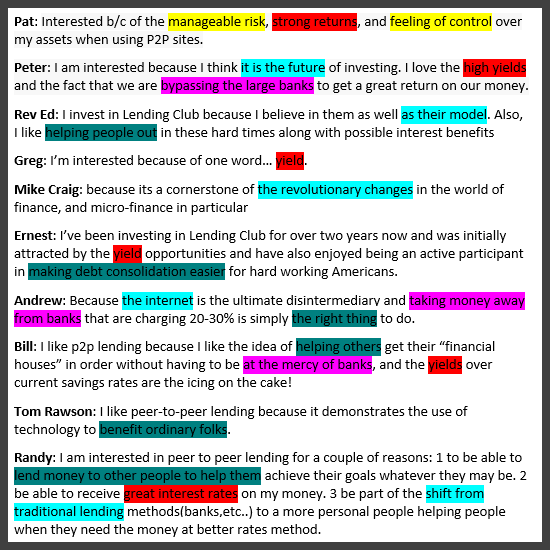

Last week we ran a reader survey asking people for the various reasons they are interested in peer to peer lending. There were 13 responses in total, with Mike’s 7th entry being randomly chosen to receive the Lending Club sweatshirt (with runners up Ed, Bill, & Randy). Congrats Mike!

The various responses were really interesting! Having looked closely at the feedback, I’ve categorized them under five major headings:

- Ethics (6 responses): What I enjoyed most was how enthusiastic people were about how peer to peer lending helps those in need. The goal to make money was often listed second to this value! I really enjoyed Ernest’s response the most. He spoke of how his initial interest in the high returns has morphed into a joy for helping others:

Ernest said, “I’ve been investing in Lending Club for over two years now and was initially attracted by the yield opportunities, and have also enjoyed being an active participant in making debt consolidation easier for hard working Americans.”

- Returns (6 responses): Of the two main reasons people gave, the other was the amount of money that can be made from peer to peer lending. Greg said, “I’m interested because of one word… yield.” With average returns of 7-15%, you can see his point.

- P2P Lending is the Future (5 responses): Many people seem happy to lend because traditional investing avenues seem to be less trustworthy, while a tech driven decentralized lending seems to be more and more trustworthy every year. As Peter Renton wrote, “I am interested because I think it is the future of investing.” Exciting.

- Bypassing Banks (4 responses): Interestingly, a large reason people remain interested is antagonism towards existing financial institutions. It seems like lenders are celebrating how technology leapfrogging the banks seems something like justice.

Bill said, “I like p2p lending because I like the idea of helping others get their financial houses in order without having to be at the mercy of banks.”

- Feeling of Control & Less Risk (1 response): Two additional reasons were given by Pat. One was a feeling of control over his finances that he does not feel when investing in traditional avenues like the stock market. The other was a feeling of lower risk on this investment. Both are solid benefits.

Here are all the answers with each of the five reasons highlighted:

Compared to Investing in the Stock Market

Let’s take a moment and examine these responses in full. The main takeaway I can see is how different they seem from the reasons we typically hear for investing. The main way Americans invest and save for retirement today is through the stock market: stocks, bonds, and mutual funds. Yet, when have you heard anybody describe their stock market investments as a way to help people? The stock market is not often referred to as a “revolution”. If anything, the average American sees the stock market as an aged overburdened source of frustration.

When most people save for retirement, the “responsible” thing they consider is yield, whether or not their investment will make them money, and thus it is typically a flat and emotionless action.

Contrast that to the answers of our survey! People certainly need some sort of yield, but are equally eager to help people out of credit card debt. People are excited to decentralize the banks and enter into a technological approach to finance. People are eager for the control P2P lending provides.

Functional Marriage Versus Romantic Marriage

This whole conversation reminds me of the spectrum that exists within marriage. Some couples in our nation today are married in a purely functional way. They do their housework as a team and pay their bills together. They even raise children. However, there is little romance between them as a couple, a celebration of the other person. They are more business partners, if anything. Contrast that to people who are in love, even decades after their marriage ceremony. While the relationship still functions efficiently, it is also a source of joy and excitement.

I see a purely functional marriage like investing in the stock market, and peer to peer lending like a marriage with romance. While the stock market has given a decent return over the past fifty years, its foundation of joy and gratitude is crumbling. Peer to peer lending, on the other hand, is arguably a return to the roots of lending as it has been for thousands of years. It is people meeting people, elegance within simplicity, and you can see that reality within the myriad of responses in our reader survey. While the function is valued by people (every investment, by definition, must include yield), it is not the sole reason we are here. On the contrary, the money we can make is simply the result of our interest and enthusiasm. For a nation plagued by volatile uncertainty, a tech driven decentralized efficient approach that helps people get out from under credit card debt is an exciting thing indeed.

Questions or comments? If you enjoyed this please Like or Tweet it below.

[image credit: littlebluepenguin “pencils (3)” CC-BY 2.0]

Simon – It’s great you are starting to get data like this. Lending Club was originally built on the social affinity concept and it is great to see that ethos carry over.

Seriously :)