Perhaps the most interesting part of peer to peer lending has to do with the practice of self-filtering the available loans to try and achieve higher than average returns. Filtering invokes a range of reaction from different people in the space, from quiet disdain to hearty celebration depending on who you’re talking to. It remains one of the few “hacks” we have, meaning it’s a way to boost returns that is creative and unconventional.

Here is a quick definition of filtering from part 1 of my 4-part series “What is Filtering in P2P Lending?”:

Despite Lending Club and Prosper’s best efforts to make all loans within a grade the same, there remains a degree of variability in these loan assignments. Some B-grade loans perform better than average; some perform worse. This is when filtering comes into play. Filtering in peer to peer lending is choosing the loans that have historically performed better than others, even if they were the exact same loan grade.

Filtering is a kind of financial arbitrage. It means we exploit (for lack of a better word) the weak spots in Lending Club or Prosper’s loan grade assignments so as to achieve higher than average returns.

With each year that goes by, Prosper and Lending Club’s loan grades become more and more accurate. Eg: the 10+ filters I used in 2012 barely work anymore. Read more about the degradation of filters in my 2014 Filters post.

Even in 2015, a few powerful filters still exist. As I’ll demonstrate below, filtering continues to be an effective way to increase overall returns. Since 2011 I have earned over 9% on this investment (see my p2p portfolio), and I attribute filtering as a big reason for my higher than average returns.

My Investing Filters for Lending Club and Prosper

Having backtested many variables in the open data, here are my personal filters going into the remainder of the year. Note: I am an investor who takes on more risk because I’m younger and have that freedom. Most investors will probably want to focus on safer loan grades that perform better in national economic downturns.

My Lending Club Filter

Goal: 9% ROI

Grades: E, F, and G

See this filter on NSR

- Home: Mortgage, Own

- Inquiries: 0

- Income: $59,900 or more

- States: No AZ/CA/FL/NV

Here is this filter on the NSR Backtesting tool:

The filter has historically performed +4% better than the Lending Club average.

My Prosper Filter

Goal: 9.5% ROI

Grades: D, E, and HR

See this filter on NSR

- Home Ownership: Yes

- Inquiries: 0

Here is this filter on the NSR Backtesting tool:

This filter performs nicely as well, earning Prosper investors +4.7% above par.

How Have these Filters Performed in the Past?

A fair critique of filtering peer to peer loans has to do with the fact that they are somewhat simplistic and often fail to pass rigorous statistical muster. In response to this, I’ve broken down the performance of these filters over the past three years. Of course, past performance does not guarantee these filters will perform the same in the future, but the history does encourage me enough to keep using them through 2015.

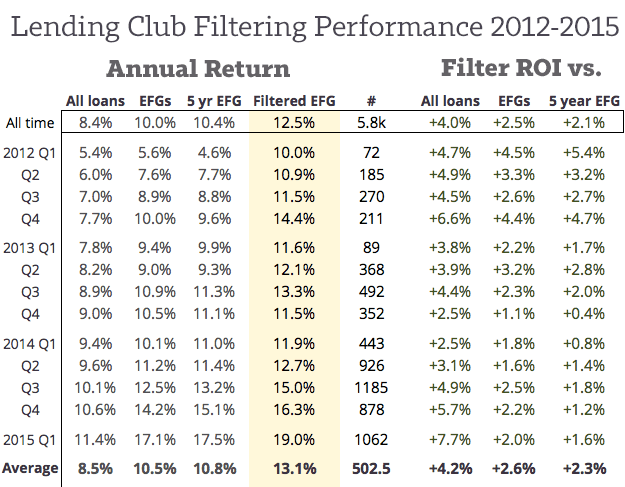

Lending Club filter: Performance over three years

Here is the Lending Club filter’s performance by quarter. I added a 5-year breakdown as well, considering almost 90% of the loans this filter returns are 5-year loans, and I wanted to make sure I was performing better than all of them.

Yes, this filter at Lending Club has been a consistent source of ROI for every quarter of the past 3 years. Typically, the filter performs +4% better than all of Lending Club’s loans, and even +2.3% better than similar rated EFG 5-year loans. Though just 73 of these loans were issued in Q1 of 2012, over a thousand are now being issued per quarter, so there is issuance to invest in if you want it.

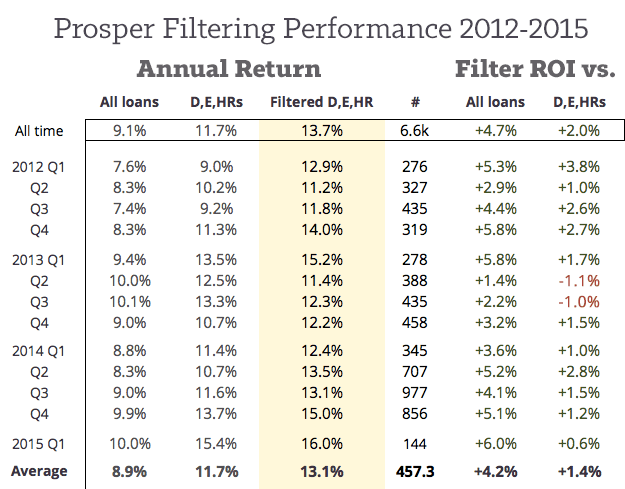

Prosper filter: Performance over three years

Here is a similar breakdown of the Prosper filter over the past 13 quarters. The 5-year breakdown is less necessary considering the filter has an similar average term to the total issuance (60/40 3yr/5yr).

This filter does not perform as strongly as my filter for Lending Club, meaning Prosper’s underwriting is perhaps more accurate overall. There are years (see D, E, HR in mid-2013) where the filter actually performs worse than average. However, the big picture continues to paint this filter as an effective way to boost ROI year-by-year, with the filter outperforming similar loans in the same grade by an average of +1.4%.

Which Filter Variables Make the Biggest Difference?

Things get really interesting if we highlight a recent vintage of these loans and look at which variable/criteria adds the most ROI.

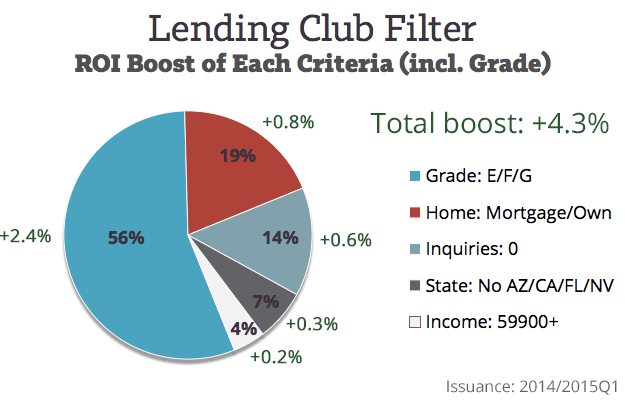

The most powerful variables for filtering Lending Club

The filter boosts returns at Lending Club by an overall +4.3% for 2014-2015. Here is where the majority of those gains come from:

The green percentages are how that variable boosted the overall return of the filter. Of course, just because Inquiries=0 gives a +0.6% boost to this filter for 2014/15 does not mean it will give the same bump to other grades, vintages, or future issued loans.

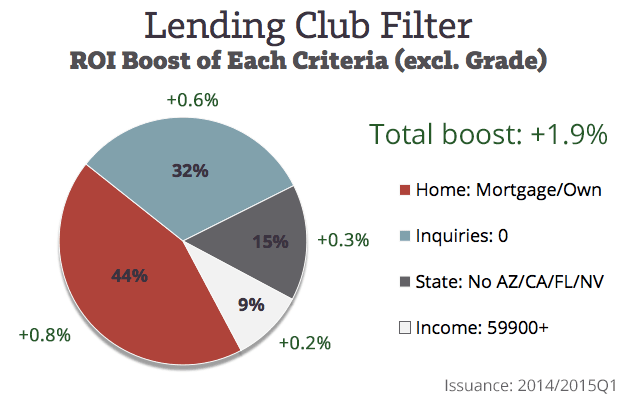

Looking at the pie chart, we can see that the biggest boost comes from simply investing in riskier loan grades. Indeed, investors looking to boost their returns often start by simply increasing the risk of their investment. But many would argue that this isn’t even filtering at all (and I would agree), so here’s the same chart excluding grades.

The most powerful filter in peer to peer lending is how a borrower self-reports their housing status. Fascinating! Inquiries=0 continues to play a powerful factor as well, with borrower state and income playing minor parts of their own.

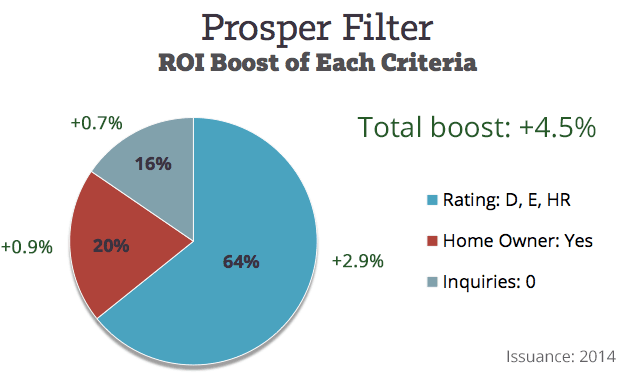

The most powerful variables for filtering Prosper

What about Prosper? Their breakdown is similar.

Again, the biggest gain comes through investing in riskier loan grades. But with grades removed, we can see how Prosper has a similar underwriting weakness for both inquiries and self-reported housing status, and our gains are evenly boosted by these two variables.

P2P Filtering: Boosting Returns Since 2006

In my How to Invest with a P2P Algorithm article, I stated my intention to move from filtering to full-on algorithm investing by the beginning of 2016. I still feel filtering is slowly dying off, so making that switch seems the right decision. That said, filtering still remains my favorite way to increase my overall return. I’ve even backtested these filters against a more rigorous statistical algorithm, and my personal filter actually performs better overall.

This is bound to change. Indeed, it is completely possible that Prosper or Lending Club will have fixed these weak spots by the middle of the year, and I’ll only realize it by the time I’ve already invested in a bunch of average performing loans, but that is a chance I’m willing to take. In my opinion, the worst that is likely to happen would be simply earning the platform average.

If you’re interested in learning how to filter, perhaps begin by reading my 4-part series starting with Part 1: What is a Peer to Peer Filter?. Secondly, you can see that tight filters often return very few loans, so if you have a hard time finding volume on Lending Club or Prosper, you may want to use an automated tool to invest. Here is a list of API tools, and here is an article describing how API tools work.

[image credit: Dietmar Down Under “Caught in a net” CC-BY 2.0]

Interesting that the criterion with the highest impact is self-reported (home ownership).

Assuming borrowers are reporting accurately implies homeowners are a better risk than the platform currently allows. However, it also make me wonder if there is an incentive for borrowers to lie about home ownership, e.g. more favorable rate, and what impact that misrepresentation would have on the returns over time (presumably negative).

Great point. I’m sure there are all sorts of ways borrowers could fudge their applications to get lower rates. If borrowers lie about their income, their documentation often shows them to be false. But giving a different home ownership status, for instance, is difficult to verify with documentation, at least with the current verification process that Prosper and Lending Club use today.

I’m not sure what type of credit analysis Lending Club or other companies do, but one easy way to find out if the person really owns a home is to see if there is any mortgage with balance in their Bureau. More than likely they don’t have their mortgage paid off.

Extremely thorough write-up. I’m also young and have a bit more risk tolerance than most. I actually have too temper my willingness to go for riskier investments.

What percentage of your portfolio are you willing to invest in higher risk loans before you feel it’s treading into unsafe territory?

Thanks Warren. My approach has always been to simply go for the highest ROI I can find. Since my time horizon is so long, I don’t consider the safety-factor at all. The only reason I lean into Es on Lending Club (and don’t go into just Fs or just Gs) is because FGs have not had a positive return for completed loans. See this: https://www.nsrplatform.com/permalink?l=44be64eb338c0a277fc33faa89844fc5

Really, I only include FGs to spice up the Es.

Understood, thanks.. It’s nice to see you have such success while taking on more risk. Your investing style is right up my alley. Thanks for the reference material, I will look into it.

What I dont see is why lend to complete strangers when you can lend to those you know then you can be sure their data is 80% accurate from the last time you met him/her. I am sure everyone would like to borrow from time to time and instead of borrowing from banks or strangers, borrow from friends. All you need is something to identify the borrower to you network say 4 degree criteria or use FB. Even when you have to shave off 2% to lend to a friend as compare to a stranger, that 2% may translate to happiness to those around you, priceless. And if you really think about it, there is no strangers because that stranger may be in his group of friends meaning to say, he might have save 2%.

The difference seems one of scale. It’s really hard to put $200,000 to work by investing it with friends.

Secondly, many people don’t like investing to friends or family because it means the relationship is at stake. If bad luck strikes (health issues, laid off, etc) you could actually lose a close friend, particularly if he or she determines your spending to be irresponsible. Many many friends and family have parted ways because of issuing credit to one another.

Simon, what about the fact that loans matching our most desired filters values are more often than not close to impossible to find. For example, I have yet to see a loan with 0 inquiries. Where do you find that?? For this reason, I am considering using LendingRobot or even attempting to write my own algorithm using the API. But my experience so far is that what’s left to the manual (i.e. browser) user to invest in is never even close to the most favorable values of the filters.

Another big issue is the high revolving percentage of notes that fail to issue. Has someone done an analysis by how much this alone affect the ROI?

Actually, I was incorrect. I do see loans with 0 inquiries, but they don’t tend to disappear when applying filters for time since last delinquency for example. Or what about income verification filter? I have given up on it.

So my overall sentiment is unchanged regarding the filtering and the high revolving unissued percentage – will appreciate any comments.

Agree totally on avoiding loans to friends. Your filter advice is helping me deliver 8.5% with my grade B loans. I’m very satisfied with that, looking at returns elsewhere. Keep up the great work.

This is a great article! I have been lurking in the background for some time now and just soaking it all in. I’m currently waiting for my first “big” chunk of money to go into LC. I have been playing with NSR and reading up on filters and I have also got a LR account setup. It’s fairly easy to get the filters for a higher ROI but my question is, do you use multiple filters each time you invest? I have setup a filter like yours but I also have a more strict filter that yields a very high ROI but very few loans. When I go to invest this first chunk of money should I enable that strict filter and let it go for a week or so before I enable the other filter? I have some other filters too that are in-between your filter and my very strict filter, should I enable those at a week or so intervals to try and get the best possible loans or should I just enable the filter like yours and let it get all my money in the pot right off the bat? Again, great website altogether! I have really enjoyed reading all your material.

Very nice website of yours, I will be starting to lend money next week, I did my very first deposit today with LC.

I have a question that 13% gain is annually or monthly? I know it might sound like a dumb question but I will try to invest onthe A loans so I can get a better return that just having a savings account in a bank they less that 1% return.

Can you let me know what was the basis for excluding few states (AZ, CA. FL, NV) in your lending club filter.

Hey S,

I am pretty sure no CA/FL/NV/AZ is based on this article:

/redlining-florida-lending-club-prosper/

Good luck!

Hi Simon,

It\’s been almost a year. How\’s your lending club filtering strategy working out for you? Still have the same filter criteria? I am just starting out with Lending Club so I value experienced investors\’ opinion such as yours.

Thanks

Ivan

I have less time for the site these days, but overall my filtering strategy has stayed the same. I removed the ‘own’ option for housing. So now it’s all mortgages.

Appreciate the response, Simon. I have my account funded and am ready to start investing. Thanks again for sharing your strategy :)

Indeed, I also would like to know. I have an IRA with Lending Club that’s been returning around 9% adjusted, which I consider decent, but it’s still early.

I am considering putting more in the IRA – like a lot more. What do you think will happen with returns if we have a recession?

Also, what will happen with any IRA’s if – shudder to think about it – Lending Club goes bust? I don’t wish it upon LC, quite the contrary, I am a believer in the company, but Wall Street pressure on it is very strong and that, coupled with a recession, may prove to be too much? Would love to know your opinion.

In a recession, I believe we’ll be fine: /p2p-lending-recession-performance/

As for a Lending Club bankruptcy, which is unlikely, the situation is still quite doable. Lending Club has backup servicers in place to make sure borrowers still make their payments to you. Remember, they earn a fee of 1% on all borrower repayments, so there’s an incentive to repay these for whoever company takes over the assets of a bankrupted Lending Club.

The biggest thing to watch closely is the default rates of these loans. They are indicative of the underwriting standards. As long as these remain robust, investors like ourselves will be ok.

Its my view that when recession comes, everyone will be in the same boat as they cant pay and even those who can pay will avoid paying. That’s my experience, so no matter how LC protects itself, it will face three issues. No lenders, no borrowers and existing borrowers who cant pay or avoiding payments. Thats why banks go belly up and LC is not much different to a bank save for overheads and focus into one type of business (ie taking away the riskier or less profitable business from the banks).

If you think a recession affects everybody the same, you need to take a closer look at the historical data across the credit industry. While the 2008 recession deeply impacted almost everybody in some way, prime-rated personal credit (in credit cards) never experienced a negative return. Does p2p lending possess this same resiliency? Who knows. But the data is promising.

Hi Simon,

I have started with Lending Club. I want to use their Automated Investing as my investment amount is pretty large.

If I go with their Custom Mixing and apply the filter you mentioned in your article above, will it work?

When I apply that filter, I see they list a target ROI in the mid 10\’s (30% in E, 40% in F, and 30% in G). Is that realistic or very hypothetical? I mean they\’ve gathered sooooo much data from past loans one would assume their prediction model would be pretty close if not spot-on.

Thanks

Ivan

In investing, there is not really such a thing as being able to predict future returns. Yes, the number is historically accurate, but the future is always different than the past.

Do you think the amount of the loan should play a part in the filtering process?

Generally, no. Though I could be wrong. The data never lies, so check for yourself :)

Hi Simon

Is filtering an option within automated investing at Lending Club (if so please explain how) or does it have to be done manually loan by loan?

Thanks Dan

You can add a filter within their Automated Investing tool.

Thanks for valuable information. Does your ROI data include losses due to past-due and charge off’s ?

Hi Simon,

Fantastic article,

I may have missed it in your previous discussion, but which time frame do you recommend the 36 or 60 month?

Thank you,

John