This morning I woke up, had breakfast, brushed my teeth, and began my day. To start, I checked to see how my peer to peer investments were doing. Logging into my accounts, I noticed that hundreds of people that I had lent $25 were paying me back, and most were paying on time. Satisfied, I shut off my computer and began my day.

Just ten years ago, peer to peer lending did not even exist. But these days, hundreds of thousands of people have been impacted. Even major news organizations like CNN and the New York Times have joined the discussion. If you’re curious about how to get involved, this article was written for you.

What is Peer to Peer Lending?

Let’s begin with a definition. Peer to peer lending (also known as p2p lending) is the large-scale lending of money between people online. It’s exactly what it sounds like — peer to peer, person to person lending, except done by thousands of people working together.

At its most basic level, peer to peer lending actually is not much different than just lending money to a friend. You have one person who has extra money and one person who needs to borrow it. But when lending money to a friend in real life, the trust and familiarity between the two people helps them feel comfortable that the money will be paid back.

When lending is done on a large scale, we don’t have the ability to get to know 1000 people by name. Instead there are two companies (Lending Club and Prosper) that help thousands of borrowers and lenders connect to each other. These companies secure the relationship between borrowers and lenders.

When lending is done on a large scale, we don’t have the ability to get to know 1000 people by name. Instead there are two companies (Lending Club and Prosper) that help thousands of borrowers and lenders connect to each other. These companies secure the relationship between borrowers and lenders.

- They make sure every borrower has good enough credit for a loan

- They help investors lend money to the borrowers

- And then they help borrowers pay the loans back to the investors

Pretty simple, right? Let’s talk about why this is new and exciting.

How a Peer to Peer Loan is Different than a Bank Loan

The main difference is cost. Like MP3s are a cheap way to deliver music to people, peer to peer lending is a much cheaper way to give people loans.

Banks have to pay for:

- Computers, websites, professionals

- Over 100,000 employees

- Branches in thousands of cities in the United States (vaults, electricity, tellers)

Peer lending companies pay for:

Peer lending companies pay for:

- Computers, websites, professionals

- Less than 1000 employees

- Two or three different locations

For example, one of the largest banks in the United States, Wells Fargo, has 270,000 employees and 9,000 branches nationwide. But a peer lending company like Prosper has just 240 employees spread across only a few locations. So you can see, Prosper has a much smaller footprint. Like Lending Club, it operates almost entirely through computers, so it is much cheaper to run than a bank. And this low-cost is the driver behind p2p lending’s incredible success.

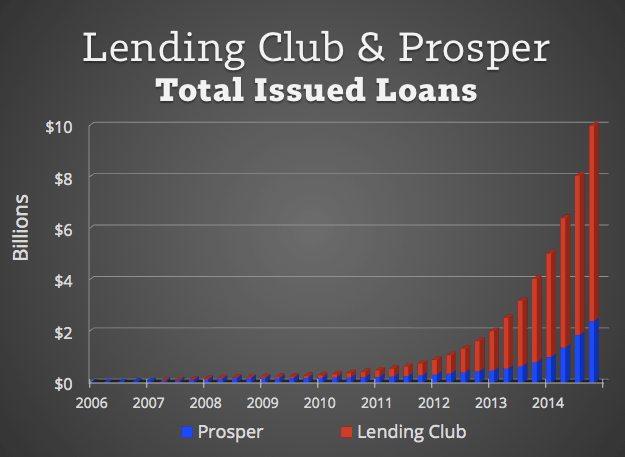

These companies have experienced incredible growth in recent years. For example, it took Lending Club over five years to issue $1 billion in loans. Today they are issuing this amount every two months! Amazing.

But how does this benefit you personally?

Since these companies operate so cheaply, they pass the savings over to us, their customers:

- Borrowers get the lowest rate for an unsecured loan in history

- Lenders earn a great return in a brand new asset class

Let’s look at these one by one.

Borrowers: 4 Reasons to Get a Peer to Peer Loan

Here are the top four reasons to get a loan through Lending Club or Prosper:

Reason #1: Lowest interest rates in the country. Period.

Like we mentioned earlier, since Lending Club and Prosper both operate through websites, they can offer their borrowers very low rates on their loans. For example, most borrowers get a rate 5% lower than their credit card. This rate can mean thousands and thousands of dollars in savings over time, just by clicking a few buttons and moving your debt to a peer to peer loan.

If you tried to get this same rate with a bank, most of them couldn’t come close. In my opinion, the choice is simple.

Reason #2: Your rate will never go up.

Unlike a credit card, these loans have a fixed-rate. What that means is the rate will never go up, even if you’re late on a payment. So if Lending Club or Prosper offers you a 9% interest rate when you get a loan, you will pay 9% until the loan is repaid. These companies will never raise your rate. Even if you’re late with a payment, your interest rate will always be 9%.

Reason #3: The application is simple and fast.

Back in the olden days when people churned butter in barrels and rode those bicycles with the big front wheel, going to the bank was a full day affair. You had to get up before dawn and ride miles into town. You might spend all day at the local bank, arriving home after dark.

Today, going to a bank can still be a hassle. My brother got a mortgage a few years ago, and he had a long string of meetings with the local bank for weeks before they gave him the money.

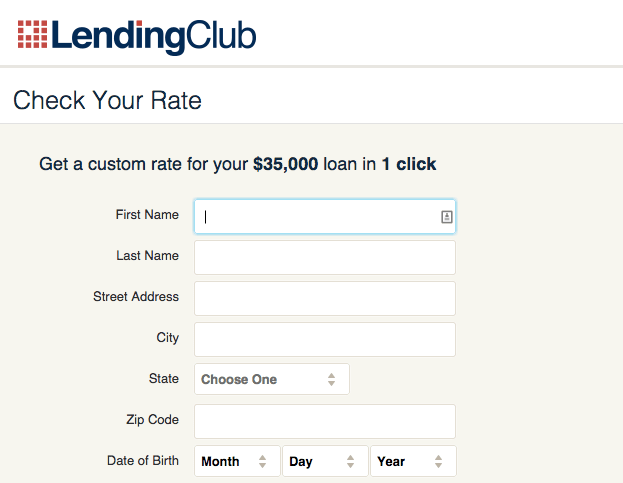

Lending Club’s application is simple.

A peer to peer loan, on the other hand, is quick and easy. You simply go online, fill in your info, submit some documents to validate your identity, and (if approved) the money is electronically moved to your checking account. When I applied for a Prosper loan, they had the money to me in just four days. And I applied in my living room wearing pajamas.

Reason #4: Low late fees and no prepayment penalty.

Finally, peer to peer loans have much lower fees than most other options. If you’re late on a payment, the fee is typically around $15. Secondly, if you want to pay the loan off early, you can do that for free! Always a great option. Avoid as much interest you can and prepay your loan.

Conclusion: If you need a personal loan, consider Lending Club or Prosper

Hopefully you don’t need a loan. Hopefully your job and savings are doing enough to keep you afloat. That said, sometimes people are carrying debt on their credit cards, or suddenly need to pay medical expenses and don’t have the cash. In these situations, getting a p2p personal loan may be their best option.

Loans up to $40,000

Check your rate at both, go with the lower rate.

Won’t hurt your credit score.

Investors: The 7 Benefits of Investing in P2P Loans

Investing in peer to peer loans is a bit more complicated, but it is more revolutionary than the borrowing side of things.

Benefit #1: You can earn a great 5-9% return

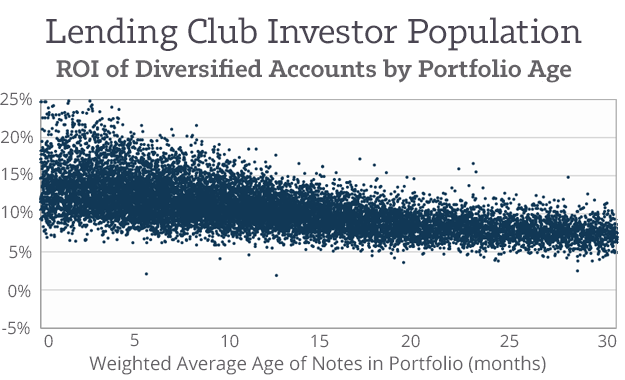

Ultimately, the reason we invest our money is to earn a return (the yield). And peer to peer lending offers investors a great return. Most seasoned accounts (18+ months old) stabilize at a 5-9% return, depending on how much risk is taken on. Investors who take on little risk earn closer to 5%. Investors who take on more risk can earn closer to 9% (see my returns).

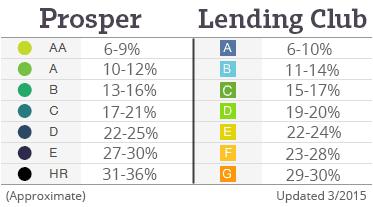

Choosing a level of risk is easy. Every borrower is rated for how risky they are, with higher grades (like As) being safer and lower grades (like Es) being riskier. A-grade loans are much less likely to default, even in a tough national economy. With E-grades, the interest rates are much higher (above 20%), but they default more often, particularly in a bad national economy.

Choosing a level of risk is easy. Every borrower is rated for how risky they are, with higher grades (like As) being safer and lower grades (like Es) being riskier. A-grade loans are much less likely to default, even in a tough national economy. With E-grades, the interest rates are much higher (above 20%), but they default more often, particularly in a bad national economy.

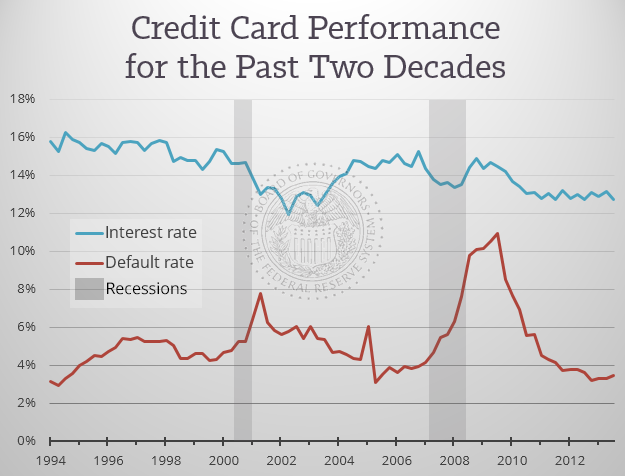

Your return will be the average interest rate of your borrowers (see chart above) minus the rate at which they default (don’t pay their loans back). Most borrowers get a 13% loan. The typical default rate is about 5%. Finally, Lending Club and Prosper take 1% in fees.

13% loan rate – losses (1% fees + 5% defaults) = average 7% investor return.

Benefit #2: This new asset class is much more stable than the stock market

The stock market has returned investors a much higher return over time (about 10%) than peer to peer lending, so what makes this investment worth your time? Stability. In 2008, the stock market had a massive crash (losing around 35% of its value). But peer to peer loans never lost their investors money. This is because peer to peer loans are part of an asset class called consumer credit.

Credit cards are simply another form of consumer credit. As seen in the chart above, the default rate (red line) never touched the interest rate (blue line) in the crash of 2008 either. This is why banks are so excited to give people credit cards – they are nearly a guaranteed positive return.

Peer to peer lending is the first time in history where average people can invest in the trustworthy asset class of consumer credit. By diversifying your investment across 200 different borrowers, you will begin to mirror the overall default rate, gaining stability and consistency within your account.

Benefit #3: The investment is simple

People need loans. You simply help fund their loans. At its core, that’s all peer to peer lending is. As a result, investors like myself feel this investment is easier to understand than most other investments. The average American has trouble telling you what a bond is, and will likely get confused about how to begin stock trading. But handing out a $25 loan to a few hundred people makes sense.

Benefit #4: This can be a passive investment

As your borrowers repay their loans, you will have a flow of cash coming into your account. Both Lending Club and Prosper have automated options for this cash flow, automatically reinvesting your cash balance into new loans of your choosing. As a result, with just a little bit of work on the front end, your investment can become nearly passive. Your cash is reinvested for you while you focus on other tasks.

As your borrowers repay their loans, you will have a flow of cash coming into your account. Both Lending Club and Prosper have automated options for this cash flow, automatically reinvesting your cash balance into new loans of your choosing. As a result, with just a little bit of work on the front end, your investment can become nearly passive. Your cash is reinvested for you while you focus on other tasks.

Benefit #5: You can invest through a retirement account

Investing through a Lending Club or Prosper IRA allows your portfolio to grow tax-deferred. You can even rollover a 401(k) or invest with an SEP/Simple IRA. Considering p2p investments are taxed the same as interest in your savings account (30% for many), this can mean huge savings for your account over time.

Benefit #6: This investment is (somewhat) liquid

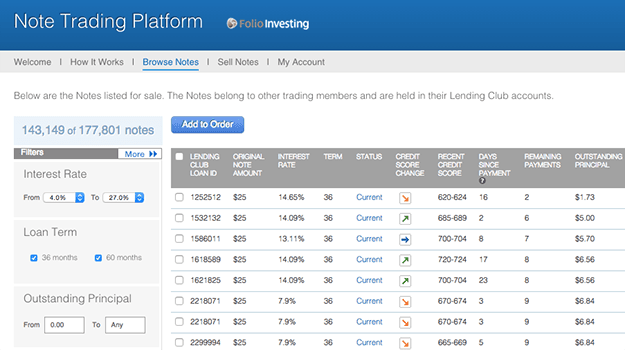

The SEC has classified peer to peer loans as a security, which means these investments can be bought and sold on a secondary market. While Prosper’s market is somewhat small, Lending Club’s secondary market (run through a company called Foliofn) is thriving, with thousands of loan portions (notes) being bought and sold per day.

Notes on Lending Club’s Secondary Market

As a result, you are able to back out of this investment if you don’t like it. To do so, you simply sell your loans on this secondary market and close your account. The process can be a bit complicated since it can be difficult to know what price to set on your loans, but overall the process is quite doable as long as your notes are small ($25 or $50 each).

Benefit #7: This investment sets people free

My favorite benefit: your money helps bring positive change in the world! People are cutting up their credit cards and paying down their debts through your invested cash. Families are becoming healthier, parents are less stressed, etc. I do enjoy the return and stability this investment offers, but nothing compares to the freedom it gives people who are struggling under ugly credit card bills.

Want to set people free from the credit card companies? Become a peer to peer lender! Read: Why Peer to Peer Lending is Beautiful

How to Get Started? Three easy steps:

Getting started as a peer to peer investor is simple:

- Open a free account at Lending Club or Prosper (read this comparison)

- Select your risk tolerance (read: What loan grades do I choose?)

- Invest across at least 200 borrowers (read: How to diversify your account)

Are you still uncertain? That’s ok. Read: How to Try P2P Lending with $2,000

[image credit: ‘Sun Netra‘ by thskys

‘Bank Vaults‘ by Jason Baker CC-BY 2.0]

Great post!

I am excited to see where these guys are in 5-10 years and see just how much they disrupt the ole banking business model. It will be another classic example of creative destruction.

Cheers

Thanks GYFG. Considering how groundbreaking the last 10 years have been (Zopa was founded in 2005), the next 10 should be just as interesting.

Great summary of P2P lending from the borrowers and lenders perspective.

Is been on my investment list for a while now, and this year is the year I finally jump in. So tired of <1% interest on my cash holdings.

Hear hear! Glad you’re making it happen Jack.

After making the initial $5000 investment for 200 notes;

Do I invest monthly?

If so, how much should I monthly after that initial investment?

Wow,

I Din’t Know About Peer To Peer At all now.

But now i can say You can be borrowers Or lenders in Both ways You’ll get Better pay for sure.

I am Thinking About investment In P2P. And as you say Lending Club is a Great Platform to do that.

Thank you for this Great Ideas.

Regards

Harry Watson

Great Work @simon

I Really Don’t Know About the Peer to Peer Landing But now i know.

Thanks to you.

I guess I can’t be a Lender but i have some ideas and i want Fund so i am sure with the Help of P2P may be i can Raise some Fund for me and My Business.

Thank you

Great Amazing Content #simon

No one ever Explained this Borrower and lenders Theories like you did, So. Congratulations on it.

Now, After Reading this I am Started Believing in Growth and i hope through this i do some growth so Thank you very much.

Thank you

This is a very good informative post that does an excellent job of introducing the concept of peer to peer lending. Thank you.

Excellent writing!

You are completely right. In my opinion, the best benefit of p2p lending is that Application process is online and simpler than ever. Borrowers can check their personalized rates within a few minutes anywhere and anytime. During the loan funding, borrowers can also track their funding progress about how much of their loans have been funded by the investors on a real time basis.

Thanks John

Insightful post indeed!

Peer to peer lending is an opportunity, where individuals do not have to use traditional banking. So if you need a loan, and you have good credit, you ask from peer to peer lenders, they evaluate the risk, and might give it to you with a low loan rate.