Part 1 – An Overview

Part 2 – Lending Step-by-Step

Part 3 – Filtering Loans

Part 4 – Final Pieces

In part three we looked at how to filter the platforms for higher-quality loans. For this section we will be looking at how to maintain and close your account. Unlike trading in the stock market, peer to peer lending is mostly a passive investment, meaning it does not require very much involvement once your account is first set up. Stock traders often have to check their accounts throughout the day to respond to any swings. Lending Club or Prosper accounts, in contrast, typically remain steady.

That said, once you have set up a diversified portfolio (filtering the platforms to buy notes in at least 200 quality loans) there are a few final things you still need to do.

Reinvest Your Returns

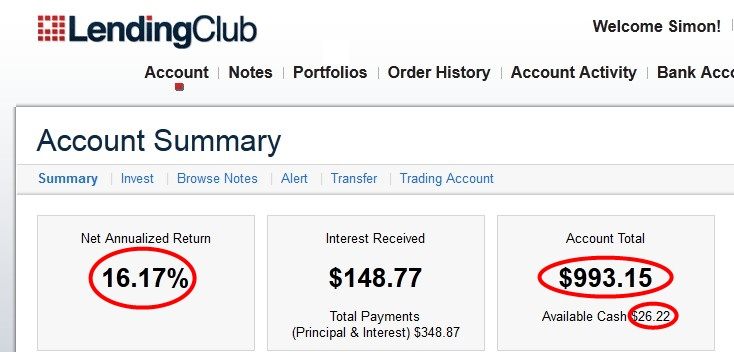

The most important thing you need to do is reinvest your returns. Once money from your invested loans starts flowing back into your account, you should reinvest this money into the platform. If you let these funds lie dormant in your account they do not earn interest. It is important to set up a routine where you log in and reinvest your available funds on some sort of schedule. Those with smaller accounts may only need to log once a month, but those with larger accounts may need to check in more regularly.

(click to zoom)

The above image is a screenshot of my Lending Club account with $26.22 in available funds (enough to purchase another note).

Note Status

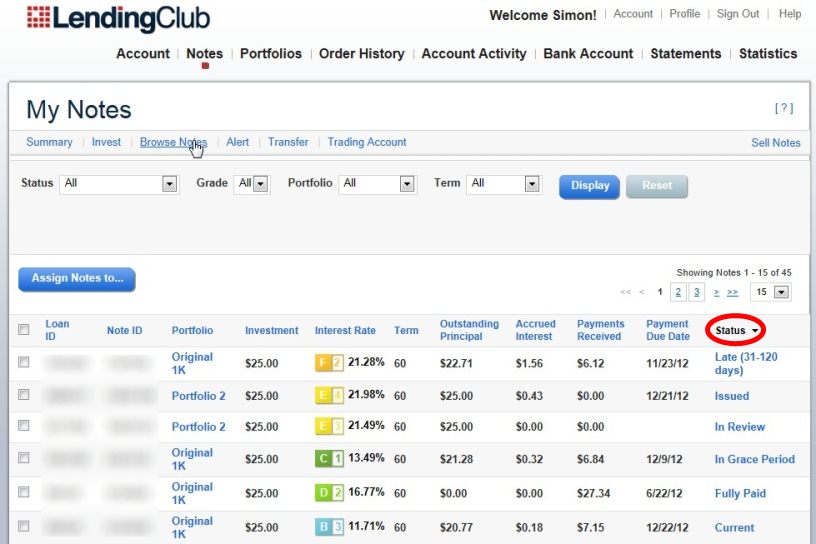

You also need to be aware of the status of the notes in your portfolio. You can do this through the “Notes” page. In both Lending Club and Prosper, you can go there by clicking on the “Notes” link at the top of your account home screen. On this screen, you will see that each of your notes have been given an individual status.

(click to zoom)

Before notes are issued, they will either have a status of In Funding or In Review. This means the note has either not been fully funded by additional lenders, or that the platform has not finalized its approval of the loan. However, once the note is approved and fully funded, it receives a status of Issued.

Issued notes are classified into five categories:

- Issued – An approved loan that has not yet received its first payment

- Current – A healthy loan being paid back on time

- Late (or In Grace Period) – A loan that is behind on its payments

- Default (or Charged-Off) – A failed loan that will not be repaid

- Fully Paid – A loan that has been completely paid back in full

A good healthy loan will move through three stages: from Issued to Current, and finally to Fully Paid.

Borrowers Who Are Late

Sometimes a borrower will be late in repaying their loan. Late loans will first be given a grace period to fix themselves, after which they receive a ‘late’ status. When a loan first goes late, there is usually little reason to worry. Almost all late loans are just borrowers having a temporary problem. For instance, if a borrower switches banks and forgets to tell this to Lending Club or Prosper, their next payment will fail and their loan will go late. The platform then contacts the borrower about the problem. The majority of late loans recover their payments within a few weeks.

Borrowers Who Default

Unfortunately, a small number of these late borrowers do not resume their payments but default, which means they will not pay their loan back. This is the worst part of peer to peer lending, because it means you lose the funds you invested in that note. While all investors are likely to experience a loan defaulting eventually, it can still be shocking the first time it happens. The best thing to do is to take a moment to look at all the loans in your account that are being paid back on time. If you are diversified in at least 200 notes, the negative impact of a single default should be quite small.

If you find that a number of your notes have defaulted or gone late, this can sometimes be quite helpful. Take a moment to examine their original descriptions side by side and see if they have any similarities. This could inform a change to the way you invest. A common factor among your defaulted loans might reveal a problematic filter to fix.

Closing Your Account

You will eventually want to get your investment back. This is where we get the word liquidity, a term that refers to how freely you can get actual cash out of Lending Club or Prosper’s system and back into your bank account. One benefit of peer to peer lending is how liquid your accounts are, far more than investing in stocks or mutual funds. With stocks, your investment can often take a huge dive around the time you need the money. This is how investors can get stuck, often having to wait for years before their account recovers and they can close their investment without too harsh a penalty. Peer to peer lending, on the other hand, allows for a couple very efficient ways to remove your investment:

Best method – Stop reinvesting your returns: If you simply stop reinvesting your returns, cash that you can withdraw will begin to build up in your account. For people who only buy notes with a 36-month term, they can have half their account in cash within 18 months without any penalty at all.

Quickest method – Sell your notes through FOLIOfn: Both Prosper and Lending Club allow you to sell your healthy notes at any time. If you needed to liquify your investment, you could post your notes on their secondary markets (a service run by a company called FOLIOfn). The bigger hit you take on your notes, the quicker they would sell. Using this method, you could liquify your account within a week. Attach a FOLIOfn market to your accounts by clicking “Trading Account” on Lending Club or by clicking “Trade Notes” under the “Invest” menu in Prosper.

Taxes (And How to Avoid Them)

There are generally two types of accounts in peer to peer lending: regular taxable accounts and retirement accounts. Regular lender accounts do not have a unique tax rate like capital gains, so if you are in a 30% tax bracket then you will pay 30% in taxes on your peer to peer investments. But Prosper and Lending Club also offer great retirement account options like Roth & Traditional IRAs that have added tax incentives. There are important details to know about these accounts (and about IRAs in general). Those details are beyond the scope of this article, so it would be a good idea to read up on these details before investing. Speaking as someone who has a peer to peer IRA, it’s amazing to watch one’s balance grow tax free.

Conclusion

This completes our four-part series on the basics of peer to peer lending. I know this may feel like a lot of information to take in, but if you open an account with just a few notes, lending will start to become quite familiar. Remember, the best way to absorb new information is always through first-hand experience.

The best advice I can give you is to go slow. Be curious, be patient, and enjoy the process. Peer to peer lending is a wonderfully rewarding way to invest our extra savings. Given a little time, I believe it can become as second-nature as depositing a paycheck in an ATM.

Questions or comments? If you enjoyed this please Like or Tweet it below.

[image credit: Andrew Plumb ‘IMG_5621‘ CC-BY 2.0]

Leave a question or comment