To encourage more people to start investing, each quarter I post the current state of my personal peer to peer lending accounts.

Because of my age and life-situation, I am an investor who feels comfortable taking on more risk. While this means my returns are higher than average, it also means my portfolio is more susceptible to macro economic factors like a rise in national unemployment.

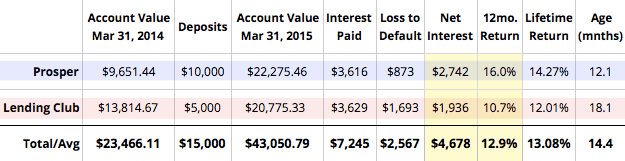

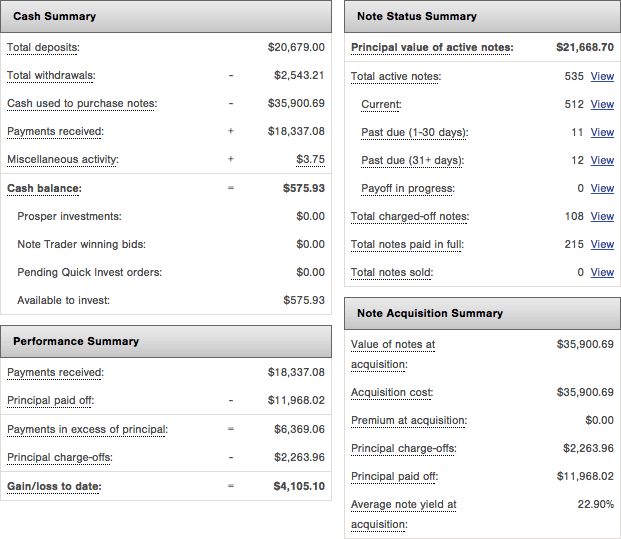

Q1 2015 Breakdown (Trailing 12 Months)

I continue to celebrate great returns at both Lending Club and Prosper:

Some notes on these returns:

- Account values, defaults, and interest are pulled from each platform’s monthly statements (See your Lending Club Statements / Prosper Statements).

- The important figure of Net Interest (highlighted in yellow) is calculated by taking the Interest Paid over the past twelve months and subtracting that period’s Loss to Default.

- The 12 Month Return, also highlighted in yellow, is done via XIRR (see: XIRR calculator), the best way to independently calculate your peer to peer returns. Most investors will probably not need to go to such lengths, and can trust the onsite return at Lending Club or Prosper.

- With an average age of 12 months, the notes in my Prosper account are not yet seasoned. Read: The P2P Return Curve

- All earnings are pre-tax.

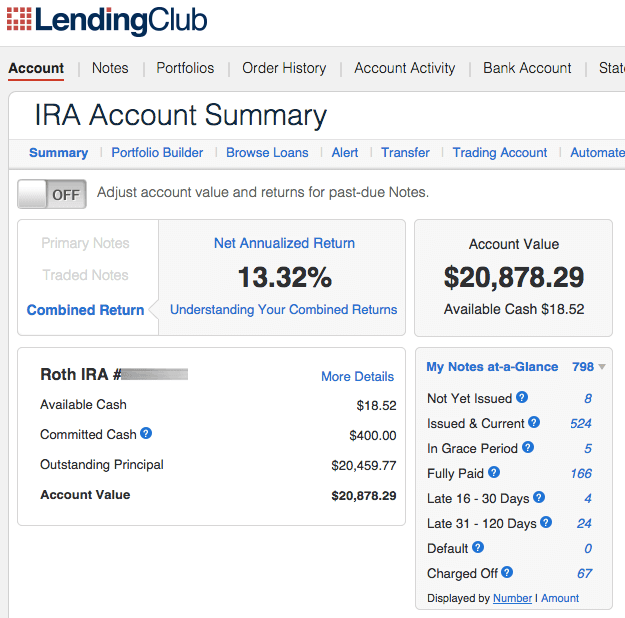

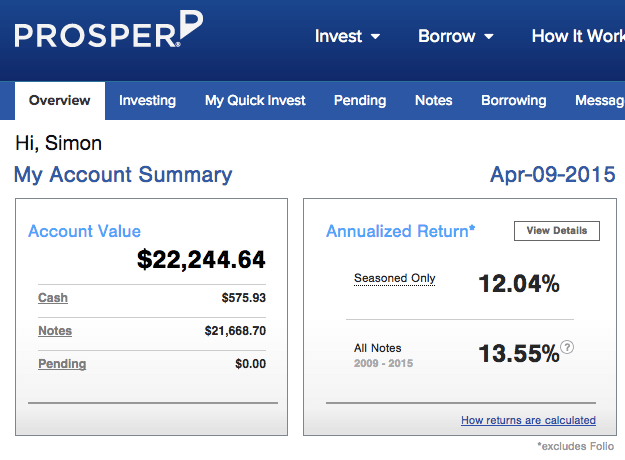

Lending Club IRA: Earning 10.7% Interest

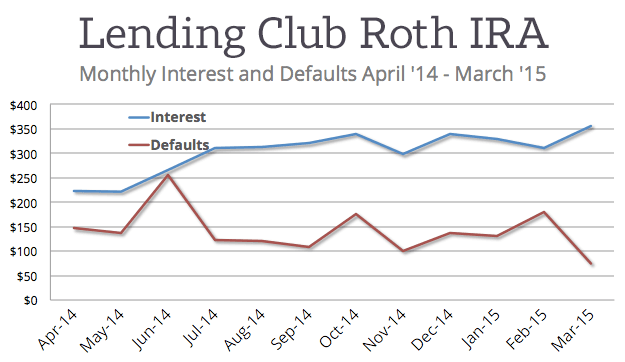

My Lending Club IRA remains an incredibly consistent and rewarding way to save for retirement. The TTM return actually increased by 60 basis points over last quarter, reversing a downward trend. Pretty much since July, this account’s monthly interest and defaults have stayed consistent, with a generous spread between them responsible for the account’s ROI:

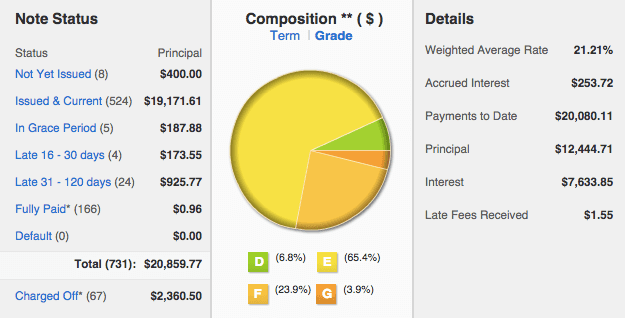

Here’s a further breakdown:

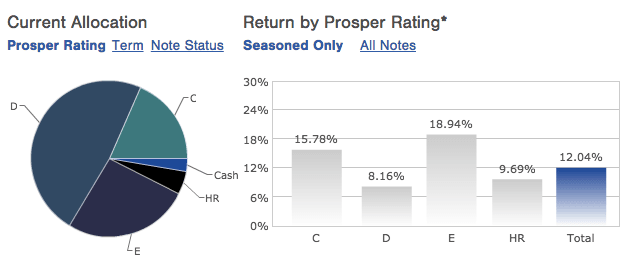

I’ve been playing around with the idea of leaning into some less risky grades, like increasing my account’s portion of Ds. I’d prefer to do this if it was obvious we were headed into another recession. The market collapse of 2008 actually spiked unemployment later in 2009 (the main national factor related to p2p defaults). Theoretically, knowing we’re headed into a recession could give investors like myself a chance to back away from E/F/G grades before they get hit with unemployment. However, I’m not convinced that recessions can be spotted so easily. More likely, I’ll probably continue to stick with what I’ve been doing.

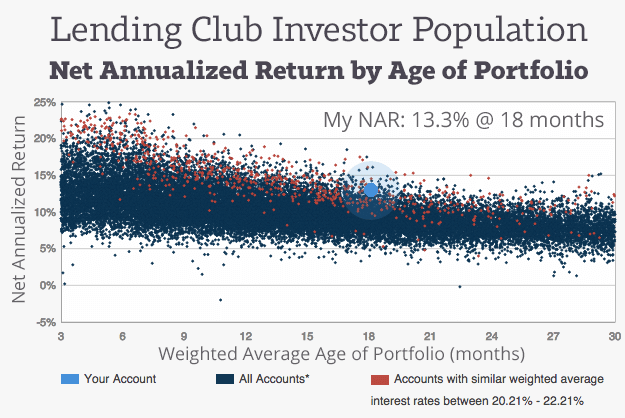

This month marks a significant milestone in my peer to peer lending journey:

My Lending Club account is finally seasoned, meaning my average loan was issued at least 18 months ago. As seen in the chart above, the impact of borrower defaults on lender returns is most heavily felt between months 1-10. But by month 18, the downward trend typically normalizes. This, of course, is unrelated to other factors that could impact defaults, like a sudden rise in national unemployment.

That said, I am dubious of my dot on this chart. This is because 90% of my notes are in 5-year loans, which have a much longer curve than 3-year loans (see this graphic). Like I mentioned last quarter, I still feel my eventual return will settle around 9%.

[Update 4/11/15: As pointed out by Larry in the comments, a large portion of this account ($925 of principal) is in loans 30+ days late. Typically just 28% of principal in 30+ day late loans is recovered. IE: if I click the “Adjust account value for past-due notes” button in the graphic above, my NAR drops 2.4%, so it seems this account is primed to be hit by defaults in the coming season.]

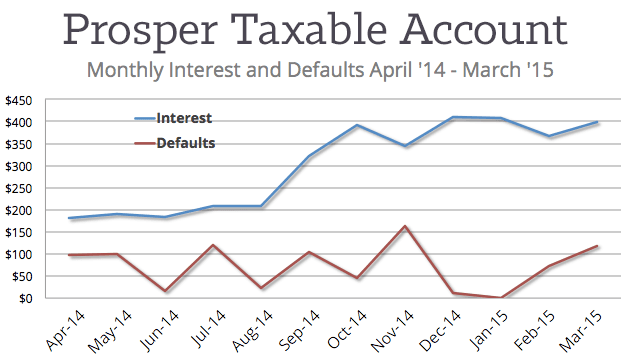

Prosper Taxable: Earning 16% Interest

Holy cats. Last quarter my ROI blossomed to 14.5%, which I attributed to the $10,000 investment I had made earlier, but which had not had the chance to get hit by defaults. I had predicted this month would be hit by a new population of non-paying borrowers. Instead, my defaults actually went lower, and the 12-month ROI shot to 16%. Check out that spread:

Here’s a further breakdown:

As I said last quarter, this return is unsustainable (though welcome while it lasts). Defaults should climb in the coming season to a more realistic $150/month or so.

I continue to be really happy with my Prosper account. Their wider credit spectrum gives me a higher average borrower rate than Lending Club (22.9% vs 21.2%), which I feel is most responsible for the higher ROI. On top of that, I feel Prosper improved its underwriting model over the past year with PMI-5, so the lower default rate could be positively impacted by that as well.

Am I Really Earning 13% in P2P Lending?

I’d like to tell everybody that a 12.9% is the new normal, that consumer credit is this fantastic new bastion of soaring yield. But this simply isn’t the case. To get this high return, a number of things have had to happen:

- A high personal risk tolerance (E-grade loans could be hit hard in a recession)

- My accounts are not fully seasoned: 5-year loans @ 14 months are no indication of how things could look a year from now.

- Tight filters that match few available loans (see my filters here)

- A lightning fast 3rd-party API tool to grab these scarce notes (NSRInvest)

- A low unemployment rate of 5% (see BLS)

- Perhaps a bit of luck

This bonanza could completely change in 12 months. But even if it does, I will likely remain a huge fan of this investment. It is my conviction that every investor nationwide should have a notable portion of their overall portfolio in consumer credit, and to do any less is a significant lost opportunity.

Almost 10% of your portfolio at lending club is between 31-120 days late. What percentage of this bucket has been charged off in the past?

Typically the majority of 31-120 loans do indeed default (maybe 80%?). Also, this is a much larger portion of 31+ days late loans than any previous quarter. I think you’ve correctly predicted my LC account will be hit by an increase in defaults in Q2.

At 80% your returns are really getting hit. These are five year loans? I looked at your two previous quarters and the percentage >30 late is increasing at an alarming rate. You should do a quarterly static pool analysis. Assume that 80% greater than 30 default and then look at your remaining exposure for the pool. You might find that your returns are significantly lower than you think.

Definitely true. If I click the “adjusted NAR” button at Lending Club, my overall return is discounted by 2.43%. So my account is definitely primed to get hit in the coming quarter or two.

See more about adjusting returns based on loan status here: https://www.lendingclub.com/account/investorReturnsAdjustments.action

Updated the article to reflect this.

The tool was very useful-thanks. Are the returns net or gross of fees?

The account values above were hit by fees, so the ROI I cite includes them.

Great update!

It will be very interesting to see how an aggressive notes portfolio like the one you have going performs in a recession.

I finally got some new money transferred over to my prosper account this month and invested. Nothing compared to your $40K portfolio of notes. I only transferred and invested $500 this month into 20 $25 notes with AA or A ratings.

I plan to invest another $250 to $500/month through the year, unless I see other opportunities I want to take advantage elsewhere.

Cheers!

Thanks Dominic. Awesome to hear you’re testing the waters. Let me know if I can help.

Great article Simon!

Have you ever tried BTCjam? They do peer to peer lending with bitcoin.

Hi Tom. I have not. But I know others who have, and they seem to report good things. What do you like about it?

Well I’m a big bitcoin fan, so I like that they use Bitcoin for investing and for providing the loans, and I think that will make it cheaper on the back end (no investor’s fees).

It also reminds me of Kiva, in that unlike Lending Club or Prosper, with BTCjam you can invest globally.

It’s still in the early days, but I think peer to peer bitcoin lending will be just as disruptive as peer to peer lending….

Thanks for the reply!

— Tom

Full Disclosure: I do work for BTCjam, so take all this with a grain of salt. ;)

Simon,

I just got introduced to Lending Memo. After reading a few of your articles my biggest question is, are the returns you are quoting from p2p lending pre-tax or post-tax returns? They seem to be pre-tax returns (but I’m not 100% sure). This could really change a lot of your analysis in my opinion. An 8.8% annualized return becomes 6.3% if your marginal rate is 28%, whereas many stocks grow more or less tax free (depending on dividends vs. buy-backs) until you sell them. P2p could be an attractive option for tax advantaged accounts (as long as you don’t have to pay some outrageous annual fees), but the tax-inefficiency of an investment account could make it less interesting.

These returns are pre-tax.

I am just testing this. If I initially invest only $500, how long should I invest for a minimum? Can I take all the money out of it if I do not like after a period of 6 months?

Can I transfer some money from my Roth IRA at Fidelity to one of these accounts in another Roth IRA? Can I talk to somebody on phone for some of my questions?

Yes you can.

So, how does it look in 2016?

Solid

Do you only use NSR invest? As opposed to finding loans on lending club or prosper directly.

Correct, I don’t log into the websites but use NSR to automatically find loans for me.