Today marks the completion of my eight month study: The Liquidity Project. Every week, from May 2013 through January 2014, I gradually discounted my taxable Lending Club account until it was completely sold off. The resulting data paints an extremely interesting picture of the secondary economy that exists in this backsection of the Lending Club website.

The Problem: P2P Lenders Have Struggled to Liquidate Their Accounts

Peer to peer lending has often been celebrated for its liquidity. Not only are its returns more stable than the swings that often characterize the stock market, and not only are the returns incredibly lucrative in the face of more traditional investor yields, but the secondary markets on Lending Club and Prosper have contained an avenue for people to sell off their investment if they ever need the cash. As a result, many proponents of this asset class, myself included, have proclaimed that peer to peer loans contain good liquidity. We feel that if someone needs to exit this asset class without taking too big of a hit, they can do so.

The problem inherent in this claim is that little proof exists to support it. Also, the wider investor community’s experience has often been quite variable and unconsolidated. In short, there has been a lack of hard data to help investors correctly price the notes they are trying to sell. As a result, investors seeking to exit peer to peer lending have often struggled in how to begin liquidating their accounts.

The Solution: An Eight Month Study on Foliofn Liquidity

The Liquidity Project (as initially outlined in this post) is a first-attempt at establishing a baseline for account liquidation. By gingerly lowering an entire portfolio’s price on Foliofn (the secondary market for Lending Club loans), each individual note’s markup became solely dependent upon its quality and characteristics alone. As a result, particular markup/discount thresholds could be identified so as to help future investors quickly liquidate an entire portfolio while still earning a respectable markup.

Methodology: Create a Sell-Calendar, Record Note Sales, and Analyze

My first Lending Club account was chosen to be liquidated for this project, an account containing 35 active notes worth around $1,000.

(click to zoom)

Starting the 29th of May, I listed all these notes for sale at the maximum possible markup (+50%). Following a selling calendar, I lowered the markup on these notes every three days until the account was liquidated.

Starting the 29th of May, I listed all these notes for sale at the maximum possible markup (+50%). Following a selling calendar, I lowered the markup on these notes every three days until the account was liquidated.

- From a 50% markup to 20%, the premium dropped 2.5% every three days until July 4.

- From a 20% markup to 10%, the premium dropped 1% every three days until August 3.

- From a 10% markup to 6%, the premium dropped by 0.5% every three days until Aug 27.

- From a 6% markup until every note was sold, the premium dropped by 0.25% every three days.

The project ran eight months, with the final note selling January 29, 2014. The portfolio’s markup/discount had adjusted 50 different times. Since Lending Club auto-renews the Foliofn listing whenever its price is updated, every note remained for sale on the platform for months at a time, from late May until every was sold.

Note: Originally I had 40 notes in this project, but five went late or were paid off, so only 35 were used. Also, my original intention was to sell a comparable number of Prosper notes the same way, comparing the liquidity of one platform against the other. Despite identifying these notes and opening their sale on Prosper’s Foliofn section, I gave up this goal when I realized how Prosper’s site frustratingly does not renew listed notes when they are repriced. Having to dig through my entire Prosper investment for specific notes (no portfolios) every 7 days was too tedious. As a result, this study became only focused on Lending Club.

Four Major Insights into the Lending Club Foliofn Secondary Market

As a reminder, all of these sold notes contained a Current status. The markup/discount was calculated from each note’s outstanding principal.

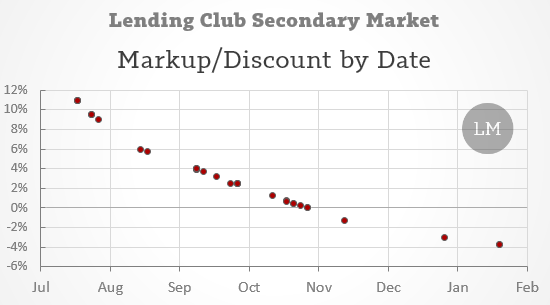

Insight #1 – Notes with ‘Current’ status sell from an 11% markup to a 4% discount

Even though the project started in late May, two months went by without a sale. But in July a number of low-grade notes were the first to sell, earning a surprising 11% premium. The project continued until late January, when the last sub-par notes were sold at a -3.75% discount.

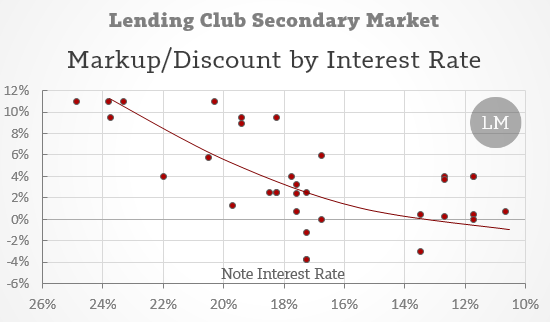

Insight #2: Notes with higher interest rates sell at higher premiums

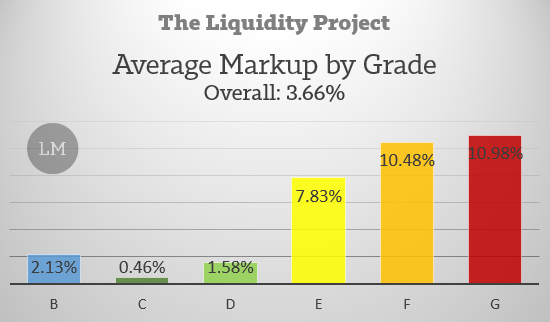

The above graphic demonstrates how the notes with higher interest rates were in greater demand, and earned a higher premium on Foliofn. This can be seen more easily in a breakdown of average markup by loan grade:

E, F, and G-grade notes earned an incredibly high markup, the Fs and Gs selling with a 11% markup to their outstanding principal. B-D grade notes earned far less than this. It deserves mentioning that there were more D grade notes (16 D vs 9 E-G), so their markup may be more accurate of the market as a whole.

Surprisingly, the entire portfolio was sold at a 3.66% markup. After 1% in fees, this account was liquidated while earning a 2.66% premium. While no seller should ever take eight months to liquidate his portfolio, this 2.66% result does propose a best-case scenario and baseline for future investors (including the Sacramento Method below).

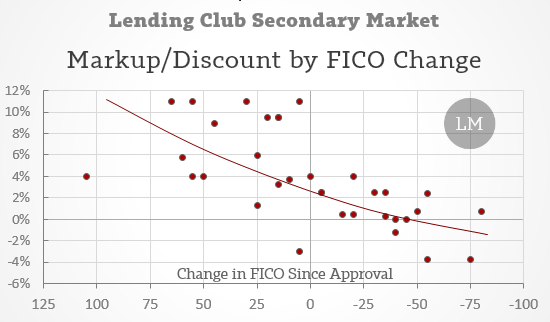

Insight #3: Notes with healthier FICOs sell at higher premiums

This result was my favorite of the bunch. I would even go so far as to say that the beautiful curve of this chart makes the entire eight-month project worth the time. I am not sure what the implications are of knowing that sell price is so deeply tied to how a borrower’s FICO has changed. Perhaps it just further encourages us to improve our initial loan selection criteria so as to imbue our overall account with as many quality borrowers as possible.

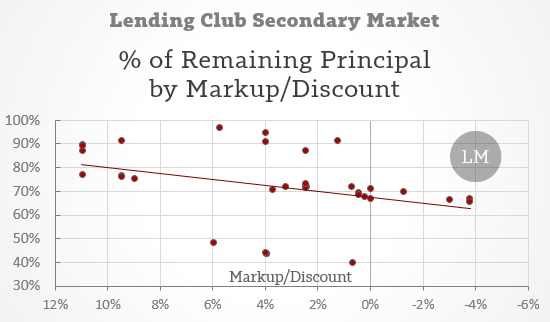

Insight #4: Notes with more outstanding principal may fetch a higher premium

This seems the loosest insight, but purchasers of notes on the Lending Club Foliofn secondary market seem eager to find notes with a greater percentage of outstanding principal.

Further Research is Needed

While this project seemed to use decent methodology, it could be improved upon. First and foremost, the number of notes in this experiment (35) were too few, though I am pleased that this data contains good correlations despite this weakness. However, a similar study with hundreds of notes would give far clearer results. Secondly, additional statistical factors could be interesting to look at, like number of missed payments, loan term, and note size. A larger liquidated portfolio that contains a mix of sizes and terms would be ideal. Thirdly, this project did not include A-grade notes. Finally, it would be really interesting to do something similar with notes that have gone late. I was able to do that with a single note during this project. A single D-grade Late note with a FICO drop of -175 sold at a 49% discount.

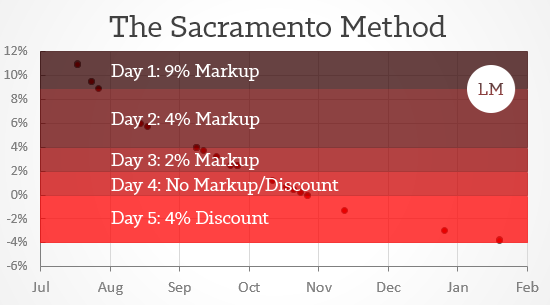

How to Quickly Liquidate Your Account? The Sacramento Method

Most people who are trying to liquidate their account are attempting to do it in the quickest manner while also earning as much premium on their healthy notes as possible. As a result, I would like to theorize a five-day liquidation method based on this project’s results: the Sacramento Method.

Named after its five sell points (a zipcode in Sacramento, CA is 94204), this method prices notes at five efficient markup/discount points so as to liquidate an account in less than a week while still garnering a respectable premium.

- Day 1: Price notes with a 9% markup over outstanding principal

- Day 2: Offer a 4% markup

- Day 3: Offer a 2% markup

- Day 4: Price notes without a markup/discount

- Day 5: Offer a 4% discount

If I would have used this model, I would have drastically lowered my sell time while still earning a 2.7% markup on my portfolio. Minus fees, this method could theoretically have liquidated my entire account and earned me a net 1.7% premium in just 5 days. Of course, there is no guarantee that Foliofn performs the same way today as it did back then, but it is possible.

The reason I feel confident in the Sacramento Method is for the way it first makes space for high-markup notes, spends three days cutting the common markup arena more gradually (4/2/0), and finishes by catching discountable notes. This method seems more effective for accounts containing a medium to high degree of risk, since this is what it was built around (project’s avg. interest rate is 17.2%). It will probably be less effective for people who have low-risk portfolios containing many A-grade notes.

Disclaimer: This Method is Conjecture

It is worth repeating that this entire project, its data, and its method was based on a small sample size (35 notes), and as such, its overall quality is speculative. Foliofn is a turbulent environment that requires a far more rigorous project than this one before any real conclusions can be made. Furthermore, even if this project had a decent sample size (800 notes or more), no method or theory is a guaranteed way of liquidating your account at an overall premium.

However, I am willing to posit the Sacramento Method as a preliminary standardized approach to account liquidation, and I am eager for more rigorous studies in the future to prove it wrong or uphold its conclusion.

Download the Liquidity Project Data

The Liquidity Project (results).CSV (right-click & Save As…)

[image credit: Kyle May “DIY Fake Ice Cubes” CC-BY 2.0]

Great write-up. Thanks for all your work. It really is proving helpful to this novice P2P lender.

I was forced by mother nature (a flood and a basement were involved) to liquidate last April. I had a modest amount of newish notes on hand – about 30. I believe i had 100% cash in hand within 10 days with less than a 2% loss. I was happy with those results given the circumstances.

My pleasure Josh. Bummer about your flood, but it looks like your discount wasn’t too steep.

Really great job Simon. I know what a huge amount of work this Liquidity Project was and appreciate you sharing it with the p2p lending community.

My pleasure, Peter.

Thank you for bringing my previous error to my attention. This is truly ground-breaking information.

I have been winding down a Prosper.com portfolio for about a year, finally firing the last 24 notes all at once onto FolioFn with a 2% discount.

I can corroborate your four observations in my own auction results.

That’s great Ross. So interesting. If you would be willing to share your overall results in a comment here, I would be much obliged.

Hi Simon,

Okay a little more color on the liquidation of my small Prosper portfolio. Of the 24 notes I offered at a 2% discount, only two (2) failed to attract a single bid.

Of the others, about half attracted multiple bids with about 1/3 of those selling for a premium. I found that the higher the interest rate, the greater the premium attracted. High yield notes are favored on the secondary market. I think that having the HY notes seasoned by 6-12 on-time payments increases their value on the 2nd market, sometimes fetching up over 2.5% premium to value.

The two notes that failed to sell were listed at a 4% discount. One sold for 2.8% discount, the other for 1.8% discount. These were loans with lower yields.

Overall, I found that if I was willing to start by offering a small discount (2%) to attract buyers interest, I could easily liquidate a portfolio within a month and that many loans would get bid to fair value anyway.

You don’t have to get skinned by suddenly having to liquidate your p2p portfolio. The second market is robust enough that with some patience you can exit with minimal losses.

This is really helpful. Thanks Ross.

Nice work here Simon, and heck of a lot persistence given the time required. Thank you for following through with this project. When selling notes in the past, I’ve come to some of the same conclusions you on the initial interest rate. I was shocked at some of the premiums I was able to get for some lower rated notes given how much lower the yield to maturity would be for the buyer. Essentially you’re taking Lending Club’s credit model and saying they are off by X% and I don’t think the underwriters at Lending Club are that off when initially pricing.

I will note that given that you only sold 35 notes, there can be some risk in making too many conclusions. Certainly those 35 notes were filtered prior to acquisition, so someone else’s notes might bear different inherent risk levels from having a different credit profile. Additionally, given the size of the secondary market, 35 notes over the course of eight months is a fraction of a fraction of the notes sold during that time frame. Lastly, the overriding assumption here is that the secondary market is an efficient marketplace, therefore the notes sold back in July would have sold for the same amount in January.

Either way, thanks again for publishing your results and going through with this exercise. I have found in my own experience that liquidity can be had fairly quickly if needed, but pushing for an overall premium might not be the right scenario for those looking to cash out quickly.

Thanks Adam,

Agreed. I tried to emphasize at the beginning of the piece that these results are very preliminary and first-attempt. The goal was to create a baseline so further work could be done (IE: mimic my methodology). However, while I do see correlations within the results (IE: interest rates and FICOs tied to markup), I agree that the overall project is weak as a result of its low sample size. So, yes, my results may not be indicative of the market at that time, and considering the Foliofn market seems to deeply swing in its character throughout the year, these results may not hold any water for the future at all.

That said, I feel confident enough with the overall picture to make some preliminary conclusions. While this study is not overtly authoritative, it does allow for some hazy conjecture.

The Sacramento Method is that sort of conjecture. I am more than willing for it to be proved wrong in the future by (1) its attempted liquidations result in being sold with an overall loss or (2) a better Foliofn study that contradicts it. That said, I am eager to posit this method as a decent starting place (especially considering none currently exist). I am willing to (lightly) assume that additional more-rigorous studies might corroborate my conclusion/method. Indeed, I would push back against your conclusion that lenders should not expect to earn a premium with quick liquidations. I feel that, while the premium might be quite small, the coming years could reveal a somewhat standard liquidation process that earns a small premium the majority of the time. Prime consumer credit seems to possess such quality.

Per your comment, I added a disclaimer to the conclusion of the piece.

Cheers,

Simon

Without a doubt, further studies will certainly help, and should shed light on the efficiency and valuation set by the market. The current environment is still so dynamic (just look at the changes within Foliofn since you started this project) that so many assumptions made today might not be the case in six months, a year, or more. Things like the IPO, modified loan underwriting (Policy 2 loans perhaps) or improved filtering would potentially alter the assumptions significantly. However, as I said in my first paragraph, there are things you’ve identified, like the premium people will pay for low rated notes, that will likely hold true to some degree.

As for expecting an overall premium for a quick cash out, I think it is a premature conjecture at this time as your experience was highly dependent on the underlying portfolio. You were selling low-rated notes primarily, something in high demand on both the secondary market and for the initial issuance. As you’ve said in the piece, this probably was a factor in your ability to generate such a high premium, however, even all low rated notes aren’t the same, otherwise we wouldn’t filter.

As an aside, it would be amazing to get a look at the data that already exists within Foliofn’s servers, but alas, we are not heading in the right direction from a transparency standpoint with P2P lending! If there is still an arena of P2P lending that could use a tremendous overhaul and increased transparency, the secondary markets are that place.

somewhat unrelated – but maybe you could point me in the right direction:

Know of any statistical data regarding loans that have been ‘in grace’ or ‘late’ but been ‘pulled up’ to ‘current’ ?

I peg an ‘in grace’ note at a 10 to 20% discount depending on ‘days out’ – but I’d like to know how to value those that do eventually end up paying. I’ve had ‘Folio sales’ cancel because of payment – but what to do with them then ? My feeling is that they’re riskier having established some payment problems. How much riskier ? What discount (if any) do they rate when placed back up for sale in Folio ?

Very interesting article! Thanks for going through with the study. It is true that a lot of claims made to promote the p2p platforms cite the liquidity without any prior data to back it up.

While you acknowledge your sample size was small, it prompts a different question for me. If we extrapolate those results out to a portfolio 100x your original 1000 USD will that translate into similar results? Or, due to fewer players in the secondary market, will it extend your sell off time exponentially? I think right now it is the latter. In my opinion, if it takes you several months to empty your position, I would not call that liquid at all…I mean, you can sell a house faster than that. I would hope that the platform is dealing with a quantitative issue rather than a qualitative one.

On the bright side….when both major players IPO I think that will draw a lot of needed scrutiny to the platforms and will result in several interviews with guests about the secondary market. Hopefully this occurs with just LC or Prosper IPO rather than both of them as a prerequisite.

I also hope someone sponsors you a 100k so that you can add more data. This is all very interesting!

I’d love to see some R^2 values on your trendlines. The data is amazing though! Nicely done.

Simon.

Thanks for this great write up!

Very we’ll written and will be very helpful for the people that consider liquidating their accounts.

I always look forward to reading your posts!

Fascinating. I’ve never listed a note with that high of a markup – I start at 4% and drop by 0.5% per week. I have a somewhat larger portfolio, ranging between $3K to my present $14K. I list tens of notes at a time, with moderate markups, and have never had a problem getting the sales I needed for my liquidity needs, meeting my goals within a week or two of initial listing.

I have noticed as well that loans with better FICO scores sell much faster. I have not had particular issues selling notes that were closer to paid off versus notes with many more months still in duration.

I\’m trying to repeat a similar experiment with a portfolio containing about 1700 notes. I was going to start with a 14% markup but when I use foliofn\’s selling interface and set the markup to +14%, many of the notes show a negative yield to maturity and I receive the following error when trying to list them, \”Notes cannot be listed at prices that result in a negative Yield to Maturity for the buyer. Please adjust your price before listing. \”.

Any ideas how I can streamline the process? Manually repricing the several hundred or so is to tedious for me to repeat every couple days when I want to re-bulk list at a lower markup. Is there any way to import a csv that specifies the list price for each note?

Also, wouldn\’t it make more sense for foliofn\’s bulk price-setting feature to allow you to specify a % yield to maturity rather than a % markup? Presumably Yield to Maturity is also a more interesting metric for the sake of our analysis and determining how to price notes, right?