At some point in our lives, our bodies break down. Muscles and joints weaken, memory gets fuzzy, and our ability to earn money and pay the bills begins to decline. This is reality. Thankfully, our country has always placed a big emphasis on saving for retirement, investing chunks of cash over a lifetime in order to draw on this retirement account as we become older.

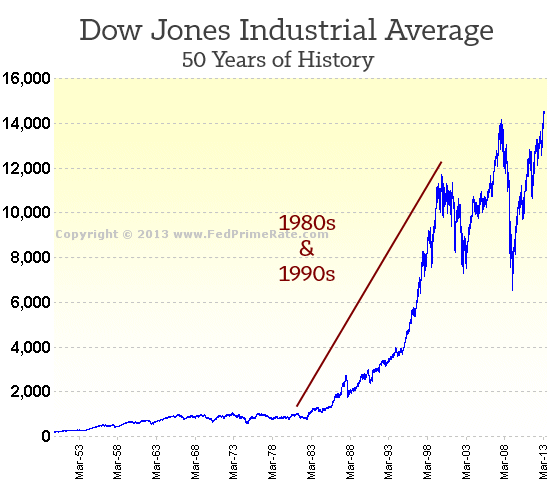

This used to be easy. In the PBS Frontline documentary The Retirement Gamble, an analyst speaks fondly about investing thirty years ago. “In the eighties you could not lose money in the stock market,” he says. Back in the day, the overall momentum of the American economy was so strong that investing became almost hilariously easy. Many of those who saved for retirement through in the stock market during the 80s and 90s eventually became millionaires.

Oh how times have changed…

These days, the market is more known for its uncertainty than its certainty. People throughout the nation who invest their 401k or IRA in mutual funds are not nearly as rewarded as they used to be.

The End of Easy Money

I want to make an argument today that the age of easy money is over. The glory days of taking 15% of your paycheck, entrusting it to a Wells Fargo or Merrill Lynch mutual fund over thirty years, and retiring comfortably are history. The new norm is doing the work ourselves. If we want to have a thriving retirement account, we are going to have to learn the ropes and be our own boss.

This is not just the end of easy money; it is the end of easy everything. Nationwide, the well-worn paths to financial security are less and less trustworthy:

- High school diplomas are almost worthless

- College degrees mean less and less (especially BAs)

- Job openings are incredibly competitive

- Most jobs are now skill-based (coding, nursing, etc.)

- Layoffs happen with great consistency

So how exactly does one take their retirement account into their own hands and earn a consistent great return? There are a number of solid ways. Most notably, self-directed IRAs allow almost anybody to save for retirement through whatever investment they choose (see wikipedia). For a long time, the self-directed IRAs have been used by middle-aged investors placing equity (like housing or land) into a retirement fund, drawing it tax-free when they turned 65. However, this approach can require a lot of money up front, a down payment for example.

For the average American who is just getting started, what other options exist? How can somebody in their twenties begin saving for retirement in a way that earns a solid return?

P2P Lending Roth IRAs: A Breath of Fresh Air

Enter the peer to peer lending IRA. Both Lending Club and Prosper offer the option to invest in their platforms with a self directed IRA (see my comparison of them here). As somebody who has opened a Lending Club IRA myself, I found the whole process quite easy. Both Lending Club and Prosper manage their IRAs through a separate company (in Lending Club’s case it is SDIRA). Furthermore, both platforms waive the fees as long as some minimum requirements are met. Lending Club, for instance, waives all the fees if you open an account with $5,000+ and have $10,000 invested within a year. You can start with less, but you’ll be charged $100 per year.

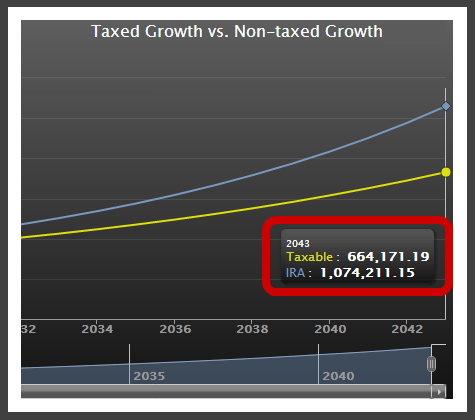

I’m not sure people realize how truly phenomenal an investment grows through an IRA. Thankfully, BankRate has created a free IRA Calculator tool that reveals tax-free growth in all its glory.

Lending Club IRA Calculator Example

If I start out with a $5000 investment, deposit $500 every month, and experience an average of 10% growth, my retirement account will have $1.07 million in thirty years time. However, if I ignored the IRA option and tried doing the same thing through a regular taxable account, I would only have $664,000 (at 25% tax). This shows that, over a lifetime, over 1/3 of our earnings can get eaten up in taxes.

What is the difference between a retirement account with $1.07 million and $664,000? If I retire at age 65 and burn through $35,000 each year, $1.07 million will get me to age 95. In contrast, $664,000 only gets me to age 84.

Put more bluntly, a peer to peer lending IRA can mean the difference between life and death.

The New Norm: Self-Made Retirement

I believe PBS Frontline when they say a national crisis is coming. Over the next thirty years, it is very likely that we will begin to see fewer and fewer people having successfully prepared for retirement. Thankfully, for those able and willing to do the work, great self-directed options exist. The path to retirement does not have to be one fraught with anxiety and uncertainty. Granted, we never can know if our work will pay off in the end. However, a peer to peer lending IRA seems to offer a far more stable and lucrative entry into investing than any other option today.

Personally speaking, I enjoy saving for retirement this way. It is fun to watch my savings grow while knowing I will withdraw them tax-free when I turn 65. Aside from the default-curve that settles down after a few years, my p2p lending IRA is a delightfully boring thing to maintain.

Open an IRA with Lending Club or Prosper.

Questions or comments? If you enjoyed this please Like or Tweet it below.

[image credit: Peter Burge “Captain Morgan” CC-BY 2.0]

This is naturally because of the declining economy and increasing population. Times have changed. You can’t expect everything to be easy all the time.

Amen

I concur. Electronic age added to that uncertainty as well. What was actual and up to date on the market a few seconds ago is no longer valid. Investors and trades can react to the new withing seconds, High frequency trading, all that added to a huge volatility unknown ever before. Al you can do is to adapt to it. But what strategy would work? Long term investing seems to be the answer and it appears that Lending club (or Prosper) or investing in consumer credit can be a new way of retirement creating effort.

Hear hear :)

Hi there

Thanks for your great article. I am turning 33 in a few months, and unfortunately, up until now, have not been good with money. But, I have finally turned things around and am researching retirement accounts now. I recently found out about iras through peer lending and was considering going this route. I think that is what I will do. Though, I was wondering what your thoughts were on gold ira’s? I have looked into that but not too much. I was considering having two different roths perhaps, and splitting contributions between the two of them–not necessarily 50/50 but to diversify I suppose. This is all so new to me.

Hi Kelli. Thanks for your comment. I have no experience using multiple IRAs at the same time, but I very much do enjoy my p2p lending IRA with Lending Club. What I do know is that you can only contribute $5000/year to an IRA, so if you have two then you would have to split this max contribution between them.

When you say 1.07 million will last to age 95 it looks like you are assuming 0% interest from retirement on??

A solid point!

Do you know if there is a minimum initial deposit/total balance for the fees to be waived with Prosper?

Good article, however you should change your scenario b/c the maximum annual contribution to an IRA is $5,500, or $458 a month – making a $500 monthly deposit not possible.

Going through an IRA is a great way to defer the taxes, the only issue I have with Prosper is the extremely long time its taking to transfer money into the account. Starting in 2013 through 2016 its taken on average 6+ weeks after my bank was debited to have the funds in Prosper, 6 weeks!

Now that Lending Club is available in my state I will be switching. Just though I would share my experience. No idea as to it can possibly take that long in this age.

10% average growth? What happened to, “I want to make an argument today that the age of easy money is over.”????? Get real

You’re reading an article from 2013. Back then, a 10% return at a site like Prosper WAS possible because the company wasn’t accurately pricing their loans, so it was possible to boost a lender’s return to 9-12% annually via filtering loans. These days the arbitrage opportunity is much less, so that return is much less possible.

With your scenario, is the $500 monthly investment including the principal payment from the borrower?