I remember what it’s like to discover peer to peer lending. This thing is realized to be new and promising, and suddenly you cannot wait to get started. But then reality sets in: there are not enough available loans. How frustrating! You did all the right work of opening a Lending Club or Prosper account, funding it with some trial money. However, when you log into the platform, you discover that few loans are available for investment.

What options do you have? In today’s post, we will examine seven strategies you can use to find more loans when few seem to exist.

2013: The Year P2P Lending Became Cool

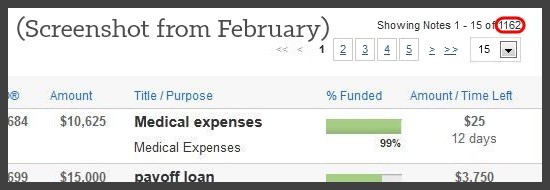

Back in the early days of peer to peer lending (like, February) investors could choose from a thousand available loans on Lending Club’s website. For years the main funding for loans came from retail investors, basically people around the country who were investing their own individual cash. These lenders were sometimes unwilling to fund riskier borrowers because they had better options available. As a result, some loans took a week or more to find enough willing investors, and some loans would even fail to get funded at all. See the screenshot below from February 6, 2013: 1162 loans were available on the platform.

Now everything has changed. Lending Club and Prosper continue to rise in popularity, earning outside investments (from Google) and positive coverage in the press (see Prosper on Fox Business). Since September 2011, every Lending Club loan has been fully funded, and most get funded within 24 hours. To boot, the Lending Club and Prosper loans that earn the best interest (the riskier low-grade loans) are often snapped up in minutes. This change is the result of peer to peer lending’s flood of institutional investors (hedge funds, money managers, etc). Years of positive returns coupled with recent positive press have given these well-funded institutions the confidence they needed to get involved.

Three ways big-dollar institutional investors make it harder for the rest of us:

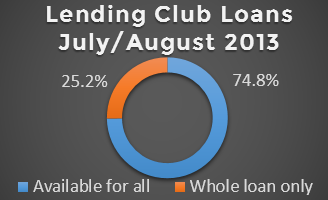

- Institutions fund 25% of Lending Club’s loans through the Whole Loan program before they are made available to retail investors like you and me.

We never even see these loans.

We never even see these loans. - The remaining 75% of Lending Club’s loans that are added to our Browse Notes screen are being snapped up via API by institutions. Prosper does this too. Basically this means that institutions are automatically placing orders through high speed server requests the moment these loans become available.

- Despite a funding limit of 50-75% per loan (IE: an institution could fund $7,500 of a $10,000 loan), these institutional investors have millions of dollars available to them, far more than the average retail investor. This means institutions purchase notes as large as $26,000, leaving a much smaller percentage of each loan available for lenders like us.

Fewer Available Loans for Retail Investors

Where does this leave the average investor like you and me? As seen in the chart below, the number of available loans changes throughout the day. The average investor, casually logging into the Lending Club website, will typically find between 50 and 100 loans to choose from:

Within 50-100 loans, perhaps just a handful are the higher interest D-G grade loans (currently just 2 loans out of 79!). How should the average investor adjust to this problem?

Seven Solid Ways We Can Find More Loans

Here are seven different ways we can find more loans, ordered by how much time they take.

#1. Invest in Whatever Loans are Available

Even though the “best” loans are snapped up by institutions using an API, the remaining loans can still be decent investments. We need to remember that Lending Club and Prosper give underwriting approval to every single loan on the platform. We can trust the underwriting and invest in whatever loans are available. This may result in earning a lower return than more active investors, but if we remain diversified it is still possible to earn a great return.

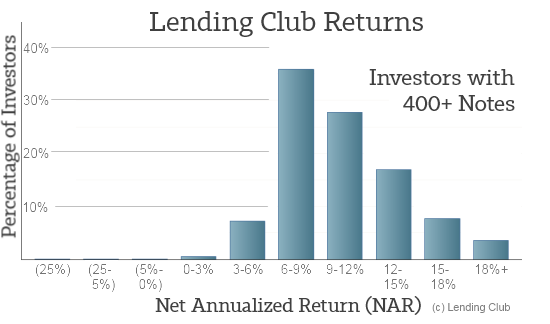

As seen in Lending Club’s chart above, the vast majority of investors who have a diversified account of at least 400 notes earn a positive return, and this includes investors who simply go with whatever loans are available. Even if you only invest in 100 notes, diversification makes a huge difference.

#2. Log in at 6am, 10am, 2pm, and 6pm PST

As seen in the graphic above about Lending Club’s loan availability, new loans are added daily at 6am, 10am, 2pm, and 6pm PST. In contrast, Prosper adds loans at 9am and 5pm (noon on weekends). For investors who log in during these times, there are far more available loans to choose, including many D-G grade loans. This can be a bit of work for people, as it means they have to set an alarm or keep their eye on the clock, but it can be rewarding for those who figure out a system to do it.

#3. Simplify your Filters

When I first started investing in peer to peer loans, I would often use filters with (too?) many qualifiers. For example, here is a filter I might have used in 2012:

- $2000-$35,000 Loans

- E-G Grade

- Purpose: Only Debt Consolidation/Credit Cards

- $60,000 income/year

- 10+ Years of Employment

- Max 20% Debt-to-Income Ratio

- 5+ Open Credit Lines

- 10+ Total Credit Lines

- No Inquiries

- No Public Records

- Max 95% Credit Utilization

- Exclude CA & FL

A filter like this had twelve attributes, meaning it cut down the available loan pool in twelve different ways. Oh, how times have changed. If I would try to use this same filter today, I would maybe find a single loan per month.

To adjust, we can simplify the filters we use. We can choose to compromise. This may mean earning a lower return, but some simple filtering can still give us a chance to beat the average. For instance, we could filter the 79 currently available notes with a simple filter like this:

- C-G Grade Loans

- No Business Loans

- $4000/month income

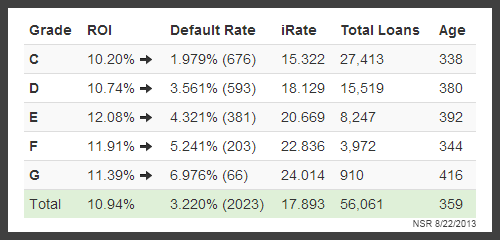

This simple 3-attribute filter would give me five solid notes out of the 79 available loans, and definitely many more if I logged in at 10am. Historically, it performs at almost 11% on the NickelSteamroller Return Forecaster tool:

Disclaimer: we need to remember that these filtering tools are notorious for being unpredictable. Not only are they pulling this data from loans that are still being repaid (many will default), but Lending Club’s underwriting has almost certainly changed since this data starts in 2009. That said, this tool is a decent place to begin.

#4. Use Multiple Filters to Find More Loans

If you typically have invested with just a single filter, you should try to expand into others. One way to do this is to take whatever filter you currently use and split it into two performing filters. This is a bit more complicated, and it is outlined fully in the fourth part of my series on filtering: Filtering with Prosper.

Multiple filters are necessary for any serious investor. In short, remember that whenever we use a filter to isolate better loans, we are almost certainly removing some good with the bad. To combat this, we can use multiple filters to pull apart the available loan pool in different ways, helping us to find more loans than if we just used a single filter on its own.

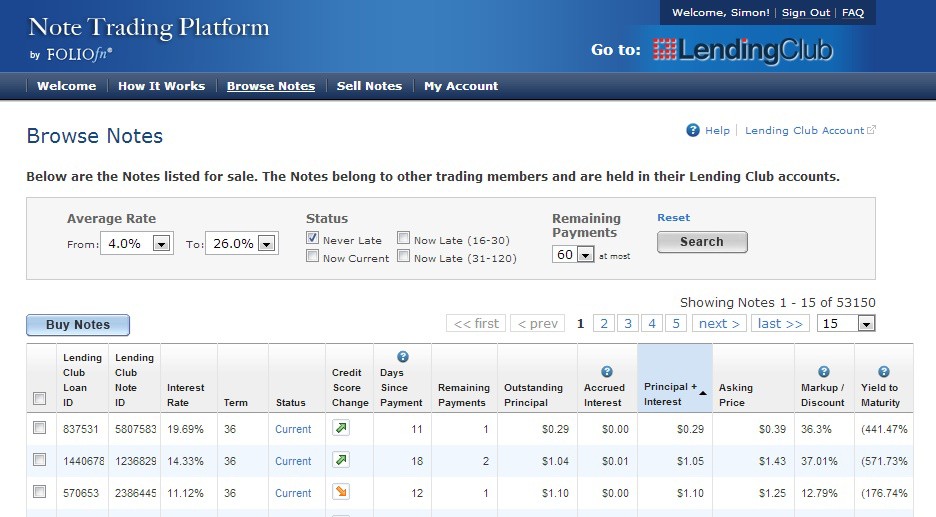

#5. Buy Notes on the Foliofn Secondary Market

NewJerseyGuy gave a really great suggestion in the comments section after this post was published: Foliofn. For those brand new to Lending Club, a secondary market exists where people are buying and selling their notes to each other. The graphic below shows how there are 53,000 notes available today for purchase on Foliofn. Now that’s some availability.

You can access the secondary market through Lending Club’s Trading Account link. Many lenders have had success this way, but many have also been frustrated by it. In short, the Foliofn interface is really rough at both Lending Club and Prosper. It might be good enough for some, but many serious Foliofn investors have found success by using Interest Radar instead, a site that can deeply filter the secondary market for solid deals on notes.

#6. Open an Account on a Different Platform

Many people wonder why I have accounts at both Lending Club and Prosper, considering they offer a similar service. Well, now one of the benefits is clearly seen: access to additional loans. Have you been having a tough time finding loans on Lending Club? Open an account at Prosper. Loans scarce at Prosper? Open an account at Lending Club.

Not only do you suddenly get access to another entire population of borrowers, but you also further diversify your peer to peer lending investment (read: Diversify Your Account Like a Pro). Additionally, I feel the lessons I have learned on one platform have helped with my lending process on the other. In summary, the benefits are tremendous.

#7. Automate Investing with Third-Party Tools

There are a number of different ways we can automate our investing at Lending Club and Prosper. Interest Radar, NSRInvest, and Lending Robot are options for investors that allow automatic investing. I shy away from these sites because they do not stick to the Lending Club API; they also scrape Lending Club’s PHP, and this is a bit insecure for me (especially any auto-sell feature). But many within the Interest Radar community continue to use it and celebrate its returns.

There are a number of different ways we can automate our investing at Lending Club and Prosper. Interest Radar, NSRInvest, and Lending Robot are options for investors that allow automatic investing. I shy away from these sites because they do not stick to the Lending Club API; they also scrape Lending Club’s PHP, and this is a bit insecure for me (especially any auto-sell feature). But many within the Interest Radar community continue to use it and celebrate its returns.

Finally, for those skilled with API code, you can request access from Lending Club and automate your own system (example | example).

I use an automated API myself, and the benefits are great. Instead of watching the clock or setting an alarm for 10am/2pm/6pm (I sleep past 6am), the system runs my filters and automatically invests for me.

Lending Club’s Scott Sanborn indicated to me in May (read the interview) that Lending Club hopes to have an in-house automated investment option soon, but he said it would be finished in the summer. Now that the summer is almost over, so I am curious how much longer it will take. Even if Lending Club’s automated investing option launches, I am doubtful if it will be able to compete with the institutions. Fast servers using an API seem like they will continue to have an edge for the foreseeable future. For instance, Prosper has had a good automated investing option (called Automated Quick Invest) for almost two years, but this tool is slow in comparison to a quick API. My own Automated Quick Invest setup with Prosper was losing out to institutions until I got in the API game myself.

Investing Large Amounts vs. Reinvesting Returns

These seven strategies are going to depend on how many loans you need to find. For instance, if you are investing a big sum of money at once, like opening an IRA with $5000, you may need to work harder in order to get it all invested in 200 notes, or at least until the initial chunk is in. Otherwise, that cash is sitting idle in your account earning no interest.

In contrast, you may be able to work a bit less if you are simply reinvesting your returns. If you simply need to find a loan or two to invest in per week, then your needs will be less.

Fewer Available Loans is the New Normal (and that’s OK)

In my opinion, this scarcity is here to stay. Institutional investors will continue to get privileged access to loans, if not from the platforms themselves then through having faster servers. It seems like retail investors like us will have to continue to struggle for access to the best loans.

That said, peer to peer lending continues to give us a healthy 6-8% return if we simply go with the flow and invest in whatever loans are available (see point #1 above). Additionally, it is still very possible to beat this average by doing just a little extra work. Institutional investors will continue to be a big factor in peer to peer lending, but just a little effort can allow us to go toe-to-toe against these big guys.

Questions or comments? If you enjoyed this please Like or Tweet it below.

[image credit: Andrew Malone “Metal Detector” CC-BY 2.0]

Thanks for another excellent and very useful post. My only point of disagreement is with the conclusion that ¨scarcity is here to stay¨. Where there is a functioning market, excess demand (for new loans) will be met with new supply sooner or later. Considering that the loan volumes of Lending Club and Prosper together are just a drop in the ocean compared to the total potential market for just credit card consolidation, (not to mention student loans, small business lending or automobile finance) there are reasons to believe that this supply will come forward as more people learn about the advantages of P2P lending, both from the investor side as well as from the borrower side.

James Levy, Madrid, Spain

Hi James. Thanks for your comment. I agree that there is plenty of room for an increase in supply, but I don’t foresee a rush of new borrowers suddenly allowing the casual retail investor, logging in at 3pm some afternoon, access to a large number of filtered D-G grade loans. I could be wrong, but it seems like the best loans will always be snapped up by those with the ability to do so.

Who did you get to program your API?

Hi JJ. I have beta access to NickelSteamroller’s upcoming tool.

This can be quite frustrating. At first even a few days ago I didn’t have such experience, so I didn’t pay attention to this lack of notes much (I was kinda telling myself, “Guys, what are you talking about.” but just yesterday and the day before when I finally could log in to the account there were only close to 10 available notes to invest. Other than that the platform on LC was empty. I couldn’t believe my eyes. It needed some effort and multiple logins to find anything to invest in. I now will have to log in in those times. Thanks for listing them, because I was looking for it the other day desperately looking for my money placement.

Simon…..Always love reading your stuff!

If you’ve been reading my stuff on Lendacademy over the past year, then you know none of this means a darn thing to me. I’m in a Folio-Only state, as are many of the other readers. Obviously, I’ve been touting the advantages of using Folio as a secondary source of both additional notes and alternative investing strategies.

Both LC and Prosper investors are still wearing blinders thinking those two platforms are the only place to get good notes. I’m surprised that you didn’t mention Folio as a “Sixth” source of obtaining freshly-issued notes. I have no choice but to get them there, yet I’m creating a quality portfolio of mainly C-D-E notes yielding me 15.9%

Lots of great notes available even when using many qualifiers in your filters. Go get some.

Hi NJG,

Folio availability is a killer suggestion for a sixth option. :) Question: how do you filter on Folio? For me, the interface has been so rough that I barely know where to begin.

Simon….I hope you’re not talking about about that interface on Folio, are you? If so, you’d be better off just shooting yourself in the foot and getting it over with now. Folio bought that cheap from a local 2nd Grade computer class. (2 balloons and a stale bag of candy).

The superb filtering on Interest Radar is designed for BOTH the Lending Club Platform OR Folio. You can run filters for LC one moment, click a box, and you’re running the exact, same filters on Folio the next moment. That’s right, the exact, same filters.

Interest Radar is the only platform that I am aware of where Folio isn’t some little afterthought. It’s packed with a ton of features. It’s a “Must Have” for us people in Folio-Only states. However, if you’re already a subscriber and don’t know about it, then it’s worth looking into.

What a great explanation of Interest Radar. Thanks for this. I am sure people who are frustrated with the state of things will be eager to explore this versatile tool.

Simon,

Thanks for PeerCube mention. Just a clarification: PeerCube doesn’t offer automated investing. We have several security and legal concerns about offering automated investing. We decided to defer automated investing features until:

1. We are convinced we can properly secure Lending Club and Prosper account information of our users,

2. Such a service will meet SEC and government regulations regarding third-party trading/investment management vis-vis managed accounts and trading authorization,

3. Any system error can be addressed to the satisfaction of our users without threatening the existence of the platform.

Instead of making a quick buck or taking advantage of arbitrage opportunity, we decided that it is better for the long term viability of PeerCube to be conservative in offering any features that may run afoul of regulations or compromise user information.

Thanks.

Anil

Thanks Anil. I stand corrected. Peercube *does have API, but only to pull the current loan listing. At the moment, it seems Interest Radar and BlueVestment are the only third-party sites open to the public, and both are not as secure as I wish they were.

Hi,

This is a great article but I’d like to point out that BlueVestment does indeed use the Lending Club API when available. The API is very much lacking features and the BlueVestment service only screen scrapes (securely using HTTPS) when the LC API comes up short.

Thanks for the clarification Nathan. I updated the article to reflect your statement.

Hi Simon,

Great article. I’m just starting out and was wondering what your experience was with 60 month F,G loans on LC? Other articles have said to stay away from 60 month loans, and if so that means I can only find D & E loans with 36 month loans.

I love my 60month Fs and the ever-rare Gs. I think the risk is great for my personal comfort, and the returns are often outstanding.

As always, another great P2P lending resource.

Thanks for the tip on the API. Being a computer programmer by training, if not by trade, it’s good to know I won’t have to wake up at 6am to find the best loans, but can access them programmatically when I’m ready to start investing.

I’ve been investing in Lending Club since February of 2009…the decline of true “peer to peer” lending has made me seriously consider giving up on this investment tool all together. I’m not going to wake up at 6am everyday, and all of the good ones are usually taken by 10am. Have almost 1K in my acct now and can’t find a note above “B” to invest in! Do you think the “peer” in “peer to peer” lending is dying?

Hi A. Good question! The short answer is, you’re going to have to adjust to this new reality if you want to stay in the game. If you automate your investing (or log in at the appropriate times) there are plenty of C, D, E, & F loans to be had. However, if you want the good ol’ days back, sorry.

I agree with Simon. I was able to finally make it work automating buying thru Interest Radar and it works perfectly. I am now buying F and G notes automatically and only review it every day in the evening how that goes. I am satisfied and full steam…

Simon,

I have a suggestion for number “8,” but it may irritate “Retail Investors.”

It makes sense to me to take advantage of the institutional investor’s dive into P2P lending? I am sure these financial institutions and their 25% whole loan program, and high speed API advantages are hitting it big in the P2P world with averages well over 15%.

Do you think it is possible for an individual investor to jump into a P2P Fund with one of these institutional investors? I am sure they have big commissions, but if they are getting the preferential treatment that is implied above I am sure the difference after their commissions and fees is still a great return. Plus, you can sit back and let financially savvy investors with super fast and cool computer programs run your whole operation without much effort.

It sounds great in my mind, but maybe these institutions are not offering these types of funds to small retail investors, but rather are limiting them to the “elite” investors.

“If you can’t beat ’em, join ’em.”

Hi Gavin, Thats an awesome question. The moment I read about Institutional Investors, a quick thought of some kind of P2P fund or something crossed my mind but I just left it at that…didnt think of it again until I saw your post :-) Lets see what Simon or NJG say about it.

http://www.hedgeco.net/news/09/2013/petra-partners-launches-p2p-hedge-fund.html

Gavin, check it out. Petra Partners launches P2P Hedge Fund…exactly what you asked for. Not sure if the minimum investment is at least $100,000 :-)

Thanks Karthi,

That is good info. Its possible that this sort of thing is the future of P2P lending. If this is competitive, other institutional investors will no doubt start jumping on the bandwagon and suck up all the loans.

They suggest a 9-12% rate with very little volatility. That is pretty good especially when you consider Simon’s prior post about the expected long term returns of P2P lending.

Hi,

To use these third party tools, do every user have to sign the Lending Club API agreement?

Hi Varun,

Third party tools do indeed need to sign the API agreement.

For now, sites like Interest Radar do automated investing via the website, but eventually Lending Club is going to shut off third party website-based (screen scraped) investing and force all third party tools to API. In my opinion, going over to API as quick as possible is a good idea anyways, and only one site currently allows this: LendingRobot.

Best,

Simon

Hi Simon,

I’ve been reading a lot lately about good notes being gobbled up by institutions within seconds of being listed. What constitutes a “good note”? Obviously is not simply just the grade of the note. While becoming less prevalent on the platform, E-G notes do come up. Do you have any idea what qualities the 10-second-and-they’re-gone notes posses?

Thanks

Jaz

Hi Jaz. Check out the service at Lending Robot. They have a better answer to this than myself.