When describing peer to peer lending to people for the first time, a typical response is disbelief. “Let me get this straight,” people say to me. “You are lending money to total strangers? Over the internet? Isn’t this risky?” The short answer is a definite yes. There are real dangers involved with investing our extra cash at Lending Club or Prosper. If we are not careful, it is possible to lose money on this investment.

However, if we are aware of the risks beforehand then we can be prepared for them. We can structure our lending habits so as to minimize the chances of something going wrong, setting a foundation to have a more positive lending experience.

The seven major risks in peer to peer lending are:

- Borrowers could default on their loans

- The platforms could make mistakes in their underwriting

- Lending Club or Prosper might go bankrupt

- A rise in unemployment could cause increased defaults

- New regulatory hurdles could bring hardship

- Interest rates may rise

- Additional unexpected catastrophe

Let’s look at each of these risks in greater detail.

Risk #1: Borrowers Could Default on their Loans

Despite our very best efforts, even if we select only the highest-quality borrowers who seem exceptionally safe recipients of our cash, most of us will eventually experience a default – a borrower who does not pay their loan back.

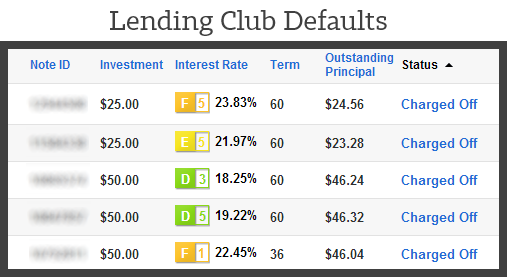

Here is what defaulted loans look like on Lending Club:

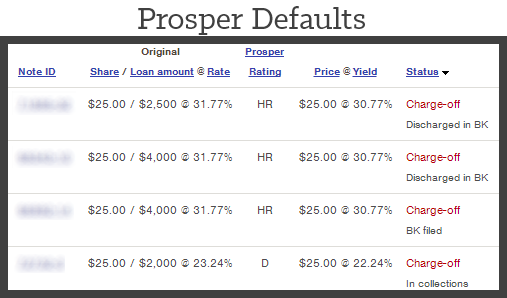

And here is what defaulted loans look like on Prosper:

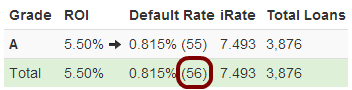

There truly is no fail-safe way to invest in peer to peer lending. For instance, on the Return Forecaster at Nickelsteamroller, I created a filter for what I consider an extremely safe investment: A-grade borrowers with 10+ years of employment and no inquiries, late payments, or past bankruptcies. Yet even this strict filter had 56 historical defaults (out of 3800, which is quite low). This proves that no cross-section of borrowers, no savvy filter, and no diversified peer to peer lending portfolio is able to avoid non-paying borrowers. None.

There truly is no fail-safe way to invest in peer to peer lending. For instance, on the Return Forecaster at Nickelsteamroller, I created a filter for what I consider an extremely safe investment: A-grade borrowers with 10+ years of employment and no inquiries, late payments, or past bankruptcies. Yet even this strict filter had 56 historical defaults (out of 3800, which is quite low). This proves that no cross-section of borrowers, no savvy filter, and no diversified peer to peer lending portfolio is able to avoid non-paying borrowers. None.

Long story short: lenders will experience defaults eventually, so we need to take precautionary steps to reduce the impact they will have on our account. The best way to reduce these defaults is diversification. If lenders diversify in as many loans as possible (at least 200 is fine), they reduce the negative impact of a defaulting loan. Lending Club and Prosper allow us to purchase notes (a portion of each loan) as small as $25. Take advantage of this! If we have 200 notes, a single defaulting loan will only drop our account by 0.5%.

Some of the horror stories we hear in peer to peer lending come from people who were not diversified. For instance, they invested their entire account in ten loans or less. A single default (again, very likely to happen) would then drop their account’s value by 10% or more. Avoid this situation by diversifying your account. Read my longer exploration of peer to peer lending diversification here.

Risk #2: Platforms May Make Mistakes in their Underwriting

We are dependent upon Lending Club and Prosper to only allow worthy borrowers into the system. Each day, people apply for a loan who have terrible credit or are submitting fake information, and the platforms catch the vast majority of these applications before they are able to get funding. However, sometime in the future a platform may mistakenly accept a large number of people who should be declined, or give high ratings to loans that are actual very risky. This would be similar to 2008 when the banks misclassified many mortgages as A-grade when they were actually junk. If a platform messes up its underwriting, lenders could experience a higher number of defaults than normal.

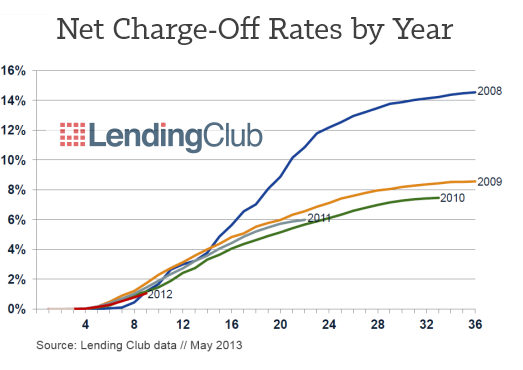

However, both Lending Club and Prosper have gotten increasingly better at underwriting. Each year that goes by informs their practice, with default rates having settled down nicely in the past few years (see chart above).

Risk #3: Platforms May Go Bankrupt

This is a very real possibility: a peer to peer lending company may go bankrupt. Thankfully, this is becoming less likely as time goes by. For years Lending Club was a cash-flow negative startup, but these days it is doing incredibly well, recently receiving a $125 million investment from Google. They are now cash flow positive and have millions of dollars in the bank. It is still possible Lending Club could go bankrupt, but I find this really unlikely.

Prosper, the smaller peer to peer lending platform, is also doing well these days. They are hitting record highs each month, a wonderful change that has come with a new management team. It is important to state that Prosper is still losing money as a company, but are well on their way to becoming cash-flow positive in the future. To boot, Prosper recently separated their notes into a different vehicle from the company, so in the event of bankruptcy, investor notes should be better protected.

For all the well-wishing, it is important to remember that these are uncertain times for this new industry. It takes surprisingly little for a web-based company like Lending Club to make a blunder and go under. Bankruptcy vehicles like the one Prosper created are helpful, but there really is no bulletproof evidence to show they actually work. As a result, I suggest all peer to peer lenders diversify across both platforms, and make peer to peer lending only a portion of their overall investments. While LendingMemo is certainly a cheerleader for this new industry, it is important to state how there are solid investment opportunities outside of peer to peer lending that can lessen our loses in the event of a bankruptcy.

Risk #4: National Unemployment May Increase Default Rates

Despite Lending Club and Prosper’s best underwriting efforts, a change in a national index like unemployment may make borrower default rates climb, causing our ROI to go down.

Lending Club lists a number of national factors in their prospectus that could make this happen (these are the same for Prosper):

- Consumer confidence may drop

- The price of people’s homes may go down

- Energy prices (like gasoline) could go up

- The value the US dollar could drop

- Many, many others

A recession like the one we experienced in 2008 could involve one or more of these factors, and would likely affect borrower default rates. Thankfully, we have good proof that our investment could weather these storms nicely, perhaps even better than traditional investments like the stock market. In the 2008 crisis, Lending Club still managed to give its investors a positive return. As Lending Club and Prosper’s underwriting improves each year, I believe the impact of a recession will be well navigated. However, there are no guarantees.

Risk #5: New Government Regulations Could Bring Hardship

In late 2008, the SEC decided that peer to peer loans were securities. This decision was a huge legal hurdle that the platforms had to cross, and not without struggle. Both Lending Club and Prosper entered quiet periods while they awaited government approval for peer to peer lending under this new legal definition. Even though both eventually emerged from this requirement, it ended up costing both platforms millions of dollars in legal fees.

These days, it seems like the roughest regulatory waters are behind us. Lending Club and Prosper are both well-equipped with solid legal teams that do a great job at keeping peer to peer lending practices within the rule of law. However, further regulations of this new industry are almost certainly just around the corner. It is impossible to know how burdensome these further requirements will be, and it remains a real possibility that these regulations could put a damper on the roaring success that peer to peer lending is currently experiencing.

Risk #6: Interest Rates May Rise

These days, the interest rate for the average American savings account is pathetically low, usually less than 0.5%. However, these rates may rise sometime in the future, and with this increase there may arrive a sudden lack of demand for some peer to peer loans. Why would investors choose to earn 6% on A-grade peer to peer loans when they could earn 5% in a federally-insured savings account like what most banks have? Savings accounts are almost risk-free investments while peer to peer lending is not.

However, in the event of interest rates rising, I think peer to peer lending would do just fine. AA and A-grade loans may struggle to get funded, but slightly riskier graded loans earning 10% and up seem like they will always have people interested in funding them.

Risk #7: Unforeseen Catastrophes

Despite our best planning about peer to peer lending risks, there are endless possible scenarios listed in Lending Club and Prosper’s prospectuses that could happen (see right). However unlikely, peer to peer lending companies could be subject to fires, water damage, natural disasters, terrorist attacks, electronic hacking, corporate scandal, etc. I hesitate to write this stuff, but it is listed in their prospectuses, so I might as well mention it.

Despite our best planning about peer to peer lending risks, there are endless possible scenarios listed in Lending Club and Prosper’s prospectuses that could happen (see right). However unlikely, peer to peer lending companies could be subject to fires, water damage, natural disasters, terrorist attacks, electronic hacking, corporate scandal, etc. I hesitate to write this stuff, but it is listed in their prospectuses, so I might as well mention it.

Conclusion: Laying Your Foundation

As peer to peer lending becomes more and more credible in the eyes of the nation, it should become somewhat less risky as an investment. The companies continue to improve their underwriting, Lending Club continues to grow by leaps and bounds, and Prosper is on its way to profitability. National and state regulators become more familiar with peer to peer lending with each passing year. The future may be uncertain, but I am confident that the (very real) risks that remain are becoming increasingly more reasonable to the new investor.

(Read more about these risks in the prospectuses at Lending Club [Apr 30 ’13, pp. 13-47] and Prosper [June 13 ’13, pp. 13-35].)

As lenders, we can build a solid foundation to have a great investing experience by staying aware of these dangers, particularly by being diversified and spreading additional investment into non-lending avenues. With knowledge of its risks, I believe the average American can go on to thrive within this exciting new way to put our extra cash to work.

[image credit: Lars Kasper “Thunderstorm Approaching” CC-BY 2.0]

I like how you laid out the very real risks of peer to peer lending. The more you know about the risks associated with an investment the better you can prepare for the worst scenario. I like to know what’s the worst that can happen and take steps to minimize the risk of losing an investment so that way I am not caught off guard. Great post.

Thanks Randy. Glad you enjoyed it.

Shouldn’t risk #4 just be included under risk #1?

Hi Andrew. Indeed, your question is a good one. The danger of defaults is actually related to #2 as well. The difference is who is to blame. In #1, the onus is on the investor. In #2, the platforms. In #3, the national condition. Lenders, a platform, and national factors can all increase borrower defaults, but they happen in three very distinct ways.

Hope this helps, Simon

Hey Simon, really enjoy your site. Great breakdown of peer to peer lending.

Thanks for stopping by Brett. Glad you’re enjoying the site.

Thanks for the detailed overview, Simon. I’ve just found your site and am enjoying reading your thoughts on P2P lending.

For me personally, my biggest concern is #3 – that one of the platforms may go under. The thought of trying to get my money out of a bankruptcy proceedings where presumably I’d be very subordinate debt, is frightening.

That said, given today’s economic environment, I’m sure I’ll have some money in P2P lending shortly.

Hi Jack. Good concerns. The bankruptcy situation was a lot more of a factor in the past few years, but I have a less worry about it these days. That said, it is still a real possibility.

A complete guideline for p2p lending aspirants. And a really a great article. I liked it Mr. Simon.

How and when can I withdraw my money from Lending Club or Prosper?

Thanks, Good explanations by the way.

There is also an issue of security. Your providing your account information to a company where there may be a breach in the future.