Two weeks ago I had the privilege of going to San Francisco to talk with Prosper and Lending Club about their past year, the future of peer to peer lending as an industry, and how LendingMemo might be able to help.

My first meeting was with Aaron Vermut, President of Prosper Marketplace. In our previous interview (See: Vermut Discusses $125M Google Investment), we met in a conference room at Prosper’s old location. This time however, I met him at their new office location, a big improvement as it seemed larger, brighter lit, and more modern. I was eager to talk with Aaron about the recent changes at Prosper, particularly the remarkable turnaround they have experienced in the past year.

Aaron and I took the elevator down to a nearby Peet’s Coffee, and I was able to ask him a few questions.

Interview with Prosper’s President

What are the latest changes that have happened at your company?

What are the latest changes that have happened at your company?

There is a really good story here regarding Prosper’s turnaround. We have made many changes in the company. One of the things we found when we got here was that the activation rate of our funnel, the percentage of borrowers who go on to complete a loan application, was way lower than it should have been. This resulted in higher than optimal borrower acquisition costs that needed to be remedied immediately.

So we locked the doors and embarked upon the borrower funnel project. We went through and mapped out our whole user experience, all the web pages and paths involved with getting a loan. And what we found was that the process was much more complex than needed and really did not reflect best practices. And back then, Scorex was our credit bureau.

Why did the previous team choose to use Experian Scorex? To artificially inflate their average borrower’s credit score?

No. I think it was because Scorex is good and reliable for lower FICO applicants. But we found that, for our prime and super prime borrowers, FICO would give us a much more accurate picture of their ability to repay.

Upon completion of the borrower funnel project in September, we got the whole web funnel down to four pages and switched to FICO, which is the gold standard for prime borrowers.

The application used to be more than four pages?

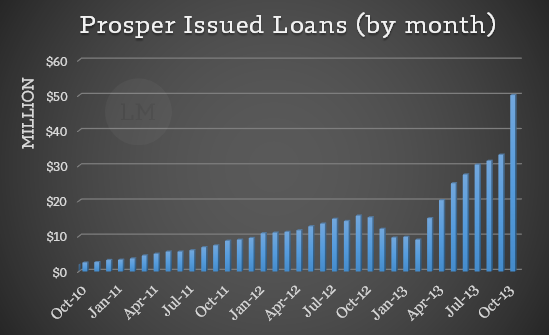

I wish I had a picture to show you how convoluted it was, especially if you deviated from the ‘happy path’. The application process was developed organically over the years by the previous team and really did not reflect best practices. We fixed that. We released FICO and the new borrower funnel in September, and you can see the effect. In the first half of September we issued $10 million in loans. For the second half we issued $22 million without a step-up in marketing spend.

Additionally, we improved much of our internal infrastructure. We replaced the equipment in our data center and opened up a disaster recovery center in Portland. If you think about a seven year old company, a lot of our equipment was past end-of-lifetime. I personally spent the summer renegotiating with all of our vendors, since one of the things we found when we got here was that the company was overpaying many vendors and service providers.

How would you see a Lending Club IPO affecting you guys?

I don’t understand the valuation, but I’m happy they are well regarded in the industry. As a former venture investor, I can say that every once in a while a company comes along that the market decides is special and can’t do anything wrong. Lending Club got that. Right now they can do no wrong, and I hope they do not lose that.

What has been your favorite part about your job?

One of the things I enjoy is that this business is far more complicated than it seems from the outside. From the outside people think we just throw loans up on the website and people buy them, but on the inside there are credit models, pricing, complexity, bidding, APIs, and strategy. I enjoy the intellectual challenge and trying to reorient this company.

One of the other things I really like about Prosper is that it is a white-hat organization. You get to be a good guy. You are providing loans at a lower rate to people who are primarily debt consolidators. We have no hidden fees and no gotchas. Because of the way the SEC has structured this thing, we are a public company. There are no secrets. Everything we do is out on the table, and this is really refreshing after being in the brokerage world. I get to solve hard problems and be really honest about it. It’s cool.

Just how big is peer to peer lending?

Lending Club and Prosper have loaned, what, $3 billion now? I think, on an annualized basis, if it’s 10% of credit cards – that is $60 billion. If it’s 1% its $6 billion. I think $20-$30 billion in issued loans per year is doable. The question is, is it a zero sum game? I’m not really the expert on this, but the question is if we are creating something new. When we make a loan, is that a loan someone else won’t make? I don’t know the answer to that question. Only 63% of our loans are debt consolidation, so I am not convinced it is a zero sum game.

Some worry that the platforms will eventually sell off their retail and become only institutional.

From my perspective, that is not going to happen. Lending Club would never do it either. A big part of their valuation is based on their being a peer to peer platform. If you get rid of that, you are just specialty finance. You are just a loan originator. We think individual retail investing is good for the brand, attracts borrowers, and actually affects the payback rate. If borrowers remember that these are people who funded them, they are more likely to pay their loan back.

How is the individual retail investor’s experience going to change in the coming year?

It will be better. We’re going to have more loans for you to choose from.

Every day we allocate between the fractional (retail) and whole loan (institutional) pools based on where we see demand. Whenever we have loan listings in the inventory we want to put them in the place that is most likely to get funding. And we make sure the loans that go to one or the other are randomly distributed so there’s no adverse selection.

A lot of individual investors get frustrated because they don’t have access to API. I invest with an API, so I have access to your D, E, and HR-grade loans, and I’m making a killing from them with a 13.8% return…

That can’t be seasoned.

It is.

That’s better than me. My investments are at 12.94% or something like that and they aren’t seasoned.

I can teach you. You should go to LendingMemo.com.

(laughter) I buy my notes manually, without an API. It’s really sad.

Do you think average retail investors are ever going to get access to D, E, & HR grade loans? Because, let’s be honest, they don’t even have access right now.

They get bought too fast?

Seconds.

Like I always tell people, the best way we can solve this issue is to get out there and bring on more inventory. Pause for a moment and look at Lending Club. Their whole inventory is like our AA, A, & B grade loans. They do not even have loans that look like our C-HR grades. The thing about Cs through HRs is that they are harder to originate, they are expensive, and there are fewer of them because borrowers like the low rates they get on A-grade loans versus Cs-HRs. Plus, we actually do not make much money on them.

Because their acquisition cost is so high?

It is because they are small. We make a smaller fee from them, yet we have to spend the same marketing dollar to get them.

And you guys probably aren’t going to issue $35,000 HR-grade loans.

Heck no. It does not work. When we go out and market, we get this distribution of loans, and it always tails off towards the HR.

Maybe what the retail community needs to do is see investing in C grade loans as a privilege.

What you should do is buy the platform average, goosed up with whatever Cs through HRs you can get. Everybody wants them and we are generating as many as we can. It is not like they are getting siphoned off to the institutional guys. They are just going quickly.

Any thoughts on Lending Club’s entry into small business loans?

I don’t actually agree with the strategy. I think it’s a fundamental departure from the core strength, which is unsecured consumer credit. We haven’t really explored our next thing at Prosper. We’re trying to get this one right.

If an individual investor with $12,000 came to you and asked, “Why should I choose Prosper?”, what would you say to them?

We have the broadest selection of loans.

Good point. I forget that.

Right. We have the widest selection of interest rates, and investors can set up our Automated Quick Invest (AQI) tool to automatically buy notes whenever new loans are added to the platform.

Lending Club told me they would release their automated investment tool back in April, but it still has not arrived.

I don’t know much about that but I can tell you at Prosper, we are really focused on customer service and providing useful tools to all of our lenders. We are constantly working on getting better at what we do. We get our statements out on the second business day every month. We have AQI, Prosper Premier, and our API is the industry gold standard. Overall, we are seeking to be the best run, the most customer focused, and the most respected brand in peer to peer lending.

Simon, phenomenal interview with Aaron. Love the, “That can’t be seasoned” response.

On a serious note, what Aaron is saying fully matches what we have been seeing from Prosper for months. I believe they have a much stronger focus on process development and customer support across the board than does Lending Club, as evidenced by the lack of automated investment option at Lending Club. And this plays right into Lending Club pursuing the small business loans. I think that segment is absolutely one to be pursued, however, it shouldn’t be at the expense of upgrading and improving the shortcomings with the main platform.

Great interview Simon. My favorite part was his response to the retail investor question: If you get rid of that, you are just specialty finance. You are just a loan originator. The real value proposition for both LC and Prosper is that individual investors can access this asset class. This is why both companies continue to work hard to please retail investors.

Great interview as always. Very insightful!

Great work, Simon.

Great interview. I always preferred Prosper to Lending Club.