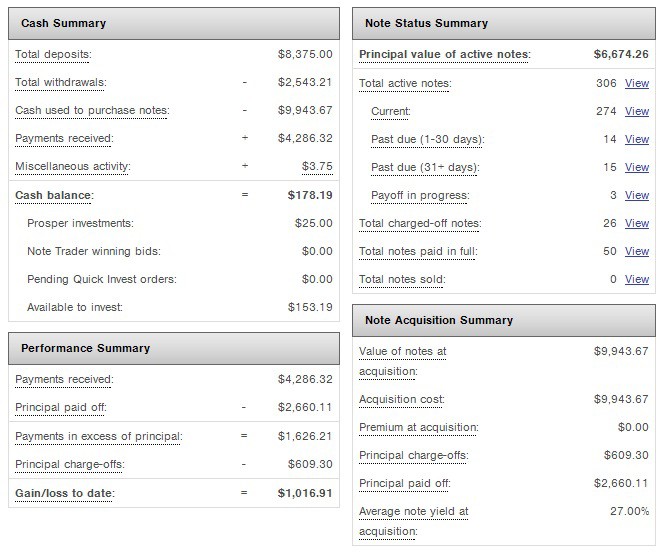

#1 – Prosper Taxable Account (14.76% return):

(click to zoom)

This was a tough quarter for my Prosper account. As you can see in the screenshot above, I continue to amass uninvested cash. There’s a good thread on this problem at the LendAcademy forum. In short, there is a lack of quality low-grade loans to invest in through Automated Quick Invest (AQI). As seen in the NSR Prosper Loan Grades chart, this is partially because Prosper has not been issuing many E & HR-grade loans, the two grades I am trying to invest in with this account. To boot, more and more lenders are investing through the Prosper API, able to snap up loans before my AQI tool can find some to invest in. This idle cash combined with a number of new defaults have caused my ROI to drop 3% to 14%. You can see this in more detail in the screengrab below:

(click to zoom)

Looking to combat this trend, I hope to switch over to API investing myself in the coming months. Secondly, its important to restate that loan defaults peak at month 10. My Prosper account is also my youngest, with the average note age at nine months. I assume this ROI will drop a bit more in the coming quarter because of additional defaults (15 notes are 31+ days late), I believe things should even out at a 12% ROI by the end of the year.

One interesting thing to note is that this quarter’s XIRR ROI exactly matches Prosper’s on-site ROI calculation. Crazy sauce.

#2 – Lending Club Roth IRA (14.09% return):

(click to zoom)

Like last month, I continue to be proud of this account. Six loans defaulted in the past quarter, dropping my ROI to 14%. But now it looks as if the rough waters are behind me – out of 342 active notes, almost none are late. I (mostly) invest in E, F, and G-grade loans in this account. To help avoid defaults, I have begun using the Foliofn secondary market more often, selling Grace Period and Late 16-30 Days notes before they default. Also, one benefit of a Lending Club IRA is being able to avoid Foliofn tax paperwork, an often confusing part of being more active on the secondary market.

#3 – Lending Club Taxable Account (9.13% return):

(click to zoom)

This account should be closed by the end of the year. I began The Liquidity Project recently, an experiment to explore the maximum I can earn while selling off notes and closing an account. This past quarter the ROI dropped another percent, partially because I have begun withdrawing available cash. Also, since this taxable Lending Club account suffered from a few beginner mistakes and even has some B-grade loans (it was my first account), its overall ROI is lower than my Lending Club IRA.

Onward & Upward: Shooting for a 12% ROI!

For those keeping track, my overall ROI dropped a full 3% in the past three months (see last quarter’s update). This is important to note. All lenders experience a default curve. Early months are interest rich and without many defaults, while later months earn less interest and contain more defaults. This curve has begun to settle over my account as well. Thankfully, the majority of the defaults seem to over at my Lending Club account. With the closing of my Lending Club taxable, a switch over to Prosper’s API, and active selling of late loans on the Lending Club secondary market, I believe a steady overall 12% ROI (XIRR) is possible.

The Beauty of Hands-On Investing

I want to close this update with a short reflection on hands-on investing. It is amazing to me that 99% of Americans invest and save for retirement in ways that are outside their control. It is amazing, a privilege even, to have found an avenue of saving for retirement that is so hands-on. It is phenomenal how I am able to examine the state of my peer to peer investments and intentionally retarget its approach into the coming quarter.

The average American will check his retirement account this week. He or she will open a browser window and ponder the haphazard line graph of whatever mutual fund they are invested in. They will experience an emotion like hope or frustration. And then they will all do the same thing: close the browser window and return to their work.

I am so thankful to have found an alternative route to financial prosperity that gives me such agency over my own future.

Nice job Simon. I am finding on both platforms that I am having a tough time getting C grade and lower loans funded and my model is based on far fewer notes purchased. Are you finding this on both or only on Prosper?

Thanks Stu! I seem to find enough on Lending Club, but low-grade availability is limited there as well, just not as bad as on Prosper.

I am having this issue primarily with LC. Since I buy far fewer notes its starting to become a problem. I am trying to fund 10 and am now on my purchase of my 23rd loan.

That spreadsheet looks really useful. Is any of that automated or do you update manually? Do you have the formula for the excel XIRR ROI ? I have two lending club accounts and I am also curious how to maximize return and believe reporting is really helpful for that.

Also if you could explain why the XIRR field is a better indication of real return I’d appreciate it!

Hi Sean. The table was typed out in MS Word. Actually, I just finished a post on this: /xirr/

Sean, on my blog I do a simple interest calculation of Net Interest Received/Amount invested but I have not had any loans term out (complete and retire) or sold any with payments remaining and its those factors that make IRR more accurate over time.

wow, this is a great result. My rate dropped due to recently added funds, but I am at 12.80% … close enough :)

Nice work Martin!