In the 1950s, it was common practice for banks to section off areas of their city as less eligible for loans. In essence, this was a form of racism. Poorer families, particularly black and Hispanic, would often struggle to get approved for a mortgage within these areas (source). Even if someone got approval, their mortgage often had larger down-payments and stricter repayment schedules.

This credit policy was called redlining, and the effects of it were devastating. Unsold homes fell into disrepair and were abandoned, property values fell, and life grew worse in the inner city. In essence, redlining simply exacerbated an already bad situation, stemming the flow of capital from the sole areas of the city that needed it most.

To address this problem, the Fair Housing Act was signed into law by President Lyndon Johnson as a part of the Civil Rights Act of 1968. This law basically made it illegal to deny someone a mortgage based on their ethnicity. This law was strengthened by another piece of regulation: The Community Reinvestment Act, signed by President Carter in 1977. This second law now required banks to have their lending practices periodically reviewed by the US government to make sure they kept in line.

I am a big fan of the Civil Rights Act of 1968. Millions of at-risk families have been helped by this law. That said, I am also a big fan of a new version of redlining, a smarter more modern derivative of its ugly racist former self.

Redlining in 2014 via Peer to Peer Lending

As many people know, the emergence of peer to peer lending in 2006 gave average Americans the ability to issue loans themselves. In peer to peer lending, an investor has the credit history of a prospective borrower laid bare before them. And while race is (thankfully) not included, a lot of personal descriptors still are. Most interesting is the presence of a borrower’s geography. And here is a fascinating thing that has come to light: certain areas of the United States have a lower rate of return than others.

Particularly Florida. Folks from Florida are less likely, in a statistically significant way, to pay back their p2p loans. So I have never loaned a dollar to people in Florida, and have gone on to earn a higher net return on my peer to peer investment than 90% of p2p lenders.

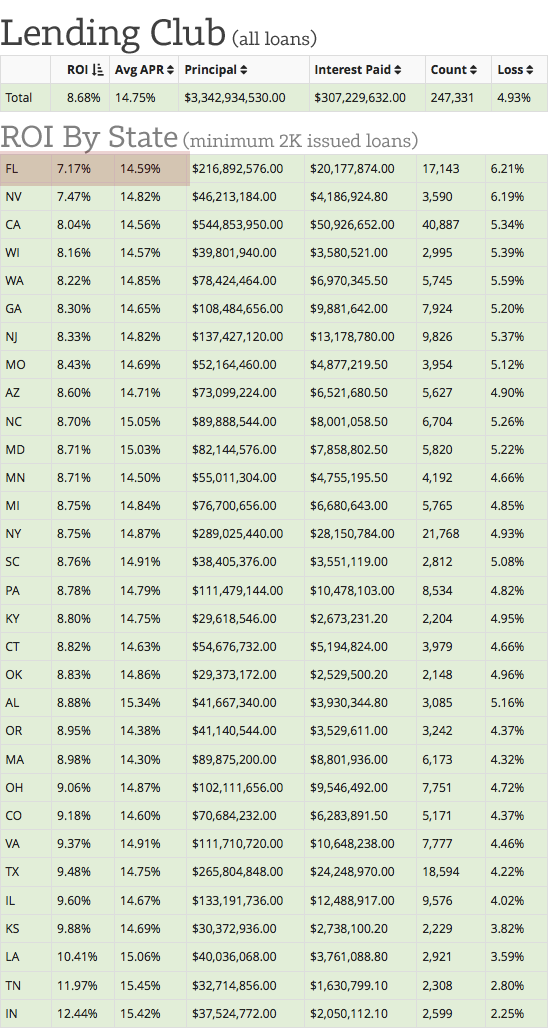

Let’s look at some juicy data from Lending Club (pulled today from NSR):

The above chart shows a couple of things. In the top box we see the entire return of all the loans in Lending Club’s history, $3.3B in issued dollars spread across almost 250,000 loans. The overall return for Lending Club? 8.68%

The bottom chart is where things get interesting. It lists the ROI by state in ascending order (excluding states where too few loans have been issued for a valid number). Basically, it shows the states at Lending Club that are the least likely to pay back their loans. And at the top of the list (and by a wide margin) is Florida with an overall peer to peer lending ROI of 7.17%, a full percent and a half lower than the national average.

Why Are People in Florida More Likely to Default on their P2P Loans? A Glance at Mortgage Habits

I. Floridians are more likely to be late on their mortgage payments

As seen in this beautiful graphic by Calculated Risk, one out of five Floridians were late on their mortgage payments in 2010. This is four times the normal national average, which is pegged at 4%. Here is another article from Bloomberg talking about Florida’s staggering 17% late mortgage rate in 2012.

II. Floridians are 2nd for being underwater on their homes

A house is deemed as underwater when people owe more on it than its current market value, and this typically happens to people who borrow against their mortgage right before housing prices fall. More interestingly, it typically happens to geographic areas that keep borrowing against their house instead of paying it off. Florida is second in the United States in this regard, with 38% of its mortgages currently underwater (USA Today).

From the same article:

In New Jersey […] borrowers in the foreclosure process haven’t made a payment for an average of 934 days, according to Lender Processing Services Inc. (LPS) New York, at 953 days, and Florida, at 938 days, are the only states with longer time frames. The U.S. average is 742 days.

III. Florida homes are twice as likely to be repossessed

Even though the rest of the United States has somewhat recovered from the massive housing bubble of 2008, Florida has not. It is still languishing with the highest rate of repossession nationwide (see: Florida Defies Housing Rebound as Foreclosures Soar via Bloomberg).

How Mortgages Compare to Peer to Peer Loans

If you think about it, it would make sense that people would repay their mortgages in a similar way to repaying their peer to peer loans. After all, both are fixed-rate amortizing lines of credit to prime borrowers. The same cannot be said about credit cards (though Florida seems to have high credit card delinquency rates as well), since they are sometimes issued to people with bad credit.

The national map for states that are more likely to be late on their credit cards corresponds more with poverty rates. Here are the states most behind on their credit cards:

- Mississippi

- Alabama

- Louisiana

- West Virginia

- Arkansas (source: the ‘Credit Cards’ tab here)

The 5 poorest states in the US?

- Mississippi

- West Virginia

- Arkansas

- Kentucky

- Alabama (source: Wikipedia)

Note: you can see further evidence of this in the list of peer to peer state ROI above. The average rate given on a peer to peer loan for Alabama is higher than the rest, meaning the borrowers there generally have lower credit scores.

In essence, when comparing only the people who get mortgages and peer to peer loans, we are talking about a similar population of borrowers with decent credit.

Or so it seems.

Why Floridians Are More Likely to Default on their Loans

The reasons why Florida is more likely to default on their loans is subject to debate. After all, we are making a generalization here about the financial habits of 20 million people, so it is probably important that we tread lightly with what we say next.

The reasons why Florida is more likely to default on their loans is subject to debate. After all, we are making a generalization here about the financial habits of 20 million people, so it is probably important that we tread lightly with what we say next.

That said, let’s begin with a question: why doesn’t the map of states behind on their mortgage payments mirror the poverty map? After all, the states late on their credit cards corresponds with states in poverty, so why doesn’t it correspond with late mortgages as well?

The answer: getting a home loan requires good credit, and people in Florida are more likely to seem like they have good credit when, in reality, they don’t. To put it another way, issuers of both mortgages or peer to peer loans are less able to predict risk for people in Florida.

This leads us to the final question: why are credit scores soft in these regions?

The Frenzied Culture of Florida, California, & Nevada

What I am about to say next is only my opinion: I believe the reason why credit scores are less accurate in Florida has to do with the state’s culture. Even though a person may have perfect credit (no late payments, bankruptcies, etc.), the surrounding culture is one that is encouraging them to borrow beyond their means – to build a bigger house than they can afford, or to borrow more money than they can repay. And this cultural influence is going to make credit scores a less accurate prediction of repayment.

This was evidenced in 2008 by the mania of approved-mortgage construction in Florida, particularly when coupled with the volume at which these new houses were repossessed:

The historic boom and subsequent decline in the nation’s housing market has been a defining feature of the current recession. The housing downturn has been most acute in four states—Arizona, California, Florida, and Nevada—that had experienced some of the highest rates of home price appreciation in the first half of the decade. (The Sand States: Anatomy of a Perfect Housing-Market Storm” FDIC.gov 2009)

In short, FICO does not weigh Jacksonville. Good credit scores on paper in these four states do not account for the fact that they exist in a boom and bust geography.

However, even though mortgage issuers ignore a person’s geography does not mean we have to as well.

Why I Never Lend Money to Florida

In summary, the data seems to indicate that prime-rated Floridians (followed by California & Nevada) are more likely to be financially irresponsible than people in other states. This does not mean all people in Florida are this way, but when aggregated, this is the picture that is painted. And while I find it ridiculous to deny a loan because of a person’s ethnicity, I find some sort of justice in redlining geographies that live beyond their means.

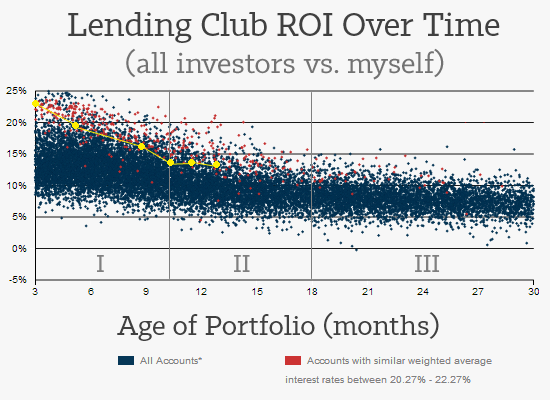

Using the Portfolio Analyzer on NSR, I’ve placed a pin on every city I have loaned money to at Lending Club. An interesting picture has begun to emerge:

The result of this practice? An overall return at Lending Club & Prosper that is greater than average:

Conclusion: The Joy of Redlining

Peer to peer lending presents us with a tremendous opportunity. For starters, we have the ability to amp our returns by avoiding geographic parts of the country that are historically less likely to repay p2p debts. Perhaps more importantly, we have the ability to inject a small bit of reality into the so-called Sand States, the areas of the country that contain higher prime-rated financial irresponsibility. Hopefully, with less credit available to them, and subsequently with less of an ability to take wild risks, these bastions of boom and bust will be relegated into humbler, healthier, more responsible versions of their former selves.

[image credit: Sarah_Ackerman “Sunset over Miami”

Sue Elias “florida” CC-BY 2.0]

I also don’t lend to Florida because the filters have told me so. This is an excellent analysis to back that up and to use in future filtering.

-RBD

Hear hear! Thanks for stopping by RBD.

Great piece of information, Simon.

Hi, Simon!

Nice piece of analysis in here. Keep up the good work! :)

Nice article…..from reading your site and a few others on P2P lending, I’ve incorporated similar filters in my Lending Club account, excluding FL and CA from my pool of potential loans. I love the level of granular detail that is emerging from their pool of existing and potential loans, allowing investors to do their homework and make better decisions.

Absolutely. Thanks for stopping by Jeff.

Simon….an amazing piece! Kept my attention from beginning to end. Excellent stats. I need to to take a closer look at that when choosing my own notes. Very well done!

A pin on every city, eh? Another reason you don’t have any kids!

Thanks for stopping by NJG

While this is interesting analysis, I think it would be helpful if you took it a step further in de-averaging these accounts. It might be possible that FL accounts are skewed in other ways (e.g. all unemployed, using loan for medical, etc). Also, I wonder how much of this is based on timing (worst performance from a while back during the crunch of the housing crisis).

Not saying you are wrong, but I would be more convinced if you looked at a more tightly defined group (e.g. loans <2 years old, by grade, controlled for major variables like use, DTI, employment length, etc).

Hi Zack,

I’d be tempted to do further analysis, but the raw sample size of florida (17k loans) is one of the largest of the group. For the average to be overaffected by a single factor such as employment or loan purpose, it would have to be quite an exceptional one indeed. If you’re able to play with the numbers at nickelsteamroller.com (or beta.nickelsteamroller.com) and show some decent evidence to the contrary, I’d be willing to update this article.

Cheers,

Simon

Here is what I have been proposing for at least a year, here’s the deal. We (the U. S.) pay off Spain’s debt. All of it. Make them completely whole. They (Spain) take Florida back.” I figure that’s a pretty even trade. If the global warming people are even half right Florida will be under water in a few decades anyway.

I didn’t know that Californians were such poor payers of debt. The CU numbers I used to see in CA were in line with the rest of the country. Maybe it’s all that sunshine or the resignation over the next “big one” coming any minute.

Red lining by culture. Now that is an interesting concept.

“Perhaps more importantly, we have the ability to inject a small bit of reality into the so-called Sand States, the areas of the country that contain higher prime-rated financial irresponsibility. Hopefully, with less credit available to them, and subsequently with less of an ability to take wild risks, these bastions of boom and bust will be relegated into humbler, healthier, more responsible versions of their former selves.”

Nevada where the population is concentrated in Clark Co i.e. Las Vegas was built on the concept of taking wild risks. lol

As I recall from the interview Simon did with Peter, Simon started his career as a preacher, seems he still has some of it in him.

I wonder if this trend has more to do with when Lending Club started issuing loans to particular states. For example, if the data includes CA loans since 2010, but IL loans since 2012, the default rates will naturally be much higher for CA because more time has passed.

Interesting article. However, I think the line

“So I have never loaned a dollar to people in Florida, and have gone on to earn a higher net return on my peer to peer investment than 90% of p2p lenders.”

is a little misleading. You are above 90% because of the overall risk you are taking (i/e the weighted average of your loans) not because you avoid Florida. If you look at your peer group (those with average rates between 20-22%) one might say that you were underperforming. Maybe the top performers separate the wheat from the chaff in Florida and get rewarded with higher returns…food for thought.

Hi Stanny.

In some ways, you are correct. The average rate on my loans at Lending Club is 21%, so I would not be earning 12% unless I took on that risk. That said, there are people with a similar weighted average who are earning a lower ROI than me. So I have to believe that redlining Florida has certainly helped (albeit to a limited degree). As for people supposedly earning 20% in peer to peer lending, that is an unsustainable return. Either (1) their accounts have not aged or (2) they are active trading on Folio.

Best,

Simon

I run my loans through three separate filters sets (each capable, independently, of picking up a loan for me). Wouldn’t it be best to simply include some of these ‘poor RIO’ states in my most stringent filter ?

Wouldn’t this help to pick some of the ‘low hanging fruit’ that, inevitably, is available – regardless of location ?

I would argue that these “poor ROI” states will always have a lower return within even your stringent filters when compared to the rest of the states. IE: even in my strict filters, FL is not enabled for investment.

Was wondering if you have incorporated unemployment rates at the local or county level to exclude loan listings? For example, if a state, such as California, has an unemployment rate of 7.9% and Kern County (CA) has an unemployment rate of 10.3%, instead of excluding all California, just exclude Kern County listings since its unemployment rate is significantly higher than California. The county for a loan listing can be retrieved from the Google Map API and unemployment rates can be retrieved from the Bureau of Labor Statistics API.

I have started to use county and state unemployment rates to further filter loans (don’t have an idea if it has made a difference yet since I’ve only been using the unemployment rates for 2 weeks so far).

My novice opinion feels like that would be an excellent tactic, Kirk. I have not broken down returns by county myself, but doing so is simply pushing this article’s state-based tactic up another level. I would love to hear your results in the next couple years (and I know others would as well).

In my opinion, excluding an entire state is just silly. By doing that you are excluding a lot of high quality loans from that state. Sure they may have some mortgage payment issues, but what about the people who rent or own their home? I’m sure there are plenty of people in FL which always pay their mortgage on time and and have equity in their home. I wouldn’t worry about what state a person resides in, I’d worry more about their financial history and filter based on that.

Hi Database Guy. I’m not arguing, by any means, that there aren’t good people in Florida to loan money to. I have friends who live there, people who I personally would entrust with a loan.

What I’m saying is that, on the aggregate, the state is a worse investment for prime consumer credit than the rest of the country, and that this realization is a reflection of the state’s culture. Furthermore, I’m saying that FICO (typically a solid predictor of creditworthiness) fails to consider a state’s geography and culture within its score, and thus is a weak predictor of repayment for these locales.

You say you wouldn’t worry about the state the person resides in, just their “financial history”. But I would ask you this: would you not consider the person’s employment status? Would you not consider that the person is borrowing money to begin a business? These are predictors of repayment, yet have nothing to do with an applicant’s credit history. However, a lender would be ill-advised to ignore these factors when considering these borrowers as worthy investments.

Thanks for your comment.

“Furthermore, I’m saying that FICO….”

Picking a nit here, but IIRC, Lending Club (and Prosper) use credit scores which are not FICO.

They use FICO. See: http://blog.prosper.com/2013/08/30/fico-08-score-comes-to-prosper-and-what-it-means-for-you/

To the question, “Why I Never Lend Money to Florida,” you answer, “In summary, the data seems to indicate that prime-rated Floridians (followed by California & Nevada) are more likely to be financially irresponsible …”

You kinda blindsided me with that because I didn’t get that from your article and your data at all. Instead, I thought this part was very key: “And this cultural influence is going to make credit scores a less accurate prediction of repayment.”

Altho’ I’m not entirely convinced culture is to blame, I would agree that there are geographic areas where credit scores are weaker predictors than in other areas.

But so then if subprime-rated borrowers are mistakenly rated prime because credit scores are less accurate in some areas, then we can’t place the blame on irresponsible borrowers. Rather, that’s something the CRAs are inherently missing.

So I submit that the take-away for lenders is not to avoid areas which meet the criteria of your summary statement (areas of “financially irresponsible” borrowers) – that’s what filters are for – but to avoid areas where lenders are left in the relative darkness of less meaningful credit scores. (And I would agree that FL, CA, NV are such areas.)

And then I suspect that if one took the time to continue looking, we’d eventually find that credit scores are less reliable under other criteria as well ( not just geography ).

Hi there. Thanks for the great comment. I think I could have stated this better. Basically, the onus of blame resides in the credit reporting agencies (CRAs), as you say. The point of the post is not to direct blame, but to suggest a generalized investment tack that both increases returns and justly denies lines of credit where they may be misued.

That said, the article also serves as a wider social commentary on the culture of these areas. The culture shares blame alongside the CRAs, which in my opinion, aren’t allowed to consider geography because of regulation that was issued in the wake of racial stereotyping. In this way, I think it’s valuable to be honest about the social problems latent in these cultures, and to pick up the slack where the CRAs fail to do so.

I’m really interested what other criteria you think the CRAs fail to consider (and agree there are probably others out there).