There are times in all of our lives where we need extra money. For example, a friend of mine told me yesterday that he is quitting his job because it makes him unhappy. This has required him to borrow a bit of cash from his parents until he finds another place of work. The fact is, my friend’s situation is not special. It is actually very normal. Everybody has seasons of their life where they fall behind on their bills and need to borrow cash until things get straightened out.

Loans up to $40,000 via Lending Club

Check your rate

Won’t affect your credit score.

Unfortunately, most people in the United States rely on credit cards to help them when times get tight, and it is easy to see why. After all, credit cards offer the easiest way for us to borrow money. Their advertisements are everywhere, and credit cards are what have helped out our friends and family in the past. The problem is that credit cards are only good for one thing: borrowing short term. They work best for temporary problems, when they are quickly used and then paid off. For long term debt, credit cards are a really poor way to borrow.

5 Reasons Lending Club Loans Beat Credit Cards

If you are going to hold onto debt long-term, a much better option is a peer to peer loan through Lending Club (up to $40,000).

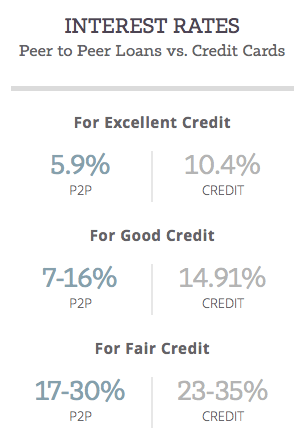

Reason #1: Lower Interest Rates

A peer to peer loan usually offers lower interest rates than credit cards. This is because the banks that issue credit cards are usually massive companies that cost a lot of money to run. But companies like Lending Club run through a quick website, so they are cheaper to maintain. They pass the savings onto the customer, with the result being low loan rates. So if you check your rate for a peer to peer loan, it is often lower than your credit card rate.

A peer to peer loan usually offers lower interest rates than credit cards. This is because the banks that issue credit cards are usually massive companies that cost a lot of money to run. But companies like Lending Club run through a quick website, so they are cheaper to maintain. They pass the savings onto the customer, with the result being low loan rates. So if you check your rate for a peer to peer loan, it is often lower than your credit card rate.

Secondly, I have some bad news for people with good credit. The credit card companies do not set interest rates based on your credit history (in the industry, this is called risk-based pricing). People with excellent credit history are simply given the same junky interest rate on their credit cards as people with bad credit.

A peer to peer loan, on the other hand, rewards people for their good credit. It gives them an interest rate based on their credit history. As a result, people with great credit are often given a much lower interest rate than any credit card could offer – as low as 6% on a loan.

Reason #2: Fixed Interest Rates

One of the most frustrating things about credit cards are their always-changing variable interest rates. When you first apply for the card, you are given an introductory low rate. Then, after some time has passed, the rate shoots up to its full amount. And then, if you are late with a payment, the rate can shoot up even more. For most people, this changing interest rate can mean a great deal of worry around holding credit card debt, like driving on the highway when the speed limit keeps changing.

A loan from Lending Club, on the other hand, is a very consistent way to borrow money. Its interest rate is fixed. You see, when you first check your rate on Lending Club’s website, you are quoted an interest rate based on the amount you want to borrow (note: smaller loans get lower rates). If you accept this loan offer and interest rate, it will never change. Ever. Even if you make a number of late payments, the interest rate will stay the same. So, not only does a peer to peer loan typically have a lower rate than a credit card (see Reason #1), but it stays low forever.

Reason #3 Fixed Terms

Debt is often a spiral. What I mean is that people who are in debt can find it easier to keep going into debt, spiraling into more and more debt with each passing year, and this problem is only made worse with credit cards. After all, you can simply charge more on your credit card anytime you want. For many people, this can feel like a one-step-forward two-steps-back situation. Even though they spend a few months paying down their credit cards, they get tempted to use the card again, and erasing all these gains can make a person feel like they will never be debt free – a very sad feeling.

But with a peer to peer loan, the debt only flows one way. You get the loan amount deposited in your checking account, and then you make monthly repayments on the loan until it is paid back in full. There is no option to suddenly go deeper into debt. In the industry this is called fixed-term debt, and is a much more peaceful way to get out of debt.

Example: say you are in $4,000 of credit card debt (the national average). If you take out a loan with Lending Club, you could apply for this amount. If you have a decent credit score like 700, perhaps your interest rate would be 13%. For a 3-year peer to peer loan of $4000 with a 13% interest rate, this would mean a monthly payment of $135 until the loan was paid back.

The beauty of this loan is how it gives you something concrete to look forward to. You can breathe easier, dear borrower, because in three years (December 2016) your debt will be completely paid off.

Bottom line: compared to credit cards, fixed-term loans are great for long-term debt.

Reason #4 Late Fees

Even the best of us run into financial trouble. For those of us in the middle of paying off debt, this can mean falling behind on our payments. It can be hard to imagine, but almost everybody in the world has fallen behind on their debts at one time or another.

Unfortunately, most credit card companies can give very harsh penalties to people who are late on their payments. They do this in two ways. First, they can charge a large fee for a late payment, often around $30. Secondly, a late payment can cause another increase of your credit card’s interest rate. As a result, just one late payment on your credit card can mean hundreds of dollars in new charges on your account.

Unfortunately, most credit card companies can give very harsh penalties to people who are late on their payments. They do this in two ways. First, they can charge a large fee for a late payment, often around $30. Secondly, a late payment can cause another increase of your credit card’s interest rate. As a result, just one late payment on your credit card can mean hundreds of dollars in new charges on your account.

A peer to peer loan has a much fairer response to a late payment. First, the late fees are smaller. Lending Club typically charges a late fee of $15, around half the amount typical of credit cards. Secondly, a late payment will never make your interest rate go up. Of course, its better if you would never go late in the first place, but if it happens then you can feel a little more at peace knowing that your interest rate will not change and the charges will not be too bad.

Reason #5: Debt Consolidation

Lastly, people who are in credit card debt typically have a number of different cards, all with different amounts and interest rates. This can often result in missed payments, since it can be hard to keep track of which payments are due. Speaking from experience, I recently got very close to having a negative mark on my credit score, since I misplaced the bill of my Bank of America credit card. I only called them and got things straightened out because they sent me an email reminding me that my bill was due.

A loan with Lending Club, on the other hand, can allow you to move all your debt into one place (and with a lower rate). Instead of trying to remember what credit card bills are due at what times during the month, a peer to peer loan simply makes one regular monthly deduction from your checking account, usually automatically and on the same day of each month.

Consolidating your debt with a peer to peer loan can mean a much more relaxed life for people trying to get out of debt.

Ditch the Card. Go with Lending Club.

It would be nice if we never needed credit at all. Life would be much simpler. However, most of us do need credit at some point in our lives, and most people choose to use credit cards to go into debt.

It is important to state that credit cards can often serve a great purpose. They can be a great “utility vehicle”, allowing us to make all our charges onto one plastic card in our wallets or purses. I personally use a credit card for all my purchases, including the fees associated with this website. However, as a place to keep long term debts, credit cards are pretty lousy. Personally speaking, I pay off my credit card every month and do not carry a balance.

A peer to peer loan, on the other hand, is a much better option for people who need a long-term line of credit, who are going to be in debt for a number of months or years. As stated in this article, a loan through Lending Club offers five benefits over a credit cards.

- Lower interest rates (especially if you have good credit)

- Fixed rates never change

- Fixed term

- Smaller late fees

- Debt consolidation

Check Your Rate at Lending Club

For a quick low-rate loan, Lending Club is one of the best options nationwide. You can check your rate with no risk of it hurting your credit score.

Won’t affect your credit score.

[image credit: Consumerist dot com “cut the card”

Heather Paul “Rate on 30-year fixed mortgage rises to 4.87 pct.” CC-BY 2.0]

My father is and has been a business owner for the past 16years. He brought this concept of CRUSHING my debt and not be at the mercy of the Credit Card Companys. I truly am hoping I have a credit score that will allow me to get ahead, even if this means I must wait and put in more work to elevate my score. I know personally more then a few couples that would this would bring HOPE to.

Glad to hear it. Thanks Amend.

Do i have to close my credit cards if i do this?

That’s a personal decision. The point of the post is to encourage you to not keep debts on your credit cards.

What does your credit score have to be

Does getting a personal loan from the lending club leave a bad mark on your credit report?

Hi Tracy. No it does not. Just make sure to make all your payments on time.