Each quarter I put my money where my mouth is and post the current state of my personal peer to peer lending investment. I am a investor who enjoys maximizing my return through targetting p2p loans that have the highest interest rates I can find (as well as some minor filtering). While this approach likely boosts my overall return, it also puts me at higher risk for suffering from a rise of any national factors that negatively affect borrowers, such as the national unemployment rate. Most investors, especially those starting out, would probably be better off staying within the more popular A/B/C/D grades.

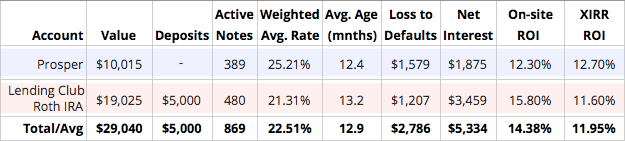

Caveat aside, you can see in the following table how I continue to celebrate positive returns on both Lending Club and Prosper.

Many Ways to Calculate Returns

Calculating your peer to peer lending return can be difficult. If you want the easy route, both Lending Club and Prosper offer you their measurement, but it can sometimes be inaccurate, especially if you do any trading on their secondary platforms. Calculating your ROI independent of the platforms via XIRR is probably the best solution. Read more about calculating XIRR here.

Calculating your peer to peer lending return can be difficult. If you want the easy route, both Lending Club and Prosper offer you their measurement, but it can sometimes be inaccurate, especially if you do any trading on their secondary platforms. Calculating your ROI independent of the platforms via XIRR is probably the best solution. Read more about calculating XIRR here.

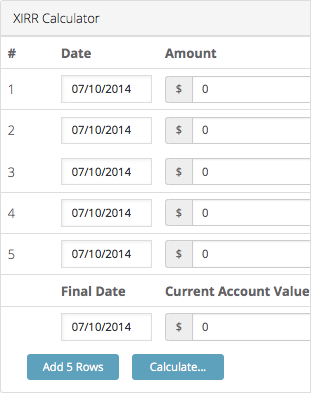

Introducing LendingMemo’s XIRR calculator

To help investors more accurately measure their returns, I am pleased to share our new XIRR calculator. See picture on the right (hat tip to Pat for his generous code).

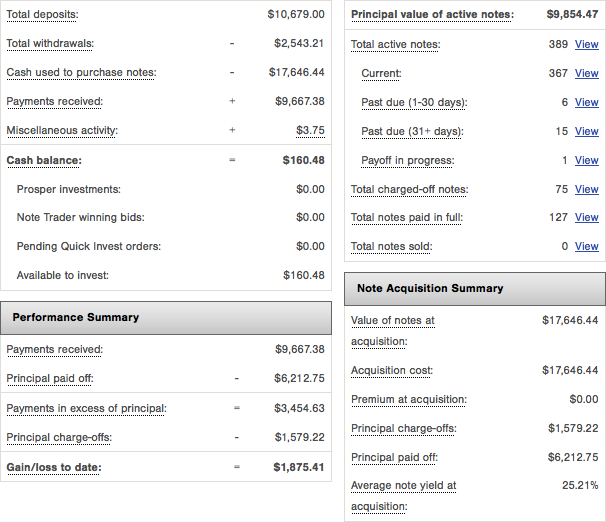

Accounts Breakdown

In comparison to last quarter’s returns, my Prosper account return rose slightly, while my Lending Club return dropped 1.5%.

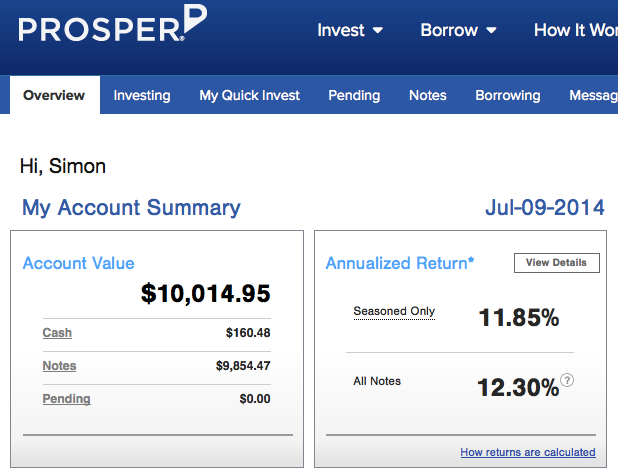

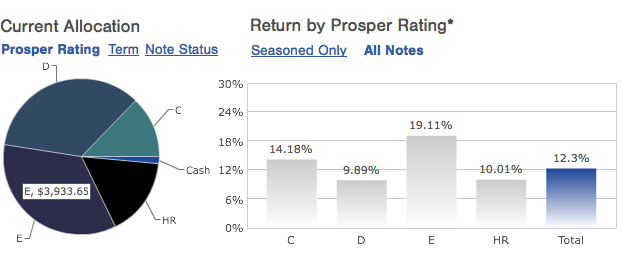

Prosper Taxable Account: 12.70% ROI

This past quarter was just another typical three months for my Prosper investments. I barely checked it. I earned 12%. Life is good.

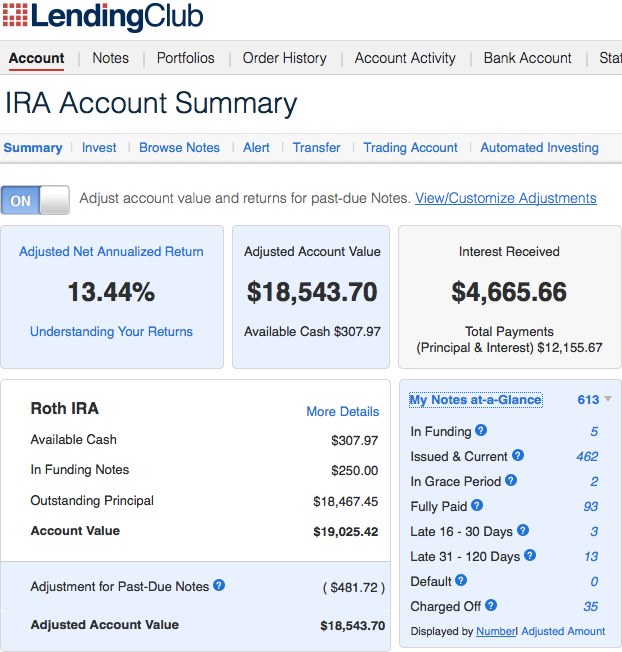

Lending Club Roth IRA: 11.60% ROI

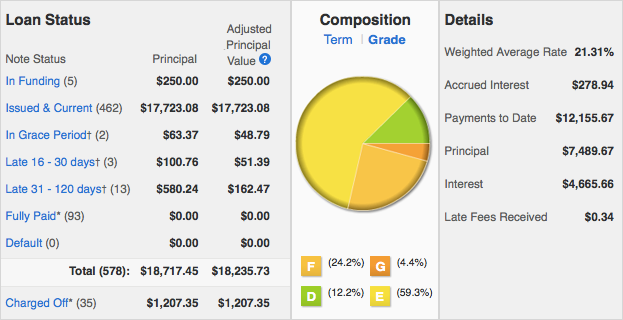

I was, at first, a bit curious why my Lending Club account return dropped 1.5%. After some digging, I discovered two factors at play. The primary cause was a rise in defaults within the account. This past quarter, I had $540 in additional principal lost to borrowers not paying their loans back, raising the total loss to $1207 (vis-à-vis the previous total of $667).

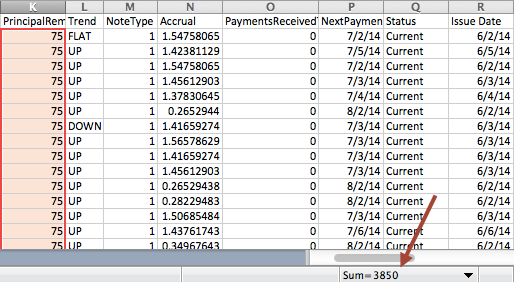

Secondly, I had just made the $5,000 annual contribution to this IRA in early May. It took three weeks to get this money fully invested (via somewhat strict filters) @ $75/note, and despite some time having passed, almost $4,000 of these loans have yet to make their first payment (see Excel below; the sum of all notes without a payment is indicated by the arrow):

Making a relatively large deposit like $5,000 typically gives a short-term boost to the rate of return (read: the Return Curve). However, it takes a month for most borrowers to begin making their payments, so for the past 6 weeks I have had nearly $5,000 bringing down the overall ROI. The boost of this quarter’s deposit should likely be felt in the coming quarter.

I am keen to see if this year’s Q3 will experience the same degree of lost principal as this past one, considering the default rate theoretically stabilizes after 18 months (and this account is, on average, 13 months old). I’m particularly interested if the typical 18-month return curve is delayed for loans with longer terms, since 88% of the notes within this account are 5-year loans, and my largest jump in defaults actually occurred after the first 10 months.

Some Final Thoughts

This is the seventh post of my personal returns that I have written on LendingMemo, and while my understanding of peer to peer lending has certainly matured in the past two years, I can honestly say my enthusiasm has stayed consistent.

I have embraced passive investing

When I began p2p lending, I enjoyed manually logging into the platforms each day, carefully selling off late notes while meticulously maintaining my filters. I did this because I loved it. It was an empowering experience to self-manage such a novel and tech-based investment. But these days my tack has changed. I am far less gung-ho than I used to be about achieving soaring 12%+ returns, following the lead of investors like Peter Renton into moving from active to passive investing.

This has happened for three reasons. First, I have less time than I used to. Second, selling late notes has largely ended for me (disallowed on both Prosper & Lending Club IRAs). Finally, filtering seems less lucrative than before. Alongside PeerCube’s recent post critiquing fast API investing, I have not seen any hard data demoting the use of filters, but it does generally feel this way. I am studying at UW in order to someday develop my own algorithmic model (similar to Bryce’s approach at P2P-Picks), but while simple filters (IE: Inq=0) still seem worthwhile, they just don’t seem to have to the same punch as they used to.

Peer to peer lending is remarkable

Despite having walked back from the more active angles I just mentioned, I have definitely walked forward into a more holistic appreciation of this investment and all it signifies about how technology is lowering barriers of entry. The short story is that consumer credit, the asset class of simply issuing lines of credit to individuals, is a staggeringly lucrative and consistent investment that is finally available to everyday Americans. Not only does peer to peer lending continue to heartily deserve my own investing dollars (seen above), but it also continues to merit the hours it takes for a site like LendingMemo to play a small part in welcoming its arrival onto the national stage.

Questions/comments?

Awesome post, Simon. Which platform has produced the highest returns to date. I’m assuming you use different filters/criteria for each platform.

Hi Yonathan. Prosper has higher returns to date if you take the platforms from post-SEC approval till now. This is largely because they offer a wider selection of borrowers to lend to. So, on Lending Club, they only issue loans to people at a 25% interest rate and below. On Prosper their HR loans go all the way up to 30%, with these borrowers being even more risky than Lending Club.

That said, the experience is quite comparable today. The situation is slowly changing as Prosper lowers their average interest rate while Lending Club raises theirs. See this: http://www.nickelsteamroller.com/#!/charts?vendor=lendingclub&chart=monthly_irate versus this: http://www.nickelsteamroller.com/#!/charts?vendor=prosper&chart=monthly_irate

I recommend a prospective lender consider getting an account with both.

Passive vs Active – I think active investing in P2P market is similar to stock market day-trading vs long-term investing. It can be very fun to analyze the numbers (I’m a numbers nerd) and make an investment decision, but I am not sure it improves returns.

Make a good investment initially and then forget about it.

I live in a state where p2p isn’t allowed. Both Prosper and Lending Club refer to Folio Investing to buy notes. I checked out their website and they offer many ready to go accts, but I didn’t see anything regarding p2p. Do you have any knowledge of Folio?

thanks!

Simon, thank you for this honest information. I just started an account with Prosper a month ago and have just seen my first payments come across. I only invested $1,000 to start as I was leery in this new realm. However, between the returns and your info, I am very excited to invest more. Thank you!

My pleasure. Thanks Eric. Just remember that investors need around 200 notes to be diversified. Or 80 A-grade notes.

Hi Simon,

I just saw you r returns at LC. I am a new investor at LC but I am between 7%- 7.5%.

Can you give a feet back on filtering. What are the best filters to bust the interest earned?

Thank You and keep up the good job

Great post thank you