Late into 2013, peer to peer lending continues to be a novel avenue to earn a decent return on investment. However, despite coverage in major news publications, despite rigorous technical analysis and years of historical data, there remain many unanswered questions. For instance, how large can this industry grow (some say $200B in loans)? Can further filtering of the available loans actually improve returns beyond the rigorous underwriting done by a platform? Finally, what return does peer to peer lending even offer?

It is this last question that we will devote the focus of our article today, hoping to get an answer by turning to leading voices within the industry. Interestingly, their answers widely vary. Some think a 5% return can be expected; others say 12%. The overall consensus certainly trumpets the lucrative returns available within peer to peer lending, but when pushed for actual numbers, this consensus breaks down. It’s like asking five dietitians what makes a healthy eating habit. All would respond a with some version of a balanced diet. But when pressed, their answers would divert into different emphases. Some would be about protein; others, green leafy vegetables.

From Diversity to Consensus: 5 to 12% ROI

There is a similar diversity of opinion within peer to peer lending. Why is this? For starters, it is difficult to calculate its return at all. The “annualized return” figures stated on the Lending Club and Prosper account screens do not take into account the drag of uninvested cash, and become even more inaccurate if any trading is done on the Foliofn secondary market. Calculating ROI using an internal rate of return (IE: XIRR) is arguably the best approach, but not everybody has taken on this practice.

There is a similar diversity of opinion within peer to peer lending. Why is this? For starters, it is difficult to calculate its return at all. The “annualized return” figures stated on the Lending Club and Prosper account screens do not take into account the drag of uninvested cash, and become even more inaccurate if any trading is done on the Foliofn secondary market. Calculating ROI using an internal rate of return (IE: XIRR) is arguably the best approach, but not everybody has taken on this practice.

Furthermore, what defines an average or typical investment? There are a wide variety of approaches that different investors take. Passive, middle-of-the-road lenders who simply invest in the notes available to them (IE: A – C grade) will often earn a significantly lower return than those who are well versed with the system, who auto-invest their backtested filters via an API into riskier higher interest notes (D & E grade).

That said, I feel we can still arrive at a majority opinion through a review of the industry voices quoted below. Doing so may allow us to answer the elusive question: what sort of return is possible within peer to peer lending? Humbly, I would like to offer their consensus: peer to peer lending offers a 5-12% return for the average retail investor, depending on their level of activity, skill, and risk tolerance.

One Question, Five Valuable Answers

Five different experts were asked to answer this question: what kind of sustainable return can a lender realistically expect through peer to peer lending? Here are their answers:

Peter Renton, Lend Academy: 6-10%

“I think astute investors will receive returns in the 8-10% range, with an average return of 6-7%. We know today that many investors are earning more than that, but I think as the industry matures returns will come down. That said, I expect 8-10% returns will be achievable for many investors through the end of this decade.”

Peter is the founder of Lend Academy. As a self-described passive p2p investor who has rigorously studied where the industry is headed, I can see his low end of 6% as indicative of what many new investors may experience today.

Marc Prosser, Learn Bonds: 8-12%

“My personal rate of return is currently 15%. However, my expectation is that my portfolio over the next 6 months will go down to about 12%. If the economy goes south and in particular the unemployment situation gets worse, I think that my returns will be in the 8% range.”

Marc writes for Forbes and has been a voice within the p2p lending sphere for some time. His numbers shows what sort of lucrative returns are possible for investors who focus on low-grade loans.

Bryce Mason, P2P Picks: 5-13%

“The rates are reflective of my experiences as an investor, personally and as a consultant to investment management companies building p2p portfolios. For a ‘Buy & Hold – High Yield’ approach: a 9-13% ROI is possible. I take a buy and hold approach exclusively at Lending Club, and have achieved fairly stable annualized returns of around 12%. In general this approach targets C-G graded loans. Individual investors will vary in their loan selection sophistication. For a ‘Buy and Hold – Low Risk’ approach: a 5-7% ROI is possible. This approach would target A-B graded loans, although loan selection again can play a role in determining the yield and consistency.

Bryce is the statistician behind P2P-Picks, and his answer contained the largest swing (which I feel makes it the most accurate). His answer also emphasizes the impact that good loan selection can have on returns – meaning, for example, that some B-grade loans perform better than others.

Brendan Ross, Ross Asset Advisors: 9-11%

“Most my P2P lending is done through funds run by professional managers; returns vary based on alpha (how good the manager is at picking loans) and beta (their chosen mix of loan grades). No fund is going to be as aggressive as the most risk-loving individual investor, which I think is a good thing. In consumer P2P lending, funds I respect range from 9-11% returns.”

Brendan of Direct Lending Investments is a known voice within the wealth management side of p2p; he was the first advisor to invest in Lending Club’s LCAdvisors fund. His answer is tilted toward large value clients, demonstrating that a high return is wonderfully scalable. Even investors with millions of dollars available to them may find a return north of 7%.

Anil Gupta, PeerCube: 6-8%

“Lenders can expect average return of about 6-8% for mature portfolios as long as economic conditions do not deteriorate and there is no major structural change in the platforms. I expect that over time, as the platform matures and becomes more efficient, the average returns will fall.

Anil is the investor and programmer behind PeerCube. As someone who has typically viewed high returns with skepticism, Anil’s ROI is probably the soberest of the bunch, and with good reason. Anil’s grasp of the hard data has convinced him that many investors (myself probably included) overstate the sustainable ROI offered by peer to peer lending.

How to Arrive at a 5-12% ROI

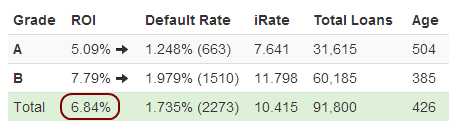

For starters, think about the lowest risk you can possibly take on within a diversified portfolio: 200 A-grade notes. Considering the historical return on A-grades at Lending Club is 5%, I would imagine this would go lower as an individual account starts to age, perhaps landing at 4%. However, most investors diversify in the variety of loan grades offered to them, easily adding a percentage point or two. Simply stated, for the average investor who diversifies in the notes available to them (for Lending Club this is A – C grade notes), the basic platform underwriting offers them around a 5% ROI (hat tip to NSR).

From this starting point, the return for the savvy investor may rise to 12% based on their investment approach and risk tolerance. There are many different ways investors try to increase their ROI (see Lending Club Strategy and Prosper Strategy), but all of these generally focus on either becoming more active as an investor (IE: developing a selection criteria/filters) or taking on more risk (IE: focusing on low-grade loans).

Conclusion: A Stable Lucrative Return of 5%

Across the board, experts agree that a wonderful real-world return of 5% or more can be achieved through a simple diversified peer to peer lending portfolio. Five percent! In my view, there exists no other large-scale avenue of investing that offers such a great return with so little volatility and such high liquidity, especially when we consider how interest rates continue to stay so low.

Investors may differ on how high up we can push the ceiling, but we generally can agree on the floor. This is an appropriate note to close on: the peer to peer lending sphere can often get so caught up in chasing returns above 10% that we forget how rare it is these days to earn a 5% return in the first place.

[image credit: raphaelstrada “Falling down from stage“/Marcin Wichary “Calculator keyboard close-up” CC-BY 2.0]

If I invest 10k how long would it take to get that money back with interest (days – Years)?

If you invest in 3 year loans, it will take 3 years before the loans are paid back. 5 year loans are a 5 year investment. Etc. Of course, you can always liquidate your account on the secondary market. See here: /liquidate-close-lending-club-prosper/

What are the tax implications upon liquidation? Capital gains, income tax etc

You’ll pay on any interest that you earned over the year, and any notes that are sold in liquidation (within a taxable account, of course) will require capital gains tax to be paid, either short term or long term, with of course the ability to claim capital losses as well.