For people who are looking for a loan, Discover can seem like a good option. By simply going to their website and submitting an application, you can get thousands of dollars in loans. Unfortunately, many people do not realize that there are better options out there. Today we will look at Discover, showing how a peer to peer loan through Prosper is a much better option.

Loans up to $40,000 via Prosper

Check your rate

Won’t affect your credit score.

Review: A Loan at Discover in Four Steps

Getting a loan through Discover is not much different than getting any other loan.

First Step: Fill Out An Application

The first thing people always do is apply for the loan online. Perhaps they heard about Discover through a friend or saw one of their ads. Either way, they (1) go to the website and (2) submit their information. The application will need some personal information so that Discover can look at the person’s credit history.

Second Step: Loan is Approved (or Denied)

This credit history that Discover asks for with each application is what they use to approve or deny the loan. They typically make this decision quite quickly, perhaps within 30 seconds of the application being submitted.

This credit history that Discover asks for with each application is what they use to approve or deny the loan. They typically make this decision quite quickly, perhaps within 30 seconds of the application being submitted.

Discover will then offer the person an interest rate. On their website, Discover says rate this can be as low as 8% or as high as 19%. The person applying for the loan then has the option to either accept or turn down this rate. If they accept it, the loan is approved.

However, even if Discover approves a request for a loan, most applications need extra review. This may mean that the person who wants the loan is required to fax in last year’s tax returns or send in copies of pay stubs from their work so that Discover can verify their identity.

Third Step: Cash is Received

Once everything is reviewed and gets final approval, Discover will officially issue the loan and send over the cash. This usually happens 7 to 10 business days later.

Fourth Step: The Loan is Slowly Paid Back

Finally, the person who applied for the loan would make fixed monthly repayments each year until the loan is completely paid back. This number of years is called a loan’s term, and Discover’s loans have a term between 3 and 7 years.

For example, imagine you took out a five year loan with Discover for $10,000. If your loan had a 12% interest rate, the monthly payments would be $222 each month for sixty months.

5 Reasons Why Getting a Loan with Prosper is Better

Unfortunately, most people who apply for a loan at Discover have no idea that there are better options out there, particularly with a peer to peer loan through a company like Prosper. Here are five big reasons to dump the orange circle:

Unfortunately, most people who apply for a loan at Discover have no idea that there are better options out there, particularly with a peer to peer loan through a company like Prosper. Here are five big reasons to dump the orange circle:

Reason #1: Prosper Has Lower Rates. Period.

At Discover, the interest rates are too high. For people with great credit history, their interest rate will be 7.9% (basically 8%). At Prosper, the rate for people with great credit is 6.73%. That is over a full percentage point higher.

Does an interest rate 1.2% higher even make a difference? It totally does, especially for larger loans. Imagine you got a $18,000 5-year loan at these rates with both Prosper and Discover. With Discover, you would pay $3,893 in interest. With Prosper you would pay $3,247.

A difference of 1.2% would mean you would pay an extra $645 for the exact same loan!

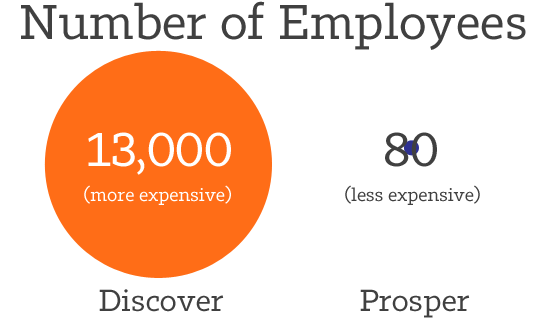

Why does Prosper have lower rates than Discover? Simple. Because they are not a bank. Discover, as a very large company, has thousands of employees they have to pay salaries to.

But Prosper is not a bank at all. It runs completely through a website. And since it has such a small footprint, it offers lower rates than Discover ever could. Don’t believe me? Click below to check your score at Prosper. Most people will find the rate is cheaper than their rate at Discover.

Reason #2: Prosper Loans are Quicker

If you are applying for a loan, chances are you need the money quickly. Perhaps your credit cards are calling you every day. In that case, the sooner you get this money and pay them off, the better.

Discover, as their website states, typically moves this loan over to you between 7 and 10 business days later. This means it might take a long time for you to get the money. For example, say you got accepted for a Discover loan on a Friday and they took 10 business days to issue the loan. You would get the cash on a Thursday almost two weeks later.

Discover, as their website states, typically moves this loan over to you between 7 and 10 business days later. This means it might take a long time for you to get the money. For example, say you got accepted for a Discover loan on a Friday and they took 10 business days to issue the loan. You would get the cash on a Thursday almost two weeks later.

Prosper, on the other hand, gets people cash much quicker, as fast as four business days. Personally speaking, I applied for a loan from Prosper on a Monday. On Thursday that same week the money was in my checking account. You can read about the whole experience at my review of Prosper.

Reason #3: Discover Has Expensive Fees

If you miss a payment on your Discover loan, their website says their late fee is $39:

There are no fees or penalties charged on a personal loan if you make your payments on time. We may charge a $39 fee if your payment is late or if you do not have sufficient funds in your bank account to cover a payment made.

(Source: Discover.com)

But Prosper’s late fees are less than half that amount: just $15. As I said before, this is because Discover as a company is more expensive to run, so they need to charge larger fees to cover the difference. But because Prosper is simply a website, it can keep late fees low.

Reason #4: Prosper Allows Larger Loans

At Discover, the largest loan they offer is $25,000. But many people are looking to consolidate credit card debt that is larger than this. Thankfully, Prosper allows loans up to $35,000. And considering their interest rates are lower, many borrowers will find they would pay the same amount of interest on a $35K loan at Prosper as on a $25K loan at Discover.

Reason #5: Prosper’s Loans Are Funded By People

Discover, being a bank, issues these loans using its large supplies of cash. Prosper, on the other hand, is a peer to peer lender. This means it funds its loans using the money of people from all around the country. So we have the option to apply for loans at Prosper and we can also help fund these loans (I have done both).

If you borrow money from Prosper, the loan has a much better overall feel to it. After all, it is not coming from some faceless corporation but from flesh-and-blood people around the United States. And you can be confident that you will take your loan payments more seriously, because if you fail to pay the loan back then it is actual people who lose out, not some massive bank.

If you borrow money from Prosper, the loan has a much better overall feel to it. After all, it is not coming from some faceless corporation but from flesh-and-blood people around the United States. And you can be confident that you will take your loan payments more seriously, because if you fail to pay the loan back then it is actual people who lose out, not some massive bank.

Conclusion: Prosper’s Personal Loans are Better

The fact of the matter is this: both Discover and Prosper offer the same product — unsecured personal loans to people with decent credit. However, that is where things stop being the same. If we look at Discover, we see how it is an expensive and bulky corporation that offers high-interest rates on its personal loans. The only real benefit they offer is the ability to repay a loan over seven years (Prosper’s max is five years).

Compared to Discover, Prosper’s personal loans have:

- Lower interest rates

- Quicker approvals (cash in 4 days)

- Lower fees

- The option for larger amounts (up to $35,000)

- Funding from people like you and me

Prosper in the News

If you have never heard of Prosper, here are some great articles about them:

- New York Times (Dealbook)

- The Wall Street Journal

- Fox Business

- NPR

Bottom line: Check your rate with Prosper

Seeing what your rate would be on a loan from Prosper is really simple. After clicking the link below and submitting some basic information, you will be offered an interest rate less than a minute later.

Seeing what your rate would be on a loan from Prosper is really simple. After clicking the link below and submitting some basic information, you will be offered an interest rate less than a minute later.

Loans up to $35,000 via Prosper

Check your rate

Won’t affect your credit score.

[image credit: MLoperative “Discover”

Hobvias Sudoneighm “/Approve”

“Money, Money, Money” by Daniel Borman

“Mother & Daughter” by Rolands Lakis CC-BY 2.0]

This appears to directly compete with P2P platforms. No origination fees either. Many banks have tons of cash at the Federal Reserve making very little interest. I can see them throwing a bunch of that in something like this.

They may end up cannibalizing their own credit card market by doing this but it could end up bringing down yields in P2P. Good for borrowers, not so good for investors. Am I overreacting here? If so, why?

Not overreacting at all. In short, p2p is just too small for it to be considered a massive threat, though it will actually become that. But even though banks may have better access to cash, they can’t issue loans cheaper than p2p companies like Prosper, so in end the banks lose.

Had a discover card since 2001, love it! Recently got a loan for $9,000. It only took 15 to 20 min on the phone and I was approved and four business days later my high interest card was paid off. Oh and my interest rate is 7.9%. So I don’t agree with a lot of the statements in comparison!

Hi Linda.

Great you had a positive experience with Discover. However, (1) you got your loan in four days, and (2) your rate was 7.9%.

In contrast, Prosper funds their loans (1) in *three* days and (2) has lower rates, just 6% for people with excellent credit.

Glad you had a good experience though,

Simon

Simon, You forgot to mention Prosper charges closing fees. So, if apply $20,000 you dont that much amount deposited. I got a loan approved for 7.16%. But including the fees, the effective APR is 8.531%

Hi Simon. Thanks for posting. I just got off the phone with Discover and was told that they do not have the 5% closing fees at Prosper or LendingTree. It would seem to me that this is a huge difference, even if the interest rate could be slightly higher and it could take a few more days for me to get the loan funds. Am I missing anything?

Hi Clark. It is true that Discover does not have the closing fees. However, even with these closing fees factored in, the overall cost for a Lending Club loan is far cheaper than Discover, at least on average. That said, you should go with whatever gives you a cheaper loan overall (including closing fees and interest rates). Everybody’s situation will be different.

I have a question for Prosper? I have had two personal loans in my life. One with HFC ( many years ago) and one with Discover, which I recently just made my last payment on. The very real and important difference to me especially coming from someone in the mortgage industry is that my Discover loan reflected as an installment debt on my credit report; whereas,, the HFC loan reflected as revolving debt. This does affect your credit rating and potential your borrowing power. How are Propers loans reported?

Applied and response was that Prosper does not lend in my state(Pennsylvania) . May want to disclose this so that others do not waste their time